ACCA考试常用公式汇总,值得上海市考生收藏!

发布时间:2020-01-10

距离2020年3月份的ACCA考试还有两个多月左右的时间,想必备考ACCA的同学们正在如火如荼地进行着复习。那么,今天这条“公式宝典”你一定要收好,或许会帮助你成功通过ACCA考试哦!接下来,51题库考试学习网将这份“公式宝典”分享给大家:

因为ACCA考试毕竟是国际性质的考试,因此一些题的计算可能就存在不同的计算方式,计算方式的不同也会导致结果的不同。

一、境内

1、税额=销项税-进项税

2、销项税=销售额×税率

3、视销征税无销额(1)当月类平均;(2)近类货平均,(3)组税价=成本×(1+成利率)

4、征增税及消税:

组税价=成本×(1+成润率)+消税

组税价=成本×(1+成润率)/(1-消率)

5、含税额换

不含税销额=含税销额/1+率(一般)

不含税销额=含税销额/1+征率(小规模)

6、购农销农品,或向小纳人购农品:

准扣的进税=买价×扣率(13%)

7、一般纳人外购货物付的运费

准扣的进税=运费×扣除率

*随运付的装卸、保费不扣

8、小纳人纳额=销项额×征率(6%或4%)

*不扣进额

9、小纳人不含税销额=含额/(1+征率)

10、自来水公司销水(6%)

不含税销额=发票额×(1+征率)

以上是国内物品的计算方式,接下来是国外进口的相关公式

二、进口货

1、组税价=关税完价+关税+消税

2、纳额=组税价×税率

三、出口货物退(免)税

1、"免、抵、退"计算方法(指生产企自营委外贸代出口自产)

(1)纳额=内销销税-(进税-免抵退税不免、抵税)

(2)免抵退税=FOB×外汇RMB牌价×退率-免抵退税抵减额

*FOB:出口货物离岸价。

*免抵退税抵减额=免税购原料价×退税率

免税购原料=国内购免原料+进料加工免税进料

进料加工免税进口料件组税价=到岸价+关、消税

(3)应退税和免抵税

A、如期末留抵税≤免抵退税,则:

应退税=期末留抵税

免抵税=免抵退税-应退税

B、期末留抵税>免抵退税,则:

应退税=免抵退税

免抵税=0

*期末留抵税额据《增值税纳税申报表》中"期末留抵税额"定。

(4)免抵退税不得免和抵税

免抵退税不免和抵税=FOB×外汇RMB牌价×(出口征率-出口退率)-免抵退税不免抵税抵减额

免抵退税不免和抵扣税抵减额=免税进原料价×(出口征率-出口货物退率)

2、先征后退

(1)外贸及外贸制度工贸企购货出口,出口增税免;出口后按收购成本与退税率算退税还外贸,征、退税差计企业成本

应退税额=外贸购不含增税购进金额×退税率

(2)外贸企购小纳人出货口增税退税规定:

A、从小纳人购并持普通发票准退税的抽纱、工艺品等12类出口货物,销售出口货入免,退还出口货进税

退税=[发票列(含税)销额]/(1+征率)×6%或5%

B、从小纳人购代开的增税发票的出口货:

退税=增税发票金额×6%或5%

C、外企托生企加工出口货的退税规定:

原辅料退税=国内原辅料增税发票进项×原辅料退税率

以上这些就是全部ACCA考试常用公式,希望对大家有所帮助!最后51题库考试学习网想告诉大家:“放弃可以找到一万个理由,但坚持只需一个信念!致敬那些在ACCA备考路上永不放弃的人,好结果只留给有毅力的人。”

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) The Superior Fitness Co (SFC), which is well established in Mayland, operates nine centres. Each of SFC’s

centres is similar in size to those of HFG. SFC also provides dietary plans and fitness programmes to its clients.

The directors of HFG have decided that they wish to benchmark the performance of HFG with that of SFC.

Required:

Discuss the problems that the directors of HFG might experience in their wish to benchmark the performance

of HFG with the performance of SFC, and recommend how such problems might be successfully addressed.

