重磅消息:听说辽宁省ACCA考试有免考?你得有这些条件哦

发布时间:2020-01-09

众所周知,ACCA国际会计注册师考试科目多达15个科目,备考和复习起来的难度也毋容置疑是十分巨大的,而目前ACCA官方出台了相关的考试规则和免考政策,免考的科目一个人可以多达9科,具体免考的条件是什么呢?且随51题库考试学习网一起去了解一下,看看你能免考几科呢?

首先,在讲述免试政策之前,你得符合ACCA考试规则才可以参与考试,具体的规则如下:

1、申请参加ACCA考试者,必须首先注册成为ACCA学员。(需要到官网上申请注册)

2、学员必须按考试大纲设置的先后次序报考,即知识课程,技术课程,核心课程和选修课程。在一个课程中可以选择任意顺序报考。51题库考试学习网建议在一个课程中可以通过自身能力来考虑报名顺序,并不一定非要按照官方给出的顺序报名。

3、基础阶段的知识课程考试时间为两小时,基础阶段的技能课程和专业阶段所有课程考试时间为三小时,及格成绩为50分(百分制)。从2016年起,ACCA实行4个考季,即学员可选择在3、6、9、12月考季在当地笔试考点进行考试。学员每年最多报考8门。

4、基础阶段9门考试不设时限;专业阶段考试年限为7年,从通过第一门专业阶段考试之日算起。只要在7年内通过全部考试科目都算考核通过,下一步即可申请证书。

5、考试的报名时间不同,考试资费标准就不同(该优惠政策仅限网上报名)。简单点来说就是较早报名考试,费用会相对较少。报考时间分为提前报名时段,常规报名时段和后期报名时段。

接下来,就是万众瞩目的ACCA专业资格考试免试政策,建议ACCAer们收藏分享哟~

以上专业所对应的免试门数仅供参考,最终免试结果由ACCA英国总部审核确认。如有和ACCA英国总部所发布的免试政策有差异,一切以ACCA英国总部发布的文献为主~

如持有国外学历,或需要了解更详细免试情况,请查询官网或联系上财培训。

注意

1、在校生只有顺利通过整学年的课程才能够申请免试。(即未拿到学位证和学历证之前不能申请免试)

2、针对在校生的部分课程免试政策只适用于会计学专业全日制大学本科的在读学生,而不适用于硕士学位或大专学历的在读学生。

3、已完成MPAcc学位大纲规定课程,还需完成论文的学员也可注册并申请免试。但须提交由学校出具的通过所有MPAcc学位大纲规定课程的成绩单,并附注“该学员已通过所有MPAcc学位大纲规定课程,论文待完成”的说明。

4、特许学位(即海外大学与中国本地大学合作而授予海外大学学位的项目)部分完成时不能申请免试。

5、政策适用于在中国教育部认可的高等院校全部完成或部分完成本科课程的学生,而不考虑目前居住地点

大家是否已经了解到了自己能免试几科呢?51题库考试学习网提醒一下大家哦,免试虽然不用考试,但考试科目的报名费用还是得缴的哟~大家还是得及时缴费,以防出现不必要的麻烦~

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

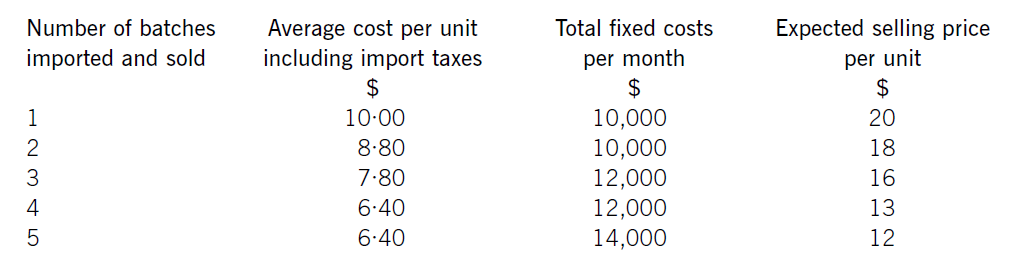

Jewel Co is setting up an online business importing and selling jewellery headphones. The cost of each set of headphones varies depending on the number purchased, although they can only be purchased in batches of 1,000 units. It also has to pay import taxes which vary according to the quantity purchased.

