2020年湖北省ACCA报名条件和考试科目是什么?

发布时间:2020-01-03

ACCA是来自英国的一个注册会计师资格,因为广泛地被全球范围内的各地区和雇主认可而备受关注。与国内的各大财会证书相比,ACCA有着极其独特之处,例如它的报名条件、考试科目等内容。

2020年ACCA考试报名条件:

- 1、教育部认可的高等院校在校生(本科在校),顺利完成大一的课程考试,即可报名成为ACCA的正式学员;

- 2、凡具有教育部承认的大专以上学历,即可报名成为ACCA的正式学员;

- 3、年满16周岁,可先注册成为FLQ学员,在获得商业会计证书后转为ACCA学员,并可豁免AB、MA、FA三门课程。

ACCA官方政策指出,要具备以下条件之一者,均可报名参加ACCA考试。那么,ACCA考试共有哪些科目呢?

|

课程类别 |

课程序号 |

课程名称(中) |

课程名称(英) |

|

知识课程 |

AB |

会计师与企业 |

Accountant in Business |

|

MA |

管理会计 |

Management Accounting |

|

|

FA |

财务会计 |

Financial Accounting |

|

|

技能课程 |

LW |

公司法与商法 |

Corporate and Business Law |

|

PM |

业绩管理 |

Performance Management |

|

|

TX |

税务 |

Taxation |

|

|

FR |

财务报告 |

Financial Reporting |

|

|

AA |

审计与认证业务 |

Audit and Assurance |

|

|

FM |

财务管理 |

Financial Management |

|

课程类别 |

课程序号 |

课程名称(中) |

课程名称(英) |

|

核心课程 |

SBL |

战略商业领袖 |

Strategic Business Leader |

|

SBR |

战略商业报告 |

Strategic Business Report |

|

|

选修课程 |

AFM |

高级财务管理 |

Advanced Financial Management (AFM) |

|

APM |

高级业绩管理 |

AdvancedPerformance Management (APM) |

|

|

ATX |

高级税务 |

Advanced Taxation (ATX) |

|

|

AAA |

高级审计与认证业务 |

Advanced Audit and Assurance (AAA) |

如需了解或想更快报考ACCA, 请持续关注51题库考试学习网,51题库考试学习网将会不定时更新关于ACCA考试的相关资讯。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

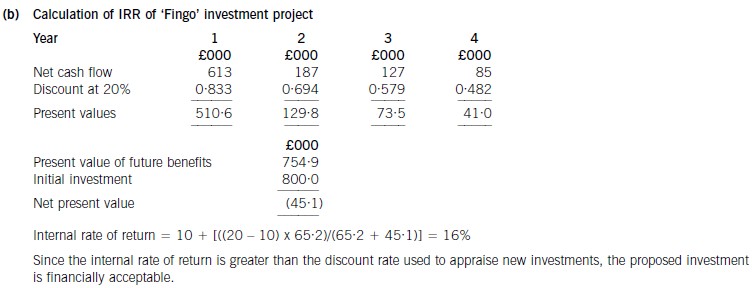

(b) Calculate the internal rate of return of the proposed investment and comment on your findings. (5 marks)

During the year the internal auditor of Mulligan Co discovered several discrepancies in the inventory records. In a

statement made to the board of directors, the internal auditor said:

‘I think that someone is taking items from the warehouse. A physical inventory count is performed every three months,

and it has become apparent that about 200 boxes of flat-packed chairs and tables are disappearing from the

warehouse every month. We should get someone to investigate what has happened and quantify the value of the

loss.’

Required:

(c) Define ‘forensic accounting’ and explain its relevance to the statement made by the internal auditor.

(5 marks)

(c) Forensic accounting is where an assurance provider investigates a specific issue, often with a legal consequence, such as a

suspected fraud. Specifically it is the process of gathering, analysing and reporting on data for the purpose of finding facts

and/or evidence in the context of financial/legal disputes and/or irregularities. The forensic accountant will also give

preventative advice based on evidence gathered. This advice is based usually on recommendations to improve the internal

control systems to prevent and detect fraud.

The relevance here is that Webb & Co are likely to be asked to provide a forensic accounting service to Mulligan Co.

The investigation will consider two issues – firstly whether the fraud actually happened, and secondly, if a fraud has taken

place, the financial value of the fraud. The investigation should determine who has perpetrated the fraud, and collect evidence

to help prosecute those involved in the deception.

In this case the suspicion that inventory is being stolen should be investigated, as there could be other reasons for the

discrepancy found in the inventory records. For example, the discrepancy could be caused by:

– Obsolete or damaged inventory thrown away but not eliminated from the inventory records

– Despatches from the warehouse not recorded in the inventory management system

– Incoming inventory being recorded incorrectly (e.g. recorded twice in the inventory management system)

– Inventory being held at a separate location and therefore not included in the count.

If it is found that thefts have taken place, then the forensic accountant should gather evidence to:

– Prove the identity of the persons involved

– Quantify the value of inventory taken.

The evidence gathered could be used to start criminal proceedings against those found to have been involved in the fraud.

(d) Corporate annual reports contain both mandatory and voluntary disclosures.