(7 marks)

(b) There are a number of potential problems which the directors of HFG need to recognise. These are as follows:

(i) There needs to exist a sufficient incentive for SFO to share their information with HFG as the success of any

benchmarking programme is dependent upon obtaining accurate information about the comparator organisation. This is

not an easy task to accomplish, as many organisations are reluctant to reveal confidential information to competitors.

The directors of HFG must be able to convince the directors of SFO that entering into a benchmarking arrangement is a

potential ‘win-win situation’.

(ii) The value of the exercise must be sufficient to justify the cost involved. Also, it is inevitable that behavioural issues will

need to be addressed in any benchmarking programme. Management should give priority to the need to communicate

the reasons for undertaking a programme of benchmarking in order to gain the full co-operation of its personnel whilst

reducing the potential level of resistance to change.

(iii) Management need to handle the ethical implications relating to the introduction of benchmarking in a sensitive manner

and should endeavour, insofar as possible, to provide reassurance to employees that their status, remuneration and

working conditions will not suffer as a consequence of the introduction of any benchmarking initiatives.

(ii) Identify the points that must be confirmed and any action necessary in order for capital treatment to

apply to the transaction. (4 marks)

(ii) Ensuring capital treatment

For the capital treatment to apply, a number of conditions need to be satisfied such that the following points need to be

confirmed.

– The business of Acrux Ltd consists wholly or mainly of the carrying on of a trade as opposed to the making of

investments.

– Spica is UK resident and ordinarily resident despite living in both the UK and Solaris.

– The transaction is being carried out for the purpose of the company’s trade and is not part of a scheme intended

to avoid tax. This is likely to be the case as HMRC accept that a management disagreement over the running of

the company has an adverse effect on the running of the business.

In addition, Spica must have owned the shares for at least five years so the transaction must not take place until

1 October 2008.

Moonstar Co is a property development company which is planning to undertake a $200 million commercial property development. Moonstar Co has had some difficulties over the last few years, with some developments not generating the expected returns and the company has at times struggled to pay its finance costs. As a result Moonstar Co’s credit rating has been lowered, affecting the terms it can obtain for bank finance. Although Moonstar Co is listed on its local stock exchange, 75% of the share capital is held by members of the family who founded the company. The family members who are shareholders do not wish to subscribe for a rights issue and are unwilling to dilute their control over the company by authorising a new issue of equity shares. Moonstar Co’s board is therefore considering other methods of financing the development, which the directors believe will generate higher returns than other recent investments, as the country where Moonstar Co is based appears to be emerging from recession.

Securitisation proposals

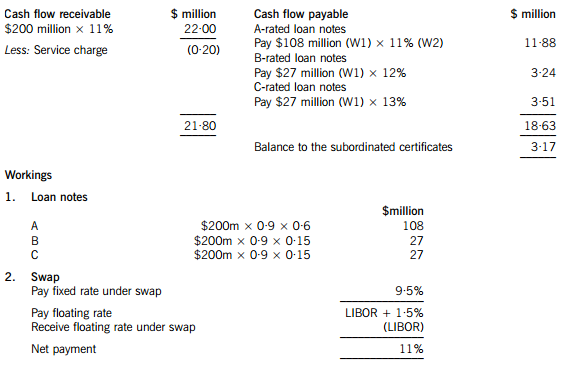

One of the non-executive directors of Moonstar Co has proposed that it should raise funds by means of a securitisation process, transferring the rights to the rental income from the commercial property development to a special purpose vehicle. Her proposals assume that the leases will generate an income of 11% per annum to Moonstar Co over a ten-year period. She proposes that Moonstar Co should use 90% of the value of the investment for a collateralised loan obligation which should be structured as follows:

– 60% of the collateral value to support a tranche of A-rated floating rate loan notes offering investors LIBOR plus 150 basis points

– 15% of the collateral value to support a tranche of B-rated fixed rate loan notes offering investors 12%

– 15% of the collateral value to support a tranche of C-rated fixed rate loan notes offering investors 13%

– 10% of the collateral value to support a tranche as subordinated certificates, with the return being the excess of receipts over payments from the securitisation process

The non-executive director believes that there will be sufficient demand for all tranches of the loan notes from investors. Investors will expect that the income stream from the development to be low risk, as they will expect the property market to improve with the recession coming to an end and enough potential lessees to be attracted by the new development.