Jewel Co has already carried out some market research and identified that sales quantities are expected to vary depending on the price charged. Consequently, the following data has been established for the first month:

Required:

(a) Calculate how many batches Jewel Co should import and sell. (6 marks)

(b) Explain why Jewel Co could not use the algebraic method to establish the optimum price for its product.

(4 marks)

(b)Thealgebraicmodelrequiresseveralassumptionstobetrue.First,theremustbeaconsistentrelationshipbetweenprice(P)anddemand(Q),sothatademandequationcanbeestablished,usuallyintheform.P=a–bQ.Here,althoughthereisaclearrelationshipbetweenthetwo,itisnotaperfectlylinearrelationshipandsomorecomplicatedtechniquesarerequiredtocalculatethedemandequation.ItalsocannotbeassumedthatalinearrelationshipwillholdforallvaluesofPandQotherthanthefivegiven.Similarly,theremustbeaclearrelationshipbetweendemandandmarginalcost,usuallysatisfiedbyconstantvariablecostperunitandconstantfixedcosts.Thechangingvariablecostsperunitagaincomplicatetheissue,butitisthechangesinfixedcostswhichmakethealgebraicmethodlessusefulinJewel’scase.Thealgebraicmodelisonlysuitableforcompaniesoperatinginamonopolyanditisnotclearherewhetherthisisthecase,butitseemsunlikely,soany‘optimum’pricemightbecomeirrelevantifJewel’scompetitorschargesignificantlylowerprices.Othermoregeneralfactorsnotconsideredbythealgebraicmodelarepoliticalfactorswhichmightaffectimports,socialfactorswhichmayaffectcustomertastesandeconomicfactorswhichmayaffectexchangeratesorcustomerspendingpower.Thereliabilityoftheestimatesthemselves–forsalesprices,variablecostsandfixedcosts–couldalsobecalledintoquestion.

(ii) Calculate her income tax (IT) and national insurance (NIC) payable for the year of assessment 2006/07.

(4 marks)

2 Clifford and Amanda, currently aged 54 and 45 respectively, were married on 1 February 1998. Clifford is a higher

rate taxpayer who has realised taxable capital gains in 2007/08 in excess of his capital gains tax annual exemption.

Clifford moved into Amanda’s house in London on the day they were married. Clifford’s own house in Oxford, where

he had lived since acquiring it for £129,400 on 1 August 1996, has been empty since that date although he and

Amanda have used it when visiting friends. Clifford has been offered £284,950 for the Oxford house and has decided

that it is time to sell it. The house has a large garden such that Clifford is also considering an offer for the house and

a part only of the garden. He would then sell the remainder of the garden at a later date as a building plot. His total

sales proceeds will be higher if he sells the property in this way.

Amanda received the following income from quoted investments in 2006/07:

£

Dividends in respect of quoted trading company shares 1,395

Dividends paid by a Real Estate Investment Trust out of tax exempt property income 485

On 1 May 2006, Amanda was granted a 22 year lease of a commercial investment property. She paid the landlord

a premium of £6,900 and also pays rent of £2,100 per month. On 1 June 2006 Amanda granted a nine year

sub-lease of the property. She received a premium of £14,700 and receives rent of £2,100 per month.

On 1 September 2006 Amanda gave quoted shares with a value of £2,200 to a registered charity. She paid broker’s

fees of £115 in respect of the gift.

Amanda began working for Shearer plc, a quoted company, on 1 June 2006 having had a two year break from her

career. She earns an annual salary of £38,600 and was paid a bonus of £5,750 in August 2006 for agreeing to

come and work for the company. On 1 August 2006 Amanda was provided with a fully expensed company car,

including the provision of private petrol, which had a list price when new of £23,400 and a CO2 emissions rate of

187 grams per kilometre. Amanda is required to pay Shearer plc £22 per month in respect of the private use of the

car. In June and July 2006 Amanda used her own car whilst on company business. She drove 720 business miles

during this two month period and was paid 34 pence per mile. Amanda had PAYE of £6,785 deducted from her gross

salary in the tax year 2006/07.

