福建省考生:ACCA准考证打印流程是怎么样的呢?

发布时间:2020-01-10

2020已经快要过去两个周啦,报名了2020年3月份ACCA考试的同学们快看过来,51题库考试学习网提醒各位同学:考前两周即可登录ACCA官网打印准考证了,那究竟操作流程是怎么样的呢? 且随51题库考试学习网继续往下看吧~

温馨提示一下初次备考ACCA考试的萌新,因为最新的ACCA考试相关政策暂未发布,所以本文的打印流程是借鉴往年的打印流程介绍,今年具体的情况还是要以官网为准哟

教程如下:

一.登录 MYACCA, 点击 Docket ,进入下一步

二.之后进入到第二个界面,点击 Access your docket

三. 进入第三个界面,财华学员选择第三个选项 Distance/Online learning,之后的 Learning Provider 下 拉 选 择 Beijing Caihuahongyuan

International Education Co.LId(Distance Learning)

其他学员根据自己的情况选填:

Full time

-face to face(classroom):全职-面对面(课堂)

Full time

-face to face(classroom):兼职-面对面(课堂)

Distance/online

learning blended learning:远程/在线学习混合学习

revision

course self-study:自学

四.之后点击 SAVE&CONFIRM 进行下载即可。

注意,面授和网课学习的同学按各自不同情况进行选择哦

以面授学员为例:

1.在‘Method of Study"选项选择"Part time -face to

face(classroom):兼职-面对面(课堂)

2.在‘’Country‘’选项选择默认项“China”,

3.在‘’Learning provider‘’选择“Shanghai Golden Finance”,别忘了在最后的小方框上点一个“√”

点击SAVE & CONFIRM,系统就就会自动跳转下载准考证啦!(远程网课学员或其他分校学员请按自身情况自行选择learning provider~)

注:

*Full

time -face to face(classroom):全职-面对面(课堂)

*Part

time -face to face(classroom):兼职-面对面(课堂)

*Distance/online

learning blended learning:远程/在线学习混合学习

*revision

course self-study:自学

ACCA考生参加考试时请务必携带好身份证(或护照)和准考证!!

准考证打印的注意事项:

1.ACCA准考证无需彩印,黑白打印即可;当然如果你希望准考证更美观,可以彩打。

2.按照规定ACCA准考证需双面打印,在一张A4纸上面。

3.准考证可以多打几张,以免丢失。

4.不要等到临考前才打印准考证,官网有时候会拥挤或犯病,所以提前打印为好。

以上信息就是关于ACCA国际注册会计师考试的准考证的打印相关流程,51题库考试学习网最后提醒一下大家,准考证必须有照片,准考证上面没有照片的学员请尽快与ACCA 英国方联系。