The non-executive director predicts that there would be annual costs of $200,000 in administering the loan. She acknowledges that there would be interest rate risks associated with the proposal, and proposes a fixed for variable interest rate swap on the A-rated floating rate notes, exchanging LIBOR for 9·5%.

However the finance director believes that the prediction of the income from the development that the non-executive director has made is over-optimistic. He believes that it is most likely that the total value of the rental income will be 5% lower than the non-executive director has forecast. He believes that there is some risk that the returns could be so low as to jeopardise the income for the C-rated fixed rate loan note holders.

Islamic finance

Moonstar Co’s chief executive has wondered whether Sukuk finance would be a better way of funding the development than the securitisation.

Moonstar Co’s chairman has pointed out that a major bank in the country where Moonstar Co is located has begun to offer a range of Islamic financial products. The chairman has suggested that a Mudaraba contract would be the most appropriate method of providing the funds required for the investment.

Required:

(a) Calculate the amounts in $ which each of the tranches can expect to receive from the securitisation arrangement proposed by the non-executive director and discuss how the variability in rental income affects the returns from the securitisation. (11 marks)

(b) Discuss the benefits and risks for Moonstar Co associated with the securitisation arrangement that the non-executive director has proposed. (6 marks)

(c) (i) Discuss the suitability of Sukuk finance to fund the investment, including an assessment of its appeal to potential investors. (4 marks)

(ii) Discuss whether a Mudaraba contract would be an appropriate method of financing the investment and discuss why the bank may have concerns about providing finance by this method. (4 marks)

(a) An annual cash flow account compares the estimated cash flows receivable from the property against the liabilities within the securitisation process. The swap introduces leverage into the arrangement.

The holders of the certificates are expected to receive $3·17million on $18 million, giving them a return of 17·6%. If the cash flows are 5% lower than the non-executive director has predicted, annual revenue received will fall to $20·90 million, reducing the balance available for the subordinated certificates to $2·07 million, giving a return of 11·5% on the subordinated certificates, which is below the returns offered on the B and C-rated loan notes. The point at which the holders of the certificates will receive nothing and below which the holders of the C-rated loan notes will not receive their full income will be an annual income of $18·83 million (a return of 9·4%), which is 14·4% less than the income that the non-executive director has forecast.

(b) Benefits

The finance costs of the securitisation may be lower than the finance costs of ordinary loan capital. The cash flows from the commercial property development may be regarded as lower risk than Moonstar Co’s other revenue streams. This will impact upon the rates that Moonstar Co is able to offer borrowers.

The securitisation matches the assets of the future cash flows to the liabilities to loan note holders. The non-executive director is assuming a steady stream of lease income over the next 10 years, with the development probably being close to being fully occupied over that period.

The securitisation means that Moonstar Co is no longer concerned with the risk that the level of earnings from the properties will be insufficient to pay the finance costs. Risks have effectively been transferred to the loan note holders.

Risks

Not all of the tranches may appeal to investors. The risk-return relationship on the subordinated certificates does not look very appealing, with the return quite likely to be below what is received on the C-rated loan notes. Even the C-rated loan note holders may question the relationship between the risk and return if there is continued uncertainty in the property sector.

If Moonstar Co seeks funding from other sources for other developments, transferring out a lower risk income stream means that the residual risks associated with the rest of Moonstar Co’s portfolio will be higher. This may affect the availability and terms of other borrowing.

It appears that the size of the securitisation should be large enough for the costs to be bearable. However Moonstar Co may face unforeseen costs, possibly unexpected management or legal expenses.

