四川省考生们!2020年ACCA国际会计师考试科目、考试题题型题量!

发布时间:2020-01-09

2020年一月即将过去一半了,各位参加3月份ACCA考试的ACCAer们得要抓紧时间好好复习了呀~考试科目难度不了解?不知道怎么在有限的时间规划复习的侧重点?这些问题都通通不用担心,接下来51题库考试学习网就为大家讲解关于ACCA考试每个科目的难度,便于各位ACCAer们有重点的复习。

最简单的:知识课程原F1,F2,F3

这三个科目的内容在ACCA所有科目中属于最基础也是新手最容易入门的,难度不算太大,但仍然需要认真复习,且需要掌握的内容不多,都是会计学的基础。也正是因为这样,会计学本专业学生在完成第二年课程后可以免试这三科。这三科考试都为机考考试,且选择题居多,通过率按照往年的数据来看都在70%左右。

技能课程:原F4,F5,F6,F7,F9

这几门相对前三门难度有所提高,但相比较后面的专业阶段的考试科目来说,通过难度不算太大的。F4法律内容较多,需要背诵,但总体不难。F5是F2的进阶版,知识点重叠的部分很多。因此,只要F2学的好,通过F5也不在话下。F6关于税法,考试时以计算题为主,也正是因为计算题量大,对于中国考生来说,难度并不高,但这一部分对计算能力的考核的难度还是有的。F9和P1相似,以文字内容为主,想要通过考试需要动用记忆能力,记忆能力欠佳的考生建议反复多读和背,只要认真背过知识点的,总体难度一般。这几门中相对较难的是F7,从近几年的通过率来看是最低的,内容涉及到财务报表的编制,为P2专业阶段的考试打基础。想要编平报表,需要大量的练习历年真题是必不可少的。

AA(F8)和SBL(P1+P3),AAA(F7)

这三门之所以难度较高,原因在于大量的主观论述题。不少考生表示考到这几科才发现ACCA考试与其说是会计考试,不如说更像是英语作文考试。这几门难就难在需要站在一定高度去分析问题,且相比之前的F阶段考试需要更深层次的去了解。在F8阶段,需要了解具体的审计程序,而到了P7,则需要从事务所合伙人的角度来思考问题。考到这一等级,ACCA考试的核心才能体现出来,之前的F阶段的全部考试都是为此打基础。对于思维方式的养成初见成效,之前熟悉的备考应试方法显得捉襟见肘,考生唯有自己学会分析问题的方法,并用自己的语言阐述出来。

SBR(P2)和选修课程(P4-P7)

这几科之所以难,难在全为文字大题,光题目都有好几页。因此这不仅仅是对考生英语词汇量的挑战,不少同学表示光是读懂题目都已经非常有挑战性。但好在P4,P5,P6,P7四科是可以4选2报考的,考生可以根据自己对科目的掌握程度,结合自己的综合能力水平,选择自己最容易通过的科目报考。到这一阶段,考察的能力也是最多的,不仅需要记忆,理解相应的知识点,还需要用自己的语言表达观点。这就是对考生的记忆、理解、表达的这三方面的考核,但即便这样,经常也会有大神表示P5非常简单,其原因还是自己充分理解了考试内容和分析问题的方法。

F级跟P级的差别,就是F级只要花足够时间去学习,及格都不成问题,通过的话也是不在话下的。

但P级就有很多开放式答案,实在难说能掌握到什么程度。考试靠发挥、考心态、还有运气成分,因此建议大家在此阶段就需要更加努力的去复习和学习。

综合分析完所有ACCA考试科目,51题库考试学习网也收集到不少关于ACCAer自己的一些看法,看看他们眼中的考试科目难度是否和你想的一样呢?