Required:

(i) Distinguish, using examples, between mandatory and voluntary disclosures in the annual reports of

public listed companies. (6 marks)

(d) (i) Mandatory and voluntary disclosures

Mandatory disclosures

These are components of the annual report mandated by law, regulation or accounting standard.

Examples include (in most jurisdictions) statement of comprehensive income (income or profit and loss statement),

statement of financial position (balance sheet), cash flow statement, statement of changes in equity, operating segmental

information, auditors’ report, corporate governance disclosure such as remuneration report and some items in the

directors’ report (e.g. summary of operating position). In the UK, the business review is compulsory.

Voluntary disclosures

These are components of the annual report not mandated in law or regulation but disclosed nevertheless. They are

typically mainly narrative rather than numerical in nature.

Examples include (in most jurisdictions) risk information, operating review, social and environmental information, and

the chief executive’s review.

5 GE Railways plc (GER) operates a passenger train service in Holtland. The directors have always focused solely on

the use of traditional financial measures in order to assess the performance of GER since it commenced operations

in 1992. The Managing Director of GER has asked you, as a management accountant, for assistance with regard to

the adoption of a balanced scorecard approach to performance measurement within GER.

Required:

(a) Prepare a memorandum explaining the potential benefits and limitations that may arise from the adoption of

a balanced scorecard approach to performance measurement within GER. (8 marks)

(a) To: Board of directors

From: Management Accountant

Date: 8 June 2007

The potential benefits of the adoption of a balanced scorecard approach to performance measurement within GER are as

follows:

A broader business perspective

Financial measures invariably have an inward-looking perspective. The balanced scorecard is wider in its scope and

application. It has an external focus and looks at comparisons with competitors in order to establish what constitutes best

practice and ensures that required changes are made in order to achieve it. The use of the balanced scorecard requires a

balance of both financial and non-financial measures and goals.

A greater strategic focus

The use of the balanced scorecard focuses to a much greater extent on the longer term. There is a far greater emphasis on

strategic considerations. It attempts to identify the needs and wants of customers and the new products and markets. Hence

it requires a balance between short term and long term performance measures.

A greater focus on qualitative aspects

The use of the balanced scorecard attempts to overcome the over-emphasis of traditional measures on the quantifiable aspects

of the internal operations of an organisation expressed in purely financial terms. Its use requires a balance between

quantitative and qualitative performance measures. For example, customer satisfaction is a qualitative performance measure

which is given prominence under the balanced scorecard approach.

A greater focus on longer term performance

The use of traditional financial measures is often dominated by financial accounting requirements, for example, the need to

show fixed assets at their historic cost. Also, they are primarily focused on short-term profitability and return on capital

employed in order to gain stakeholder approval of short term financial reports, the longer term or whole life cycle often being

ignored.

The limitations of a balanced scorecard approach to performance measurement may be viewed as follows:

The balanced scorecard attempts to identify the chain of cause and effect relationships which will provide the stimulus for

the future success of an organisation.

Advocates of a balanced scorecard approach to performance measurement suggest that it can constitute a vital component

of the strategic management process.

However, Robert Kaplan and David Norton, the authors of the balanced scorecard concept concede that it may not be suitable

for all firms. Norton suggests that it is most suitable for firms which have a long lead time between management action and

financial benefit and that it will be less suitable for firms with a short-term focus. However, other flaws can be detected in

the balanced scorecard.

The balanced scorecard promises to outline the theory of the firm by clearly linking the driver/outcome measures in a cause

and effect chain, but this will be difficult if not impossible to achieve.

The precise cause and effect relationships between measures for each of the perspectives on the balanced scorecard will be

complex because the driver and outcome measures for the various perspectives are interlinked. For example, customer

satisfaction may be seen to be a function of several drivers, such as employee satisfaction, manufacturing cycle time and

quality. However, employee satisfaction may in turn be partially driven by customer satisfaction and employee satisfaction

may partially drive manufacturing cycle time. A consequence of this non-linearity of the cause and effect chain (i.e., there is

non-linear relationship between an individual driver and a single outcome measure), is that there must be a question mark

as to the accuracy of any calculated correlations between driver and outcome measures. Allied to this point, any calculated

correlations will be historic. This implies that it will only be possible to determine the accuracy of cause and effect linkages

after the event, which could make the use of the balanced scorecard in dynamic industries questionable. If the market is

undergoing rapid evolution, for example, how meaningful are current measures of customer satisfaction or market share?

These criticisms do not necessarily undermine the usefulness of the balanced scorecard in presenting a more comprehensive

picture of organisational performance but they do raise doubts concerning claims that a balanced scorecard can be

constructed which will outline a clear cause and effect chain between driver and outcome measures and the firm’s financial

objectives.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-10

- 2020-02-22

- 2020-04-05

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-02-26

- 2020-02-26

- 2019-01-06

- 2020-02-22

- 2020-07-31

- 2020-01-03

- 2020-02-26

- 2020-09-03

- 2020-01-10

- 2020-02-28

- 2020-01-10

- 2021-05-22

- 2020-01-09

- 2020-01-09

- 2020-02-26

- 2019-01-06

- 2019-01-06

- 2020-01-03

- 2020-01-09

- 2020-01-07

- 2020-01-09

- 2020-01-10

- 2020-01-09

- 2020-01-03