(c) (i) Sukuk finance could be appropriate for the securitisation of the leasing portfolio. An asset-backed Sukuk would be the same kind of arrangement as the securitisation, where assets are transferred to a special purpose vehicle and the returns and repayments are directly financed by the income from the assets. The Sukuk holders would bear the risks and returns of the relationship.

The other type of Sukuk would be more like a sale and leaseback of the development. Here the Sukuk holders would be guaranteed a rental, so it would seem less appropriate for Moonstar Co if there is significant uncertainty about the returns from the development.

The main issue with the asset-backed Sukuk finance is whether it would be as appealing as certainly the A-tranche of the securitisation arrangement which the non-executive director has proposed. The safer income that the securitisation offers A-tranche investors may be more appealing to investors than a marginally better return from the Sukuk. There will also be costs involved in establishing and gaining approval for the Sukuk, although these costs may be less than for the securitisation arrangement described above.

(ii) A Mudaraba contract would involve the bank providing capital for Moonstar Co to invest in the development. Moonstar Co would manage the investment which the capital funded. Profits from the investment would be shared with the bank, but losses would be solely borne by the bank. A Mudaraba contract is essentially an equity partnership, so Moonstar Co might not face the threat to its credit rating which it would if it obtained ordinary loan finance for the development. A Mudaraba contract would also represent a diversification of sources of finance. It would not require the commitment to pay interest that loan finance would involve.

Moonstar Co would maintain control over the running of the project. A Mudaraba contract would offer a method of obtaining equity funding without the dilution of control which an issue of shares to external shareholders would bring. This is likely to make it appealing to Moonstar Co’s directors, given their desire to maintain a dominant influence over the business.

The bank would be concerned about the uncertainties regarding the rental income from the development. Although the lack of involvement by the bank might appeal to Moonstar Co's directors, the bank might not find it so attractive. The bank might be concerned about information asymmetry – that Moonstar Co’s management might be reluctant to supply the bank with the information it needs to judge how well its investment is performing.

(ii) Describe the procedures to verify the number of serious accidents in the year ended 30 November 2007.

(4 marks)

(ii) Procedures to verify the number of serious accidents during 2007 could include the following:

Tutorial note: procedures should focus on the completeness of the disclosure as it is in the interest of Sci-Tech Co to

understate the number of serious accidents.

– Review the accident log book and count the total number of accidents during the year

– Discuss the definition of ‘serious accident’ with the directors and clarify exactly what criteria need to be met to

satisfy the definition

– For serious accidents identified:

? review HR records to determine the amount of time taken off work

? review payroll records to determine the financial amount of sick pay awarded to the employee

? review correspondence with the employee regarding the accident.

Tutorial note: the above will help to clarify that the accident was indeed serious.

– Review board minutes where the increase in the number of serious accidents has been discussed

– Review correspondence with Sci-Tech Co’s legal advisors to ascertain any legal claims made against the company

due to accidents at work

– Enquire as to whether any health and safety visits have been conducted during the year by regulatory bodies, and

review any documentation or correspondence issued to Sci-Tech Co after such visits.

Tutorial note: it is highly likely that in a regulated industry such as pharmaceutical research, any serious accident

would trigger a health and safety inspection from the appropriate regulatory body.

– Discuss the level of accidents with representatives of Sci-Tech Co’s employees to reach an understanding as to

whether accidents sometimes go unreported in the accident log book.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2019-07-20

- 2020-01-09

- 2020-04-28

- 2020-01-10

- 2020-01-10

- 2020-05-09

- 2020-01-31

- 2020-01-10

- 2020-01-10

- 2019-12-06

- 2020-01-09

- 2020-04-18

- 2021-06-03

- 2020-05-14

- 2020-03-07

- 2020-03-11

- 2020-01-10

- 2020-03-25

- 2020-01-10

- 2020-02-01

- 2020-01-01

- 2020-01-10

- 2020-01-10

- 2020-04-06

- 2020-01-10

- 2020-01-10

- 2020-01-09

- 2020-01-10

- 2019-02-15

- 2020-05-09