ACCA能读研究生吗?我是学区域经济学的

发布时间:2021-12-30

ACCA能读研究生吗?我是学区域经济学的

最佳答案

我也是学区域经济学的,事实上考研收生就是供求关系, ACCA 考试的难度是以英国大学学位考试的难度为标准, 具体而言, 第一、第二部分的难度分别相当于学士学位高年级课程的考试难度, 第三部分的考试相当于硕士学位最后阶段的考试。第一部分 的每门考试只是测试本门课程所包含的知识, 着重于为后两个部分中实务性的课程所要运用的理论和技能打下基础。第二部分 的考试除了本门课程的内容之外, 还会考到第一部分的一些知识, 着重培养学员的分析能力。第三部分 的考试要求学员综合运用学到的知识、技能和决断力。不仅会考到以前的课程内容, 还会考到邻近科目的内容。

全球单科通过率基本在 30-40% 左右, 中国学员通过率为50-60% 。我国目前有3000名左右ACCA会员。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(ii) Using the previous overhead allocation basis (as per note 4), calculate the budgeted profit/(loss)

attributable to each type of service for the year ending 31 December 2006 and comment on the results

obtained using the previous and revised methods of overhead allocation. (5 marks)

Roy Crawford has argued for a reduction in both the product range and customer base to improve company

performance.

(b) Assess the operational advantages and disadvantages to Bonar Paint of choosing such a strategy.

(15 marks)

(b) Divestment of products or parts of the business is one of the most difficult strategic decisions. As apparent in Bonar Paint a

reduction in the products and customers served by the firm is likely to cause significant changes to the firm’s value chain and

system. Currently Bonar Paint supplies its customers, regardless of size, directly and this inevitably means that their

distribution costs are increased. The reduction in products and customers may allow a choice to be made about the costs of

supplying customers directly as against using distributors to handle the smaller customers.

In using the value chain one is looking to identify the significant cost activities and how those costs behave. Some costs may

be affected by the overall size of the firm e.g. advertising while others affected by the batch size being processed. The changeto fewer products will lead to a bigger batch size and a number of positive consequences for costs. The value chain’s major

benefit is in identifying and quantifying the links that exist between various activities within the firm and between the firm

and its customers and suppliers. In Bonar Paint’s case does a reduction in product range lead to less product failures and

consequent warranty claims? Does simplifying the product range lead to shorter lead times and better delivery time

performance for its customers? Above all, a good understanding of its value chain will let it know if it changes an activity what

are the consequences for other parts of the system.

In terms of reducing the product range, before such a decision is taken Bonar Paint must carry out a thorough analysis of the

pattern of customer demand for each paint type. In all probability it will find that 80% of its sales come from 20% of its

product range. Having given this qualification, reducing the product range can have a number of beneficial results on other

parts of the value chain. The immediate effect is likely to be that Bonar Paint produces fewer batches over a given time period

but produces them in larger quantities. This will bring cost savings but the impact on other parts of the value chain is equally

important. The beneficial effects are:

– With a smaller product range the control of raw materials and finished inventory will be simplified affecting inbound and

outbound logistics. This will improve the inventory turn and make for better product availability.

– With an improved inventory turn this will reduce the firm’s working capital needs and release significant amounts of

cash.

– A simpler operations process should facilitate staff savings and support more automation.

– Warranty claims and support costs could be reduced.

– Bonar Paint will be purchasing fewer raw materials but in greater volume and on a more regular basis. This will lead to

improved price and delivery terms from its suppliers.

– Bonar Paint can offer improved product reliability and better delivery to its customers and should improve its market

share.

In terms of operational disadvantages, these therefore are largely in terms of the impact on customer service levels seen in

terms of product range availability. Once again it is important to have accurate information on the sales and profitability of

each product so informed divestment decisions could be taken. Care must be taken to identify any paints, which though

ordered infrequently, and in small quantities are a pre-cursor for customers ordering other paints. Some important customers

may require that the full range of their paint needs are met in order to continue buying from Bonar Paint.

Reduction of the product range and customer base is an important strategic decision. Eliminating non-contributors or ‘dog’

products both in terms of paints and customers is a key part of managing the product portfolio. However, inertia both in terms

of products and customers is a real strategic weakness. In terms of the three tests of suitability, acceptability and feasibility

the analysis suggests that only acceptability is likely to be an issue. Tony Edmunds needs to be convinced that it is an

appropriate strategy to adopt. It is the lack of accurate sales analysis that lies at the heart of the problem and that is his areaof responsibility!

