ACCA证书注册及领取知识!

发布时间:2019-07-20

2019年6月ACCA考试已经结束,很多小伙伴已经开始准备9月份的考试了,但是尽管已经考过ACCA一个科目或者几个科目很多小伙伴对于ACCA的证书注册地信息仍不了解,ACCA在哪注册?ACCA注册后究竟有什么用?ACCA可以领取哪些证书?这些知识点相信很多小伙伴都不是太了解吧,为此小编特地整理了如下内容。

一、ACCA注册简介

ACCA是"英国特许公认会计师公会(The Association of Chartered Certified Accountants)的简称,是世界上领先的专业会计师团体,也是国际学员最多、学员规模发展最快的专业会计师组织。ACCA会员资格得到欧盟立法以及许多国家公司法的承认。

英国特许公认会计师公会(The Association of Chartered

Certified Accountants)简称ACCA,成立于1904年,是世界上领先的专业会计师团体,也是国际学员最多、学员规模发展最快的专业会计师组织。ACCA总部设在伦敦,在美国洛杉矶、加拿大多伦多、澳大利亚悉尼建有分会,在世界上70多个城市均设有办事处。

ACCA为全世界有志投身于财务、会计以及管理领域的专才提供首选的资格认证,一贯坚持最高的标准,提高财会人员的专业素质,职业操守以及监管能力,并秉承为公众利益服务的原则。

在英国,英国立法许可ACCA会员从事审计、投资顾问和破产执行的工作。ACCA会员资格得到欧盟立法以及许多国家公司法的承认。ACCA在欧洲会计专家协会(FEE)、亚太会计师联合会(CAPA)和加勒比特许会计师协会(ICAC)等会计组织中起着非常重要的作用。在国际上,ACCA是国际会计准则理事会(IASB)的创始成员,也是国际会计师联合会(IFAC)的成员。

二、ACCA证书

其实,每个阶段完成后,ACCA官方协会都会颁发相应的证书鼓励ACCA考试小伙伴继续考下去,同时这些证书都可以帮助你找实习找工作、升职加薪、申请国外留学等等

商业会计证书

当学员完成Knowledge部分——Accounting

in Business, Management Accounting, Financial Accounting这三门考试,并且通过基础阶段道德测试,即可获得商业会计证书。如已免试,无法获得此证书。

高级商业会计证书

当学员完成Skill部分——LW, PM,

TX, FR, AA, FM六门考试,并且完成道德测试模块,即可获得高级商业会计证书。如全部免试将无法获得此证书。

牛津布鲁克斯大学学士学位

考完ACCA前9门可申请英国牛津布鲁克斯大学应用会计学学士学位,想要申请学位需要提前提交英语成绩证明,并且写一篇英文论文,通过后即可获得此学位。

牛津布鲁克斯大学硕士学位

13门全部通过以后将有机会申请牛津布鲁克斯大学MBA硕士学位,需要去英国学习答辩,论文答辩通过即可获得硕士学位。

ACCA会员证书

通过13门考试,即可获得ACCA准会员证书。累计三年工作经验,即可申请转为正式ACCA member。

综上所述就是关于ACCA注册信息以及证书领取的全部内容希望对于各位正在备考的小伙伴们有帮助,小编将持续更新ACCA相关资讯。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(c) Explain the reasons for the concerns of the government of Happyland with companies such as TMC and

advise the directors of a strategy that might be considered in order to avoid being subject to any forthcoming

legislation concerning the environment. (5 marks)

(c) The government of Happyland will be concerned by the negative impact on the environment. The growth in the number of

children born in Happyland will have raised the demand for disposable nappies as is evidenced from the market size data

contained in the question. In some countries disposable nappies make up around 4% of all household waste and can take

up to five hundred years to decompose! The government will be concerned by the fact that trees are being destroyed in order

to keep babies and infant children in nappies. The disposal costs incurred by the government in terms of landfill etc will be

very high, hence its green paper on the effect of non-biodegradable products in Happyland. The costs of such operations as

the landfill for such products will need to be funded out of increased taxation.

It might be beneficial for the directors of TMC to develop more eco-friendly products such as washable nappies which, by

definition, are recyclable many times over during the life of the ‘product’. Many parents are now changing to ‘real nappies’

because they work out cheaper and better for the environment than disposables.

