ACCA考完后需要注册和继续教育吗?怎么操作?

发布时间:2020-02-29

虽然近年来ACCA考试热度逐渐上升,但是仍然有部分小伙伴对证书注册的相关信息并不了解。比如,有网友就在询问ACCA考完后需要注册和继续教育吗?怎么操作。鉴于此,51题库考试学习网在下面为大家带来2020年ACCA会员注册的相关信息,以供参考。

注册成为ACCA会员后并不需要继续教育,每年按时缴纳年费即可保持会员身份。申请ACCA会员注册的材料比较简单,首先是ACCA准会员资格:当你学完了ACCA的所有课程,且通过了考试,就能获得准会员资格。其次,需要在线完成相应的Professionalism and ethics学习和测试,还必须具备三年及以上的工作经验,才可以进行申请。提交申请后,需要通过审核才能正式成为ACCA会员。

具体申请流程为:登录ACCA网站下载并填写《ACCA会员申请表》,并在满足会员必要条件后向ACCA递交ACCA会员申请表。ACCA总部会对申请人进行资料审核,审核通过后,会为申请人颁发ACCA会员证书,一般这个过程需要两个月的时间。等拿到证书后,小伙伴们就是正式的ACCA会员了。

值得一提的是,成为会员约五年后,可向ACCA总部申请称为资深会员(FCCA),具体要求还请各位考生咨询ACCA官网。

以上就是关于ACCA会员申请的相关情况。51题库考试学习网提醒:如果未按时缴纳年费,会导致ACCA账户被冻,请各位考生注意。最后,51题库考试学习网预祝准备参加2020年ACCA考试的小伙伴都能顺利通过。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

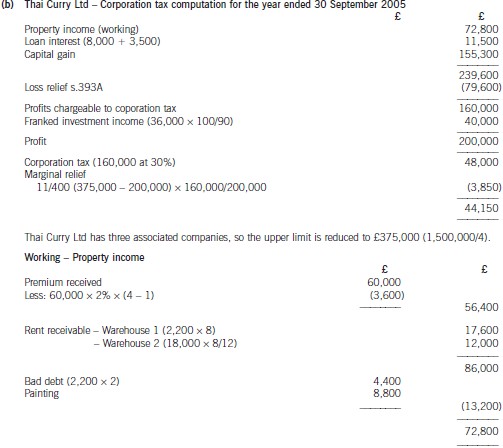

(b) Assuming that Thai Curry Ltd claims relief for its trading loss against total profits under s.393A ICTA 1988,calculate the company’s corporation tax liability for the year ended 30 September 2005. (10 marks)

6 Certain practices have developed that threaten to damage the integrity and objectivity of professional accountants and

the reputation of the accounting profession.

Required:

Explain the following practices and associated ethical risks and discuss whether current ethical guidance is

sufficient:

(a) ‘lowballing’; (5 marks)

6 CERTAIN PRACTICES

Tutorial note: The answer which follows is indicative of the range of points which might be made. Other relevant material will

be given suitable credit.

(a) ‘Lowballing’

Explanation of term

‘Lowballing’ is the ‘loss-leading’ practice in which auditors compete for clients by reducing their fees for statutory audits.

Lower audit fees are then compensated by the auditor carrying out more lucrative non-audit work (e.g. consultancy and tax

advice). Audits may even be offered for free.

Such ‘predatory pricing’ may undercut an incumbent auditor to secure an appointment into which higher price consultancy

services may be sold.

Ethical risks

There is a risk of incompetence if the non-audit work does not materialise and the lowballing firm comes under pressure to

cut corners or resort to irregular practices (e.g. the falsification of audit working papers) in order to ‘keep within budget’.

However, a lack of audit quality may only be discovered if the situation arises that the company collapses and the auditors

are charged with negligence.

If, rather than comprise the quality of the audit, an audit firm substantially increases audit fees, a fee dispute could arise. In

this case the client might refuse to pay the higher fee. It could be difficult then for the firm to take the matter to arbitration

if the client was misled. Thus an advocacy threat may arise.

Financial dependence is a direct incentive that threatens independence. A self-interest threat therefore arises when, having

secured the audit, the audit firm needs the client to retain its services in order to recoup any losses initially incurred.

The provision of many other services gives rise to a self-review threat (as well as a self-interest threat).

Sufficiency of current ethical guidance

In current ethical guidance, the fact that an accountancy firm quotes a lower fee than other tendering firms is not improper,

providing that the prospective client is not misled about:

– the precise range of services that the quoted fee is intended to cover; and

– the likely level of fees for any other work undertaken.

This is clearly insufficient to prevent the practice of lowballing.

Legal prohibitions on the provision of many non-audit services (e.g. bookkeeping, financial information systems design and

implementation, valuation services, actuarial services, internal audit (outsourced), human resource services for executive

positions, investment and legal services) should make lowballing a riskier pricing strategy. This may curb the tendency to

lowball.

Lowballing could be eliminated if, for example, auditors were required to act ‘exclusively as auditors’. Although regulatory

environments have moved towards this there is not a total prohibition on non-audit services.

(c) Explain the possible impact of RBG outsourcing its internal audit services on the audit of the financial

statements by Grey & Co. (4 marks)

(c) Impact on the audit of the financial statements

Tutorial note: The answer to this part should reflect that it is not the external auditor who is providing the internal audit

services. Thus comments regarding objectivity impairment are not relevant.

■ As Grey & Co is likely to be placing some reliance on RBG’s internal audit department in accordance with ISA 610

Considering the Work of Internal Auditing the degree of reliance should be reassessed.

■ The appointment will include an evaluation of organisational risk. The results of this will provide Grey with evidence,

for example:

– supporting the appropriateness of the going concern assumption;

– of indicators of obsolescence of goods or impairment of other assets.

■ As the quality of internal audit services should be higher than previously, providing a stronger control environment, the

extent to which Grey may rely on internal audit work could be increased. This would increase the efficiency of the

external audit of the financial statements as the need for substantive procedures should be reduced.

■ However, if internal audit services are performed on a part-time basis (e.g. fitting into the provider’s less busy months)

Grey must evaluate the impact of this on the prevention, detection and control of fraud and error.

■ The internal auditors will provide a body of expertise within RBG with whom Grey can consult on contentious matters.

Tutorial note: Appropriate credit will be given for arguing that less reliance may be placed on internal audit in this year of

change of provider.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2019-07-20

- 2020-01-09

- 2019-07-20

- 2020-01-09

- 2020-01-09

- 2019-07-20

- 2020-01-09

- 2020-01-09

- 2020-02-29

- 2020-09-04

- 2020-05-20

- 2019-07-20

- 2020-09-04

- 2019-07-20

- 2020-02-29

- 2020-01-09

- 2020-09-04

- 2020-02-29

- 2020-04-22

- 2020-02-29

- 2020-01-09

- 2019-07-20

- 2020-02-29

- 2020-01-09

- 2020-01-03

- 2020-01-09

- 2019-07-20

- 2020-02-29

- 2019-07-20

- 2019-07-20