After working for Shearer plc for a full year, Amanda becomes entitled to the following additional benefits:

– The opportunity to purchase a large number of shares in Shearer plc on 1 July 2007 for £3·30 per share. It is

anticipated that the share price on that day will be at least £7·50 per share. The company will make an interestfree

loan to Amanda equal to the cost of the shares to be repaid in two years.

– Exclusive free use of the company sailing boat for one week in August 2007. The sailing boat was purchased by

Shearer plc in January 2005 for use by its senior employees and costs the company £1,400 a week in respect

of its crew and other running expenses.

Required:

(a) (i) Calculate Clifford’s capital gains tax liability for the tax year 2007/08 on the assumption that the Oxford

house together with its entire garden is sold on 31 July 2007 for £284,950. Comment on the relevance

to your calculations of the size of the garden; (5 marks)

Assume that the corporation tax rates for the financial year 2004 apply throughout.

(b) Explain the corporation tax (CT) and value added tax (VAT) issues that Irroy should be aware of, if she

proceeds with her proposal for the Irish subsidiary, Green Limited. Your answer should clearly identify those

factors which will determine whether or not Green Limited is considered UK resident or Irish resident and

the tax implications of each alternative situation.

You need not repeat points that are common to each situation. (16 marks)

(b) There are several matters that Irroy will need to be aware of in relation to value added tax and corporation tax. These are set

out below.

Residence of subsidiary

Irroy will want to ensure that the subsidiary is treated as being resident in the Republic of Ireland. It will then pay corporation

tax on its profits at lower rates than in the UK. The country of incorporation usually claims taxing rights, but this is not by

itself sufficient. Irroy needs to be aware that a company can be treated as UK resident by virtue of the location of its central

management and control. This is usually defined as being where the board of directors meets to make strategic decisions. As

a result, Irroy needs to ensure that board meetings are conducted outside the UK.

If Green Limited is treated as being UK resident, it will be taxed in the UK on its worldwide income, including that arising in

the Republic of Ireland. However, as it will be conducting trading activities in the Republic of Ireland, Green Limited will also

be treated as being Irish resident as its activities in that country are likely to constitute a permanent establishment. Thus it

may also suffer tax in the Republic of Ireland as a consequence, although double tax relief will be available (see later).

A permanent establishment is broadly defined as a fixed place of business through which a business is wholly or partly carried

on. Examples of a permanent establishment include an office, factory or workshop, although certain activities (such as storage

or ancillary activities) can be excluded from the definition.

If Green Limited is treated as being an Irish resident company, any dividends paid to Aqua Limited will be taxed under

Schedule D Case V in the UK. Despite being non resident, Green Limited will still count as an associate of the existing UK

companies, and may affect the rates of tax paid by Aqua Limited and Aria Limited in the UK. However, as a non UK resident

company, Green Limited will not be able to claim losses from the UK companies by way of group relief.

Double tax relief

If Green Limited is treated as UK resident, corporation tax at UK rates will be payable on all profits earned. However, income

arising in the Republic of Ireland is likely to have been taxed in that country also by virtue of having a permanent

establishment located there. As the same profits have been taxed twice, double tax relief is available, either by reference to

the tax treaty between the UK and the Republic of Ireland, or on a unilateral basis, where the UK will give relief for the foreign

tax suffered.

If Green Limited is treated as an Irish resident company, it will pay tax in the Republic of Ireland, based on its worldwide

taxable profits. However, any repatriation of profits to the UK by dividend will be taxed on a receipts basis in the UK. Again,

double tax relief will be available as set out above.

Double tax relief is available against two types of tax. For payments made by Green Limited to Aqua Limited on which

withholding tax has been levied, credit will be given for the tax withheld. In addition, relief is available for the underlying tax

where a dividend is received from a foreign company in which Aqua Limited owns at least 10% of the voting power. The

underlying tax is the tax attributable to the relevant profits from which the dividend was paid.