首先,很多小伙伴说,在经历了前期4科的70+%通过率之后,F5忽然滑落到40%左右。这一点让不少新手ACCA都是十分胆怯的。对考取ACCA证书信心备受打击。

51题库考试学习网询认为,任何考试都有它的一些备考技巧,因此想要顺利通过F5只需要注意3个方面的问题即可。

以知识点为重,注意记忆

先看F5的考试题型:

Section A 15*2(选择题,共30分)

Section B 3*5*2(选择题,共30分)

Section C 2*20(我们俗称的“大题”,有计算和文字,共40分)

可以看出,光是选择题就占60分的比重,所以在F5的备考中,保证选择题不丢分是重中之重。因此建议大家可以多练习真题才可以,将章节的大框架理解到位。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

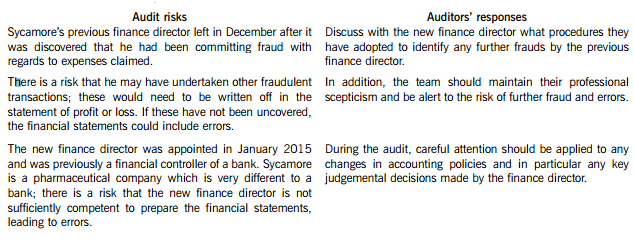

You are the audit supervisor of Maple & Co and are currently planning the audit of an existing client, Sycamore Science Co (Sycamore), whose year end was 30 April 2015. Sycamore is a pharmaceutical company, which manufactures and supplies a wide range of medical supplies. The draft financial statements show revenue of $35·6 million and profit before tax of $5·9 million.

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

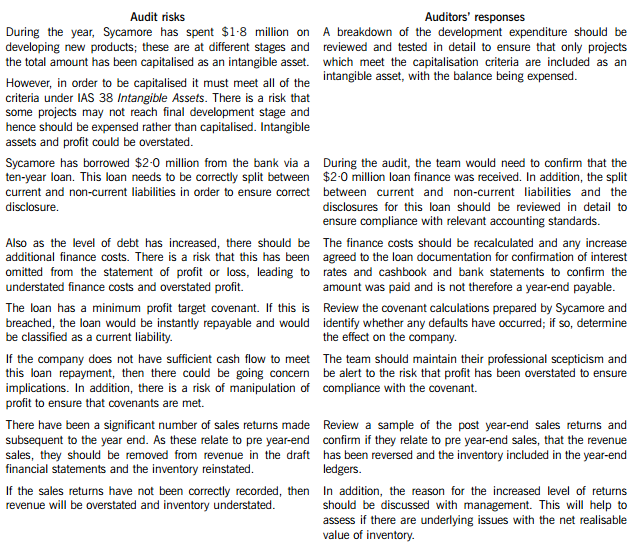

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

(a) Fraud responsibility

Maple & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error.

In order to fulfil this responsibility, Maple & Co is required to identify and assess the risks of material misstatement of the financial statements due to fraud.

They need to obtain sufficient appropriate audit evidence regarding the assessed risks of material misstatement due to fraud, through designing and implementing appropriate responses. In addition, Maple & Co must respond appropriately to fraud or suspected fraud identified during the audit.

When obtaining reasonable assurance, Maple & Co is responsible for maintaining professional scepticism throughout the audit, considering the potential for management override of controls and recognising the fact that audit procedures which are effective in detecting error may not be effective in detecting fraud.

To ensure that the whole engagement team is aware of the risks and responsibilities for fraud and error, ISAs require that a discussion is held within the team. For members not present at the meeting, Sycamore’s audit engagement partner should determine which matters are to be communicated to them.

(b) Audit risks and auditors’ responses

(c) (i) Review engagements

Review engagements are often undertaken as an alternative to an audit, and involve a practitioner reviewing financial data, such as six-monthly figures. This would involve the practitioner undertaking procedures to state whether anything has come to their attention which causes the practitioner to believe that the financial data is not in accordance with the financial reporting framework.

A review engagement differs to an external audit in that the procedures undertaken are not nearly as comprehensive as those in an audit, with procedures such as analytical review and enquiry used extensively. In addition, the practitioner does not need to comply with ISAs as these only relate to external audits.

(ii) Levels of assurance

The level of assurance provided by audit and review engagements is as follows:

External audit – A high but not absolute level of assurance is provided, this is known as reasonable assurance. This provides comfort that the financial statements present fairly in all material respects (or are true and fair) and are free of material misstatements.