10 What would the company’s profit become after the correction of the above errors?

A $634,760

B $624,760

C $624,440

D $625,240

630,000 – 4,320 – 440

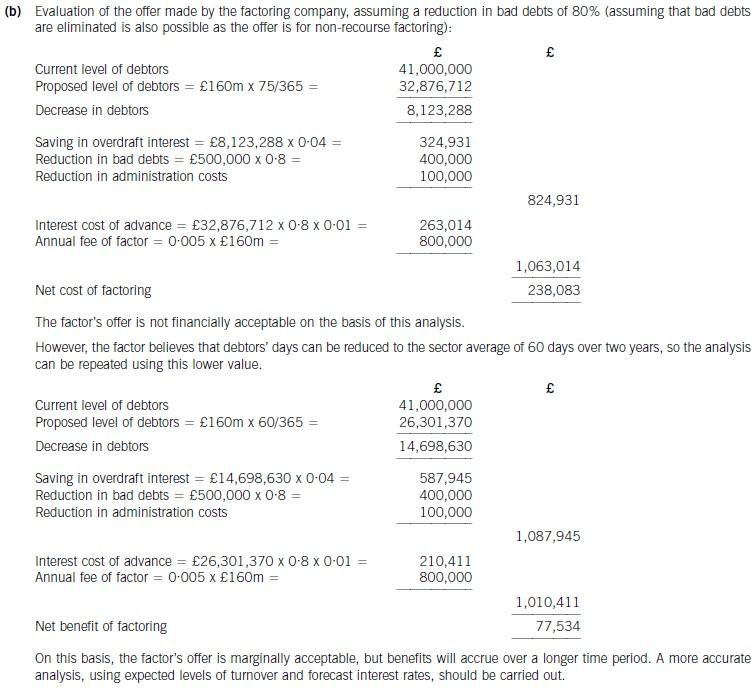

(b) Determine whether the factoring company’s offer can be recommended on financial grounds. Assume a

working year of 365 days and base your analysis on financial information for 2006. (8 marks)

(b) Provide the directors of Acrux Ltd with a detailed explanation of the maximum rate of tax that will be suffered

on both the distributed and non-distributed profits of the non-UK resident investee companies where:

(1) there is a double tax treaty between the UK and the country in which the individual companies are

resident; and

(2) there is no such double tax treaty.

Note: you are not required to explain the position of the overseas resident branches. (6 marks)

(b) Rate of tax on profits of non-UK resident investee companies

Undistributed profits

The companies will be subject to tax in the countries in which they are resident; this is because of their residency status or

because they have a permanent establishment in that country. Undistributed profits will not be taxed in the UK.

The rate of tax on undistributed profits will therefore be the rate of tax in the country of residency of the respective companies.

Distributed profits with double tax treaty

The dividends received by Acrux Ltd from each of the overseas companies will be grossed up in respect of underlying tax (the

overseas corporation tax paid on the distributed profits) because Acrux Ltd will own at least 10% of the overseas companies.

The gross amount will then be included in Acrux Ltd’s profits chargeable to corporation tax.

The treaty will provide double tax relief in the UK for the overseas tax suffered in respect of each dividend up to a maximum

of the UK tax on the grossed up overseas dividend. As a result of the double tax relief, the overall rate of tax suffered will be

the higher of the UK rate paid by Acrux Ltd and the overseas tax rate borne by the overseas company.

Where the rate of overseas tax in respect of a particular dividend exceeds the rate of corporation tax in the UK, excess foreign

tax will arise. This can be relieved, via onshore pooling, against the UK tax due on those dividends where the rate of tax in

the UK exceeds the rate overseas. This will reduce the overall rate of tax suffered on the total overseas profits of the overseas

companies as a whole.

Distributed profits with no double tax treaty

Where there is no double tax treaty, unilateral double tax relief will be available in the UK. This relief will operate in the same

way as double tax relief under a double tax treaty such that the overall rate of tax on each dividend will be the higher of the

UK rate paid by Acrux Ltd and the overseas rate borne by the overseas company. Relief via onshore pooling will also be

available.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-02-29

- 2020-02-29

- 2019-07-20

- 2020-01-09

- 2019-07-20

- 2019-07-20

- 2019-07-20

- 2020-01-09

- 2020-05-20

- 2020-01-09

- 2021-05-27

- 2020-01-09

- 2019-07-20

- 2019-07-20

- 2020-02-29

- 2020-01-09

- 2020-03-08

- 2020-02-29

- 2020-04-22

- 2020-01-09

- 2020-01-09

- 2019-07-20

- 2020-02-29

- 2020-03-08

- 2019-07-20

- 2020-03-08

- 2020-09-04

- 2020-01-09

- 2020-02-29

- 2019-07-20