Double tax relief is given at the lower rate of the UK tax and the foreign tax (withholding and underlying taxes) suffered.

Transfer pricing

Where groups have subsidiaries in other countries, they may be tempted to divert profits to subsidiaries which pay tax at lower

rates. This can be achieved by artificially changing the prices charged (known as the transfer price) between the group

companies. While they can do this commercially through common control, anti avoidance legislation seeks to correct this by

ensuring that for taxation purposes, profits on such intra-group transactions are calculated as if the transactions were carried

out on an arms length basis. Since 1 April 2004, this legislation can also be applied to transactions between UK group

companies.

If Green Limited is treated as a UK resident company, the group’s status as a small or medium sized enterprise means that

transfer pricing issues will not apply to transactions between Green Limited and the other UK group companies.

If Green Limited is an Irish resident company, transfer pricing issues will not apply to transactions between Green Ltd and the

UK resident companies because of the group’s status as a small or medium-sized enterprise and the existence of a double

tax treaty, based on the OECD model, between the UK and the Republic of Ireland.

Controlled foreign companies

Tax legislation exists to stop a UK company accumulating profits in a foreign subsidiary which is subject to a low tax rate.

Such a subsidiary is referred to as a controlled foreign company (CFC), and exists where:

(1) the company is resident outside the UK, and

(2) is controlled by a UK resident entity or persons, and

(3) pays a ‘lower level of tax’ in its country of residence.

A lower level of tax is taken to be less than 75% of the tax that would have been payable had the company been UK resident.

If Green Limited is an Irish resident company, it will be paying corporation tax at 12·5% so would appear to be caught by

the above rules and is therefore likely to be treated as a CFC.

Where a company is treated as a CFC, its profits are apportioned to UK resident companies entitled to at least 25% of its

profits. For Aqua Limited, which would own 100% of the shares in Green Limited, any profits made by Green Limited would

be apportioned to Aqua Limited as a deemed distribution. Aqua Limited would be required to self-assess this apportionment

on its tax return and pay UK tax on the deemed distribution (with credit being given for the Irish tax suffered).

There are some exemptions which if applicable the CFC legislation does not apply and no apportionments of profits will be

made. These include where chargeable profits of the CFC do not exceed £50,000 in an accounting period, or where the CFC

follows an acceptable distribution policy (distributing at least 90% of its chargeable profits within 18 months of the relevant

period).

Value added tax (VAT)

Green Limited will be making taxable supplies in the Republic of Ireland and thus (subject to exceeding the Irish registration

limit) liable to register for VAT there. If Green Limited is registered for VAT in the Republic of Ireland, then supplies of goods

made from the UK will be zero rated. VAT on the goods will be levied in the Republic of Ireland at a rate of 21%. Aqua Limited

will need to have proof of supply in order to apply the zero rate, and will have to issue an invoice showing Green Limited’s

Irish VAT registration number as well as its own. In the absence of such evidence/registration, Aqua Limited will have to treat

its transactions with Green Limited as domestic sales and levy VAT at the UK standard rate of 17·5%.

In addition to making its normal VAT returns, Aqua Limited will also be required to complete an EU Sales List (ESL) statement

each quarter. This provides details of the sales made to customers in the return period – in this case, Green Limited. Penalties

can be applied for inaccuracies or non-compliance.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-09

- 2020-01-09

- 2020-05-20

- 2020-03-01

- 2020-02-18

- 2020-02-01

- 2020-03-29

- 2020-01-09

- 2020-04-10

- 2020-01-01

- 2020-01-09

- 2019-12-28

- 2020-02-21

- 2020-05-12

- 2020-04-22

- 2020-02-26

- 2020-01-09

- 2020-03-12

- 2020-04-23

- 2020-01-09

- 2020-01-09

- 2020-05-15

- 2020-02-20

- 2020-01-01

- 2020-03-27

- 2020-04-17

- 2020-01-09

- 2020-01-09

- 2019-07-19

- 2020-01-09