CMA和ACCA在全球哪个更具有影响力?

发布时间:2021-07-28

CMA和ACCA分别属于管理会计和财务会计两个不同范畴的国际知名专业认证,都具有影响力没有可比性。ACCA培养的主要方向是财务会计和审计方向,虽然也涉及管理会计内容但不是其重点。ACCA的优势在于对财务会计所有领域全面覆盖,而且研究深入,对英国的财务会计准则也花费大量篇幅研究,完成ACCA的认证完全具备财务会计领域的中高级职位的知识结构要求。主要看的是是否适合你自己的职业发展,ACCA更侧重财务会计和审计,如果向审计领域发展,具备ACCA证书是非常有用的。

ACCA的劣势有两方面,一:财务会计主要是依据各国不同的财务会计准则,ACCA依据的英国财务会计准则应用面有限,但由于英国同欧盟的融合,国际财务会计准则也已经部分的适用于英国企业,而英国财务会计准则并不能通行欧洲。美国又认为自己地位领先,始终倾向于使用美国财务会计准则,中国的财务会计准则与欧洲和美国准则还是有较大的差异。在这种背景下,ACCA的知识结构和内容应用领域不够宽广,其实企业更看中的是ACCA学员的学习能力,而非ACCA学员实际学到的东西。值得说明的是在英国国内,更为广泛认可的财务会计和审计认证资格是英国皇家特许会计师(ACA),而非ACCA。

二:ACCA课程总计16门,课程难度也非常大,全部学完通常需要四年及以上,对于四年的紧张生活对于人生来说也是一种煎熬,具会计师视野网站的调查统计,竟有83%的学员中途放弃,使人遗憾这些学员当初的草率决定和大笔金钱投入。

CMA的优势在于它代表着会计发展的方向,不论你选择财务会计、审计、税务、成本、预算、资金或是其它会计模块,随着职业发展,必定会走入管理会计领域,并很可能因在管理会计领域卓有成效的工作,最终走向最高管理层。同时CMA课程设置比较简单:四门课其中三门课程考试都是选择题,考试时间较灵活,只要自己学完有把握通过,随时可以约考,CMA全球学员的通过率在50%以上,平均通过时间只需一年左右。CMA的劣势在于,虽然其美誉度很高,但在中国知名度不高,其知名度在外资中高层才有较强的体现。但也正因如此,CMA目前在中国还十分稀缺,欧美公司中高层职位对CMA认证会员的需求极高。

今天关于CMA和ACCA在全球哪个更具有影响力的分享就到这里了,想要了解更多资讯,敬请关注51题库考试学习网!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(c) What changes to Churchill’s existing marketing mix will be needed to achieve the three strategic goals?

(15 marks)

(c) Each of the strategic goals will have a profound impact on the marketing mix as it currently exists. As each goal affects the

market position of Churchill developing an appropriate marketing mix will be the key to successful implementation of the

overall growth strategy. The product, the brand and the reputation it creates are at the heart of the company’s marketing

strategy. Their focus on the premium segment of the market seems a sensible one and one which allows a small family-owned

business to survive and grow slowly. Evidence suggests this is a luxury indulgence market reflecting changing consumer tastes

and lifestyles. Managing the product range will be a major marketing activity. While the core products may develop an almost

timeless quality there will be a need to respond to the product innovations introduced by its much larger competitors. The

company’s emphasis on the quality of its products resulting from the quality of its ingredients is at the heart of its competitive

advantage. Growing the product range will also bring the danger of under performing products and a consequent need to

divest such products. Packaging is likely to be a key part of the products’ appeal and will be an area where constant innovation

is important.