俗话说,有志者事竟成,备考ACCA考试的各位同学们,加油~

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

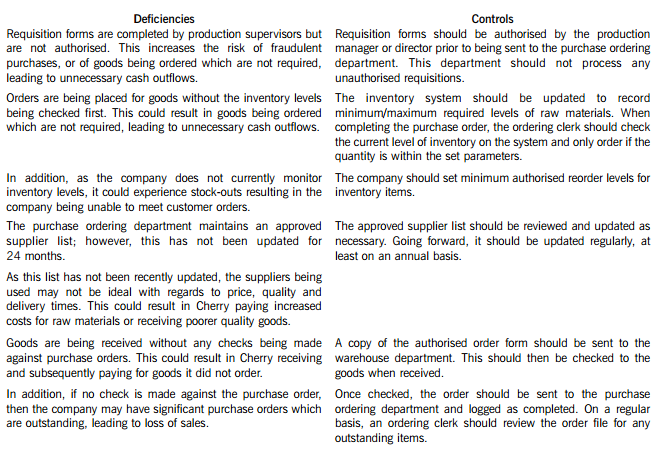

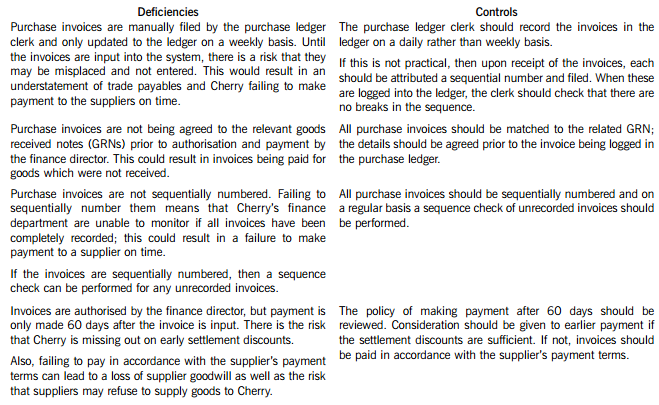

Cherry Blossom Co (Cherry) manufactures custom made furniture and its year end is 30 April. The company purchases its raw materials from a wide range of suppliers. Below is a description of Cherry’s purchasing system.

When production supervisors require raw materials, they complete a requisition form. and this is submitted to the purchase ordering department. Requisition forms do not require authorisation and no reference is made to the current inventory levels of the materials being requested. Staff in the purchase ordering department use the requisitions to raise sequentially numbered purchase orders based on the approved suppliers list, which was last updated 24 months ago. The purchasing director authorises the orders prior to these being sent to the suppliers.

When the goods are received, the warehouse department verifies the quantity to the suppliers despatch note and checks that the quality of the goods received are satisfactory. They complete a sequentially numbered goods received note (GRN) and send a copy of the GRN to the finance department.

Purchase invoices are sent directly to the purchase ledger clerk, who stores them in a manual file until the end of each week. He then inputs them into the purchase ledger using batch controls and gives each invoice a unique number based on the supplier code. The invoices are reviewed and authorised for payment by the finance director, but the actual payment is only made 60 days after the invoice is input into the system.

Required:

In respect of the purchasing system of Cherry Blossom Co:

(i) Identify and explain FIVE deficiencies; and

(ii) Recommend a control to address each of these deficiencies.

Note: The total marks will be split equally between each part.

Cherry Blossom Co’s (Cherry) purchasing system deficiencies and controls

5 Which of the following events after the balance sheet date would normally qualify as adjusting events according

to IAS 10 Events after the balance sheet date?

1 The bankruptcy of a credit customer with a balance outstanding at the balance sheet date.

2 A decline in the market value of investments.

3 The declaration of an ordinary dividend.

4 The determination of the cost of assets purchased before the balance sheet date.

A 1, 3, and 4

B 1 and 2 only

C 2 and 3 only

D 1 and 4 only

(b) As a newly-qualified Chartered Certified Accountant in Boleyn & Co, you have been assigned to assist the ethics

partner in developing ethical guidance for the firm. In particular, you have been asked to draft guidance on the

following frequently asked questions (‘FAQs’) that will be circulated to all staff through Boleyn & Co’s intranet:

(i) What Information Technology services can we offer to audit clients? (5 marks)

Required:

For EACH of the three FAQs, explain the threats to objectivity that may arise and the safeguards that should

be available to manage them to an acceptable level.

NOTE: The mark allocation is shown against each of the three questions.

(b) FAQs

(i) Information Technology (IT) services

The greatest threats to independence arise from the provision of any service which involves auditors in:

■ auditing their own work;

■ the decision-making process;

■ undertaking management functions of the client.

IT services potentially pose all these threats:

■ self-interest threat – on-going services that provide a large proportion of Boleyn’s annual fees will contribute to a

threat to objectivity;

■ self-review threat – e.g. when IT services provided involve (i) the supervision of the audit client’s employees in the

performance of their normal duties; or (ii) the origination of electronic data evidencing the occurrence of

transactions;

■ management threat – e.g. when the IT services involve making judgments and taking decisions that are properly

the responsibility of management.

Thus, services that involve the design and implementation of financial IT systems that are used to generate information

forming a significant part of a client’s accounting system or financial statements is likely to create significant ethical

threats.