3 (a) Financial statements often contain material balances recognised at fair value. For auditors, this leads to additional

audit risk.

Required:

Discuss this statement. (7 marks)

3 Poppy Co

(a) Balances held at fair value are frequently recognised as material items in the statement of financial position. Sometimes it is

required by the financial reporting framework that the measurement of an asset or liability is at fair value, e.g. certain

categories of financial instruments, whereas it is sometimes the entity’s choice to measure an item using a fair value model

rather than a cost model, e.g. properties. It is certainly the case that many of these balances will be material, meaning that

the auditor must obtain sufficient appropriate evidence that the fair value measurement is in accordance with the

requirements of financial reporting standards. ISA 540 (Revised and Redrafted) Auditing Accounting Estimates Including Fair

Value Accounting Estimates and Related Disclosures and ISA 545 Auditing Fair Value Measurements and Disclosures

contain guidance in this area.

As part of the understanding of the entity and its environment, the auditor should gain an insight into balances that are stated

at fair value, and then assess the impact of this on the audit strategy. This will include an evaluation of the risk associated

with the balance(s) recognised at fair value.

Audit risk comprises three elements; each is discussed below in the context of whether material balances shown at fair value

will lead to increased risk for the auditor.

Inherent risk

Many measurements based on estimates, including fair value measurements, are inherently imprecise and subjective in

nature. The fair value assessment is likely to involve significant judgments, e.g. regarding market conditions, the timing of

cash flows, or the future intentions of the entity. In addition, there may be a deliberate attempt by management to manipulate

the fair value to achieve a desired aim within the financial statements, in other words to attempt some kind of window

dressing.

Many fair value estimation models are complicated, e.g. discounted cash flow techniques, or the actuarial calculations used

to determine the value of a pension fund. Any complicated calculations are relatively high risk, as difficult valuation techniques

are simply more likely to contain errors than simple valuation techniques. However, there will be some items shown at fair

value which have a low inherent risk, because the measurement of fair value may be relatively straightforward, e.g. assets

that are regularly bought and sold on open markets that provide readily available and reliable information on the market prices

at which actual exchanges occur.

In addition to the complexities discussed above, some fair value measurement techniques will contain significant

assumptions, e.g. the most appropriate discount factor to use, or judgments over the future use of an asset. Management

may not always have sufficient experience and knowledge in making these judgments.

Thus the auditor should approach some balances recognised at fair value as having a relatively high inherent risk, as their

subjective and complex nature means that the balance is prone to contain an error. However, the auditor should not just

assume that all fair value items contain high inherent risk – each balance recognised at fair value should be assessed for its

individual level of risk.

Control risk

The risk that the entity’s internal monitoring system fails to prevent and detect valuation errors needs to be assessed as part

of overall audit risk assessment. One problem is that the fair value assessment is likely to be performed once a year, outside

the normal accounting and management systems, especially where the valuation is performed by an external specialist.

Therefore, as a non-routine event, the assessment of fair value is likely not to have the same level of monitoring or controls

as a day-to-day business transaction.

However, due to the material impact of fair values on the statement of financial position, and in some circumstances on profit,

management may have made great effort to ensure that the assessment is highly monitored and controlled. It therefore could

be the case that there is extremely low control risk associated with the recognition of fair values.

Detection risk

The auditor should minimise detection risk via thorough planning and execution of audit procedures. The audit team may

lack experience in dealing with the fair value in question, and so would be unlikely to detect errors in the valuation techniques

used. Over-reliance on an external specialist could also lead to errors not being found.

Conclusion

It is true that the increasing recognition of items measured at fair value will in many cases cause the auditor to assess the

audit risk associated with the balance as high. However, it should not be assumed that every fair value item will be likely to

contain a material misstatement. The auditor must be careful to identify and respond to the level of risk for fair value items

on an individual basis to ensure that sufficient and appropriate evidence is gathered, thus reducing the audit risk to an

acceptable level.

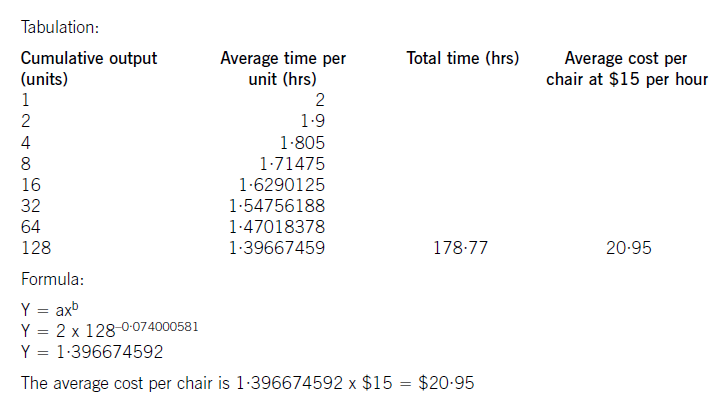

Big Cheese Chairs (BCC) manufactures and sells executive leather chairs. They are considering a new design of massaging chair to launch into the competitive market in which they operate.