Pricing raises a number of issues. Why is Churchill’s core product priced at £1 less than its immediate competition? What is

the basis on which Churchill prices this product? Each of the methods of pricing has its advantages and disadvantages. Using

cost plus may create an illusion of security in that all costs are covered, but at the same time raises issues as to whether

relevant costs have been included and allocated. Should the company price in anticipation of cost reductions as volume

increases? Should the basis for pricing be what your competitors are charging? As a luxury product one would assume that

its demand is relatively price inelastic: a significant increase in price e.g. £1 would lead to only a small reduction in quantity

demanded. Certainly, profit margins would be enhanced to help provide the financial resources the company needs if it is to

grow. One interesting issue on pricing is the extent to which it is pursuing a price skimming or price penetration policy –

evidence from the scenario suggests more of a price skimming policy in line with the luxury nature of the product.

Place is an equally important issue – the vertical integration strategy of the company has led to company-owned shops being

the main way customers can buy the product. At the same time, this distribution strategy has led to Churchill’s sales being

largely confined to one region in the UK – although it is the most populous. If Churchill has a desire to grow, does it do this

through expanding the number of company owned and franchised outlets or look for other channels of distribution in

particular the increasingly dominant supermarket chains? Each distribution strategy will have significant implications for other

elements in the marketing mix and for the resources and capabilities required in the company.

Finally, promotion is an interesting issue for the company. The relatively recent appointment of a sales and marketing director

perhaps reflects a need to balance the previous dominance of the manufacturing side of the business. Certainly there is

evidence to suggest that John Churchill is not convinced of the need to advertise. There are some real concerns about how

the brand is developed and promoted. Certainly sponsorship is now seen as a key part of the firm’s promotional strategy. The

company has a good reputation but customer access to the product is fairly limited. Overall there is scope for the company

to critically review its marketing mix and implement a very different mix if it wants to grow.

The four Ps above are very much the ‘hard’ elements in the marketing mix and Churchill in its desire to grow will need toensure that the ‘softer’ elements of people, physical evidence and processes are aligned to its ambitious strategy.

(a) The following figures have been calculated from the financial statements (including comparatives) of Barstead for

the year ended 30 September 2009:

increase in profit after taxation 80%

increase in (basic) earnings per share 5%

increase in diluted earnings per share 2%

Required:

Explain why the three measures of earnings (profit) growth for the same company over the same period can

give apparently differing impressions. (4 marks)

(b) The profit after tax for Barstead for the year ended 30 September 2009 was $15 million. At 1 October 2008 the company had in issue 36 million equity shares and a $10 million 8% convertible loan note. The loan note will mature in 2010 and will be redeemed at par or converted to equity shares on the basis of 25 shares for each $100 of loan note at the loan-note holders’ option. On 1 January 2009 Barstead made a fully subscribed rights issue of one new share for every four shares held at a price of $2·80 each. The market price of the equity shares of Barstead immediately before the issue was $3·80. The earnings per share (EPS) reported for the year ended 30 September 2008 was 35 cents.

Barstead’s income tax rate is 25%.

Required:

Calculate the (basic) EPS figure for Barstead (including comparatives) and the diluted EPS (comparatives not required) that would be disclosed for the year ended 30 September 2009. (6 marks)

