提前看看ACCA考试的通过率分析情况

发布时间:2020-04-22

小伙伴们看过来啦! 有关ACCA考试的通过率及情况分析,51题库考试学习网在这里将作如下的回复,希望各位小伙伴们能够采纳,跟着51题库考试学习网一起来看看吧!

关于ACCA考试的报考条件

报名注册ACCA条件,具备以下3条中的1条即可:

1、教育部认可的高等院校在校生(本科在校),顺利完成大一的课程考试,即可报名成为ACCA的正式学员;

2、凡具有教育部承认的大专以上学历,即可报名成为ACCA的正式学员;

3、未符合1、2项报名资格的申请者,可以先申请参加FIA(Foundations in

Accountancy)基础财务资格考试。在完成FAB(基础商业会计)、FMA(基础管理会计)、FFA(基础财务会计)3门课程后,可以豁免ACCAF1-F3三门课程的考试,直接进入ACCA技能课程的考试。

ACCA具有系统性的考试体系,在报考条件上奉行宽进严出的准则,对于年满16周岁的中国公民来说,都可以报考。即使是从零基础开始,最终也有机会成为一个具备高端财务技能和职业操守的综合性人才,并胜任跨国集团的各类高级财务岗位。

关于ACCA考试的通过率分析

目前2020年官方公布了3月季相关考试及通过率情况,由此分析如下:

1、AB-LW前四科目通过率依旧保持乐观,考试难度相对较低。

2、PM难度进一步增加,单科通过率仅有35%,创2009年以来的新低,仅比战略阶段的最难的选修课高1%~2%。

PM业绩管理一直是历年技能课程考试中难度较大的科目,历年通过率约在38%~43%之间。但从今年首次考季的整体结果来看,本次考试要比往年最低点38%再低3个百分点,由此可见该科目在难度上不容小觑,甚至在实施新大纲后难度还会有所提升。

3、TX为2018年以来最低水平。虽然为最低点,但TX通过率波动较小,自2018年来,始终维持在46%~51%之间。

4、FR为2015年以来最低水平,为44%。PR往年通过率同TX一样,约为46%~51%。

5、AA本次通过率为36%,同2019年9月考季相同,同为2015年以来最低点。与之相较,FM一科的通过率则处在正常偏低的位置。

6、对于战略阶段的课程来说,SBL/SBR以及除高级税务之外的三门选修课程,通过率相对较为稳定,与以往相差无几。不过,在本次考季当中,ATX一科目的通过率却创造了近年来最高纪录,高达44%。

好了,以上就是有关于ACCA考试的全部内容。如果想要了解更多的考试信息,考友们可以关注51题库考试学习网哦!感谢各位的支持与信任,最后衷心祝愿考生们能取得理想成绩!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) The CEO of Oceania National Airways (ONA) has already strongly rejected the re-positioning of ONA as a ‘no

frills’ low-cost budget airline.

(i) Explain the key features of a ‘no frills’ low-cost strategy. (4 marks)

(b) (i) A ‘no frills’ strategy combines low price with low perceived benefits of the product or service. It is primarily associated

with commodity goods and services where customers do not discern or value differences in the products or services

offered by competing suppliers. In some circumstances the customer cannot afford the better quality product or service

of a particular supplier. ‘No frills’ strategies are particularly attractive in price-sensitive markets. Within the airline sector,

the term ‘no frills’ is associated with a low cost pricing strategy. In Europe, at the time of writing, easyJet and Ryanair

are the two dominant ‘no frills’ low-cost budget airlines. In Asia, AirAsia and Tiger Airways are examples of ‘no frills’ lowcost

budget carriers. ‘No frills’ strategies usually exist in markets where buyers have high power coupled with low

switching costs and so there is little brand loyalty. It is also prevalent in markets where there are few providers with

similar market shares. As a result of this the cost structure of each provider is similar and new product and service

initiatives are quickly copied. Finally a ‘no frills’ strategy might be pursued by a company entering the market, using thisas a strategy to gain market share before progressing to alternative strategies.

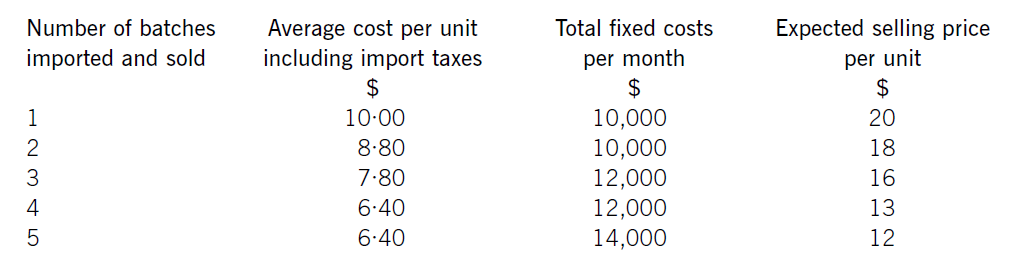

Jewel Co is setting up an online business importing and selling jewellery headphones. The cost of each set of headphones varies depending on the number purchased, although they can only be purchased in batches of 1,000 units. It also has to pay import taxes which vary according to the quantity purchased.