They have carried out an investigation in the market and using a target costing system have targeted a competitive selling price of $120 for the chair. BCC wants a margin on selling price of 20% (ignoring any overheads).

The frame. and massage mechanism will be bought in for $51 per chair and BCC will upholster it in leather and assemble it ready for despatch.

Leather costs $10 per metre and two metres are needed for a complete chair although 20% of all leather is wasted in the upholstery process.

The upholstery and assembly process will be subject to a learning effect as the workers get used to the new design.

BCC estimates that the first chair will take two hours to prepare but this will be subject to a learning rate (LR) of 95%.

The learning improvement will stop once 128 chairs have been made and the time for the 128th chair will be the time for all subsequent chairs. The cost of labour is $15 per hour.

The learning formula is shown on the formula sheet and at the 95% learning rate the value of b is -0·074000581.

Required:

(a) Calculate the average cost for the first 128 chairs made and identify any cost gap that may be present at

that stage. (8 marks)

(b) Assuming that a cost gap for the chair exists suggest four ways in which it could be closed. (6 marks)

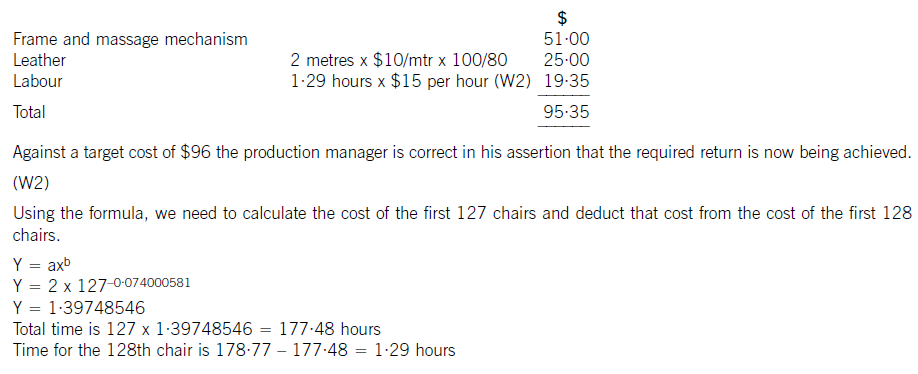

The production manager denies any claims that a cost gap exists and has stated that the cost of the 128th chair will be low enough to yield the required margin.

(c) Calculate the cost of the 128th chair made and state whether the target cost is being achieved on the 128th chair. (6 marks)

(W1)

The cost of the labour can be calculated using learning curve principles. The formula can be used or a tabular approach would

also give the average cost of 128 chairs. Both methods are acceptable and shown here.

(b) To reduce the cost gap various methods are possible (only four are needed for full marks)

– Re-design the chair to remove unnecessary features and hence cost

– Negotiate with the frame. supplier for a better cost. This may be easier as the volume of sales improve as suppliers often

are willing to give discounts for bulk buying. Alternatively a different frame. supplier could be found that offers a better

price. Care would be needed here to maintain the required quality

– Leather can be bought from different suppliers or at a better price also. Reducing the level of waste would save on cost.

Even a small reduction in waste rates would remove much of the cost gap that exists

– Improve the rate of learning by better training and supervision

– Employ cheaper labour by reducing the skill level expected. Care would also be needed here not to sacrifice quality or

push up waste rates.

(c) The cost of the 128th chair will be:

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2021-05-19

- 2021-03-12

- 2021-05-21

- 2021-03-12

- 2021-02-14

- 2021-12-17

- 2021-01-04

- 2021-03-10

- 2021-04-15

- 2021-04-21

- 2021-03-11

- 2021-12-31

- 2021-01-04

- 2021-12-30

- 2021-03-10

- 2021-11-06

- 2021-03-10

- 2021-03-11

- 2021-03-12

- 2021-03-12

- 2021-03-10

- 2021-04-15

- 2021-07-15

- 2021-02-15

- 2021-03-12

- 2021-01-04

- 2021-03-13

- 2021-03-12

- 2021-03-10

- 2021-03-11