(a)Whilstprofitaftertax(anditsgrowth)isausefulmeasure,itmaynotgiveafairrepresentationofthetrueunderlyingearningsperformance.Inthisexample,userscouldinterpretthelargeannualincreaseinprofitaftertaxof80%asbeingindicativeofanunderlyingimprovementinprofitability(ratherthanwhatitreallyis:anincreaseinabsoluteprofit).Itispossible,evenprobable,that(someof)theprofitgrowthhasbeenachievedthroughtheacquisitionofothercompanies(acquisitivegrowth).Wherecompaniesareacquiredfromtheproceedsofanewissueofshares,orwheretheyhavebeenacquiredthroughshareexchanges,thiswillresultinagreaternumberofequitysharesoftheacquiringcompanybeinginissue.ThisiswhatappearstohavehappenedinthecaseofBarsteadastheimprovementindicatedbyitsearningspershare(EPS)isonly5%perannum.ThisexplainswhytheEPS(andthetrendofEPS)isconsideredamorereliableindicatorofperformancebecausetheadditionalprofitswhichcouldbeexpectedfromthegreaterresources(proceedsfromthesharesissued)ismatchedwiththeincreaseinthenumberofshares.Simplylookingatthegrowthinacompany’sprofitaftertaxdoesnottakeintoaccountanyincreasesintheresourcesusedtoearnthem.Anyincreaseingrowthfinancedbyborrowings(debt)wouldnothavethesameimpactonprofit(asbeingfinancedbyequityshares)becausethefinancecostsofthedebtwouldacttoreduceprofit.ThecalculationofadilutedEPStakesintoaccountanypotentialequitysharesinissue.Potentialordinarysharesarisefromfinancialinstruments(e.g.convertibleloannotesandoptions)thatmayentitletheirholderstoequitysharesinthefuture.ThedilutedEPSisusefulasitalertsexistingshareholderstothefactthatfutureEPSmaybereducedasaresultofsharecapitalchanges;inasenseitisawarningsign.InthiscasethelowerincreaseinthedilutedEPSisevidencethatthe(higher)increaseinthebasicEPShas,inpart,beenachievedthroughtheincreaseduseofdilutingfinancialinstruments.Thefinancecostoftheseinstrumentsislessthantheearningstheirproceedshavegeneratedleadingtoanincreaseincurrentprofits(andbasicEPS);however,inthefuturetheywillcausemoresharestobeissued.ThiscausesadilutionwherethefinancecostperpotentialnewshareislessthanthebasicEPS.

5 (a) Compare and contrast the responsibilities of management, and of auditors, in relation to the assessment of

going concern. You should include a description of the procedures used in this assessment where relevant.

(7 marks)

5 Dexter Co

(a) Responsibilities of management and auditors

Responsibilities

ISA 570 Going Concern provides a clear framework for the assessment of the going concern status of an entity, and

differentiates between the responsibilities of management and of auditors. Management should assess going concern in order

to decide on the most appropriate basis for the preparation of the financial statements. IAS 1 Presentation of Financial

Statements (revised) requires that where there is significant doubt over an entity’s ability to continue as a going concern, the

uncertainties should be disclosed in a note to the financial statements. Where the directors intend to cease trading, or have

no realistic alternative but to do so, the financial statements should be prepared on a ‘break up’ basis.

Thus the main focus of the management’s assessment of going concern is to ensure that relevant disclosures are made where

necessary, and that the correct basis of preparation is used.

The auditor’s responsibility is to consider the appropriateness of the management’s use of the going concern assumption in

the preparation of the financial statements and to consider whether there are material uncertainties about the entity’s ability

to continue as a going concern that need to be disclosed in a note.

The auditor should also consider the length of the time period that management have looked at in their assessment of going

concern.

The auditor will therefore need to come to an opinion as to the going concern status of an entity but the focus of the auditor’s

evaluation of going concern is to see whether they agree with the assessment made by the management. Therefore whether

they agree with the basis of preparation of the financial statements, or the inclusion in a note to the financial statements, as

required by IAS 1, of any material uncertainty.

Evaluation techniques

In carrying out the going concern assessment, management will evaluate a wide variety of indicators, including operational

and financial. An entity employing good principles of corporate governance should be carrying out such an assessment as

part of the on-going management of the business.

Auditors will use a similar assessment technique in order to come to their own opinion as to the going concern status of an

entity. They will carry out an operational review of the business in order to confirm business understanding, and will conduct

a financial review as part of analytical procedures. Thus both management and auditors will use similar business risk

assessment techniques to discover any threats to the going concern status of the business.

Auditors should not see going concern as a ‘completion issue’, but be alert to issues affecting going concern throughout the

audit. In the same way that management should continually be managing risk (therefore minimising going concern risk),

auditors should be continually be alert to going concern problems throughout the duration of the audit.

However, one difference is that when going concern problems are discovered, the auditor is required by IAS 570 to carry out

additional procedures. Examples of such procedures would include:

– Analysing and discussing cash flow, profit and other relevant forecasts with management

– Analysing and discussing the entity’s latest available interim financial statements

– Reviewing events after the period end to identify those that either mitigate or otherwise affect the entity’s ability to

continue as a going concern, and

– Reading minutes of meetings of shareholders, those charged with governance and relevant committees for reference to

financing difficulties.