Review engagements – where an opinion is being provided, the practitioner gathers sufficient evidence to be satisfied that the subject matter is plausible; in this case negative assurance is given whereby the practitioner confirms that nothing has come to their attention which indicates that the subject matter contains material misstatements.

(b) Assuming that the cost of equity and cost of debt do not alter, estimate the effect of the share repurchase on the company’s cost of capital and value. (5 marks)

(b) Estimated new cost of capital:

If equity is repurchased such that the gearing becomes 50% equity, 50% debt, the new estimated weighted average cost of capital is:

(b) Explain how Perfect Shopper might re-structure its upstream supply chain to address the problems identified

in the scenario. (10 marks)

(b) Perfect Shopper currently has a relatively short upstream supply chain. They are bulk purchasers from established suppliers

of branded goods. Their main strength at the moment is to offer these branded goods at discounted prices to neighbourhood

shops that would normally have to pay premium prices for these goods.

In the upstream supply chain, the issue of branding is a significant one. At present, Perfect Shopper only provides branded

goods from established names to its customers. As far as the suppliers are concerned, Perfect Shopper is the customer and

the company’s regional warehouses are supplied as if they were the warehouses of conventional supermarkets. Perfect

Shopper might look at the following restructuring opportunities within this context:

– Examining the arrangements for the delivery of products from suppliers to the regional warehouses. At present this is in

the hands of the suppliers or contractors appointed by suppliers. It appears that when Perfect Shopper was established

it decided not to contract its own distribution. This must now be open to review. It is likely that competitors have

established contractual arrangements with logistics companies to collect products from suppliers. Perfect Shopper must

examine this, accompanied by an investigation into downstream distribution. A significant distribution contract would

probably include the branding of lorries and vans and this would provide an opportunity to increase brand visibility and

so tackle this issue at the same time.

– Contracting the supply and distribution of goods also offers other opportunities. Many integrated logistics contractors also

supply storage and warehousing solutions and it would be useful for Perfect Shopper to evaluate the costs of these.

Essentially, distribution, warehousing and packaging could be outsourced to an integrated logistics company and Perfect

Shopper could re-position itself as a primarily sales and marketing operation.

– Finally, Perfect Shopper must review how it communicates orders and ordering requirements with its suppliers. Their

reliance on supplier deliveries suggests that the relationship is a relatively straightforward one. There may be

opportunities for sharing information and allowing suppliers access to forecasted demand. There are many examples

where organisations have allowed suppliers access to their information to reduce costs and to improve the efficiency of

the supply chain as a whole.

The suggestions listed above assume that Perfect Shopper continues to only supply branded goods. Moving further upstream

in the supply chain potentially moves the company into the manufacture and supply of goods. This will raise a number of

significant issues about the franchise itself.

At present Perfect Shopper has, by necessity, concentrated on branded goods. It has not really had to understand how these

goods sell in specific locations because it has not been able to offer alternatives. The content of the standing order reflects

how the neighbourhood shop wishes to compete in its locality. However, if Perfect Shopper decides to commission its own

brand then the breadth of products is increased. Neighbourhood shops would be able to offer ‘own brand’ products to compete

with supermarkets who also focus on own brand products. It would also increase the visibility of the brand. However, Perfect

Shopper must be sure that this approach is appropriate as a whole. It could easily produce an own brand that reduces the

overall image of the company and hence devalues the franchise. Much more research is needed to assess the viability ofproducing ‘own brand’ goods.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-09

- 2020-05-13

- 2020-04-22

- 2020-01-10

- 2020-01-10

- 2020-04-21

- 2020-01-09

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2021-08-21

- 2020-01-10

- 2020-01-10

- 2020-02-22

- 2020-01-10

- 2020-03-14

- 2020-01-10

- 2020-04-07

- 2020-01-10

- 2020-04-08

- 2020-01-10

- 2020-01-10

- 2020-04-17

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2021-07-31

- 2020-01-10

- 2020-02-20

- 2020-01-10