Jewel Co has already carried out some market research and identified that sales quantities are expected to vary depending on the price charged. Consequently, the following data has been established for the first month:

Required:

(a) Calculate how many batches Jewel Co should import and sell. (6 marks)

(b) Explain why Jewel Co could not use the algebraic method to establish the optimum price for its product.

(4 marks)

(b)Thealgebraicmodelrequiresseveralassumptionstobetrue.First,theremustbeaconsistentrelationshipbetweenprice(P)anddemand(Q),sothatademandequationcanbeestablished,usuallyintheform.P=a–bQ.Here,althoughthereisaclearrelationshipbetweenthetwo,itisnotaperfectlylinearrelationshipandsomorecomplicatedtechniquesarerequiredtocalculatethedemandequation.ItalsocannotbeassumedthatalinearrelationshipwillholdforallvaluesofPandQotherthanthefivegiven.Similarly,theremustbeaclearrelationshipbetweendemandandmarginalcost,usuallysatisfiedbyconstantvariablecostperunitandconstantfixedcosts.Thechangingvariablecostsperunitagaincomplicatetheissue,butitisthechangesinfixedcostswhichmakethealgebraicmethodlessusefulinJewel’scase.Thealgebraicmodelisonlysuitableforcompaniesoperatinginamonopolyanditisnotclearherewhetherthisisthecase,butitseemsunlikely,soany‘optimum’pricemightbecomeirrelevantifJewel’scompetitorschargesignificantlylowerprices.Othermoregeneralfactorsnotconsideredbythealgebraicmodelarepoliticalfactorswhichmightaffectimports,socialfactorswhichmayaffectcustomertastesandeconomicfactorswhichmayaffectexchangeratesorcustomerspendingpower.Thereliabilityoftheestimatesthemselves–forsalesprices,variablecostsandfixedcosts–couldalsobecalledintoquestion.

(c) Mentoring. (3 marks)

(c) Mentoring, not to be confused with coaching, involves training on a wider range of activities, often aimed at career development of employees at supervisory or management level. The trainee is provided with a development programme and is under close supervision. The mentor should not be the trainee’s immediate supervisor or manager.

(c) Lamont owns a residential apartment above its head office. Until 31 December 2006 it was let for $3,000 a

month. Since 1 January 2007 it has been occupied rent-free by the senior sales executive. (6 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Lamont Co for the year ended

31 March 2007.

NOTE: The mark allocation is shown against each of the three issues.

(c) Rent-free accommodation

(i) Matters

■ The senior sales executive is a member of Lamont’s key management personnel and is therefore a related party.

■ The occupation of Lamont’s residential apartment by the senior sales executive is therefore a related party

transaction, even though no price is charged (IAS 24 Related Party Disclosures).

■ Related party transactions are material by nature and information about them should be disclosed so that users of

financial statements understand the potential effect of related party relationships on the financial statements.

■ The provision of ‘housing’ is a non-monetary benefit that should be included in the disclosure of key management

personnel compensation (within the category of short-term employee benefits).

■ The financial statements for the year ended 31 March 2007 should disclose the arrangement for providing the

senior sales executive with rent-free accommodation and its fair value (i.e. $3,000 per month).

Tutorial note: Since no price is charged for the transaction, rote-learned disclosures such as ‘the amount of outstanding

balances’ and ‘expense recognised in respect of bad debts’ are irrelevant.

(ii) Audit evidence

■ Physical inspection of the apartment to confirm that it is occupied.

■ Written representation from the senior sales executive that he is occupying the apartment free of charge.

■ Written representation from the management board confirming that there are no related party transactions requiring

disclosure other than those that have been disclosed.

■ Inspection of the lease agreement with (or payments received from) the previous tenant to confirm the $3,000

monthly rental value.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-04-18

- 2020-01-10

- 2020-01-01

- 2021-02-26

- 2020-01-10

- 2019-03-29

- 2020-01-10

- 2020-04-22

- 2020-01-10

- 2020-05-21

- 2020-01-10

- 2020-01-30

- 2020-01-10

- 2020-01-10

- 2019-01-04

- 2020-01-10

- 2020-04-21

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-05-14

- 2020-01-09

- 2020-01-10

- 2020-08-16

- 2020-03-12

- 2020-01-10