Possible safeguards include:

■ disclosing and discussing fees with the client’s audit committees (or others charged with corporate governance);

■ the audit client providing a written acknowledgment (e.g. in an engagement letter) of its responsibility for:

– establishing and monitoring a system of internal controls;

– the operation of the system (hardware or software); and

– the data used or generated by the system;

■ the designation by the audit client of a competent employee (preferably within senior management) with

responsibility to make all management decisions regarding the design and implementation of the hardware or

software system;

■ evaluation of the adequacy and results of the design and implementation of the system by the audit client;

■ suitable allocation of work within the firm (i.e. staff providing the IT services not being involved in the audit

engagement and having different reporting lines); and

■ review of the audit opinion by an audit partner who is not involved in the audit engagement.

Services in connection with the assessment, design and implementation of internal accounting controls and risk

management controls are not considered to create a threat to independence provided that the firm’s personnel do not

perform. management functions.

It would be acceptable to provide IT services to an audit client where the systems are not important to any significant

part of the accounting system or the production of financial statements and do not have significant reliance placed on

them by the auditors, provided that:

■ a member of the client’s management has been designated to receive and take responsibility for the results of the

IT work undertaken; and

■ appropriate safeguards are put in place (e.g. using separate partners and staff for each role and review by a partner

not involved in the audit engagement).

It would also generally be acceptable to provide and install off-the-shelf accounting packages to an audit client.

(c) Briefly outline the corporation tax (CT) issues that Tay Limited should consider when deciding whether to

acquire the shares or the assets of Tagus LDA. You are not required to discuss issues relating to transfer

pricing. (7 marks)

(c) (1) Acquisition of shares

Status

The acquisition of shares in Tagus LDA will add another associated company to the group. This may have an adverse

effect on the rates of corporation tax paid by the two existing group companies, particularly Tay Limited.

Taxation of profits

Profits will be taxed in Portugal. Any profits remitted to the UK as dividends will be taxable as Schedule D Case V income,

but will attract double tax relief. Double tax relief will be available against two types of tax suffered in Portugal. Credit

will be given for any tax withheld on payments from Tagus LDA to Tay Limited and relief will also be available for the

underlying tax as Tay Limited owns at least 10% of the voting power of Tagus LDA. The underlying tax is the tax

attributable to the relevant profits from which the dividend was paid. Double tax relief is given at the lower rate of the

UK tax and the foreign tax (withholding and underlying taxes) suffered.

Losses

As Tagus LDA is a non-UK resident company, losses arising in Tagus LDA cannot be group relieved against profits of the

two UK companies. Similarly, any UK trading losses cannot be used against profits generated by Tagus LDA.

(2) Acquisition of assets

Status

The business of Tagus will be treated as a branch of Tay Limited i.e. an extension of the UK company’s activities. The

number of associated companies will be unaffected.

Taxation of profits

Tay Limited will be treated as having a permanent establishment in Portugal. Profits attributable to the Tagus business

will thus still be taxed in Portugal. In addition, the profits will be taxed in the UK as trading income. Double tax relief

will be available for the tax already suffered in Portugal at the lower of the two rates.

Capital allowances will be available. As the assets in question will not previously have been subject to a claim for UK

capital allowances, there will be no cost restriction and the consideration attributable to each asset will form. the basis

for the capital allowance claim.

Losses

The Tagus trade is part of Tay Limited’s trade, so any losses incurred by the Portuguese trade will automatically be offset

against the trading profits of the UK trade, and vice versa.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-12-24

- 2021-05-22

- 2020-09-04

- 2021-01-01

- 2020-01-08

- 2020-09-04

- 2020-09-04

- 2020-01-08

- 2020-08-15

- 2020-09-04

- 2020-01-10

- 2020-09-03

- 2020-09-04

- 2020-01-09

- 2020-12-24

- 2020-09-04

- 2020-09-04

- 2021-01-03

- 2020-01-09

- 2020-01-09

- 2020-01-10

- 2020-01-08

- 2020-09-04

- 2021-04-17

- 2020-01-10

- 2020-01-10

- 2020-09-04

- 2020-01-08

- 2020-01-10

- 2021-01-03