Management are not explicitly required to gather specific evidence about going concern, but as part of good governance would

be likely to investigate and react to problems discovered.

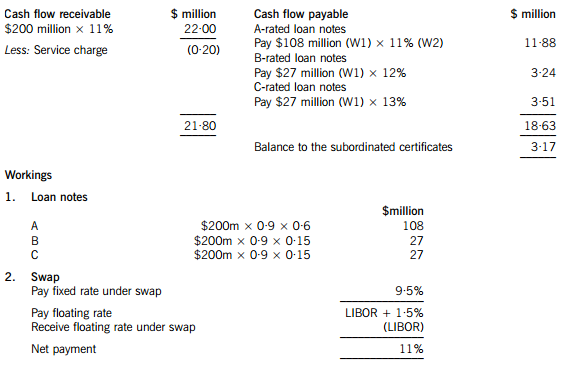

Moonstar Co is a property development company which is planning to undertake a $200 million commercial property development. Moonstar Co has had some difficulties over the last few years, with some developments not generating the expected returns and the company has at times struggled to pay its finance costs. As a result Moonstar Co’s credit rating has been lowered, affecting the terms it can obtain for bank finance. Although Moonstar Co is listed on its local stock exchange, 75% of the share capital is held by members of the family who founded the company. The family members who are shareholders do not wish to subscribe for a rights issue and are unwilling to dilute their control over the company by authorising a new issue of equity shares. Moonstar Co’s board is therefore considering other methods of financing the development, which the directors believe will generate higher returns than other recent investments, as the country where Moonstar Co is based appears to be emerging from recession.

Securitisation proposals

One of the non-executive directors of Moonstar Co has proposed that it should raise funds by means of a securitisation process, transferring the rights to the rental income from the commercial property development to a special purpose vehicle. Her proposals assume that the leases will generate an income of 11% per annum to Moonstar Co over a ten-year period. She proposes that Moonstar Co should use 90% of the value of the investment for a collateralised loan obligation which should be structured as follows:

– 60% of the collateral value to support a tranche of A-rated floating rate loan notes offering investors LIBOR plus 150 basis points

– 15% of the collateral value to support a tranche of B-rated fixed rate loan notes offering investors 12%

– 15% of the collateral value to support a tranche of C-rated fixed rate loan notes offering investors 13%

– 10% of the collateral value to support a tranche as subordinated certificates, with the return being the excess of receipts over payments from the securitisation process

The non-executive director believes that there will be sufficient demand for all tranches of the loan notes from investors. Investors will expect that the income stream from the development to be low risk, as they will expect the property market to improve with the recession coming to an end and enough potential lessees to be attracted by the new development.

The non-executive director predicts that there would be annual costs of $200,000 in administering the loan. She acknowledges that there would be interest rate risks associated with the proposal, and proposes a fixed for variable interest rate swap on the A-rated floating rate notes, exchanging LIBOR for 9·5%.

However the finance director believes that the prediction of the income from the development that the non-executive director has made is over-optimistic. He believes that it is most likely that the total value of the rental income will be 5% lower than the non-executive director has forecast. He believes that there is some risk that the returns could be so low as to jeopardise the income for the C-rated fixed rate loan note holders.

Islamic finance

Moonstar Co’s chief executive has wondered whether Sukuk finance would be a better way of funding the development than the securitisation.

Moonstar Co’s chairman has pointed out that a major bank in the country where Moonstar Co is located has begun to offer a range of Islamic financial products. The chairman has suggested that a Mudaraba contract would be the most appropriate method of providing the funds required for the investment.

Required:

(a) Calculate the amounts in $ which each of the tranches can expect to receive from the securitisation arrangement proposed by the non-executive director and discuss how the variability in rental income affects the returns from the securitisation. (11 marks)

(b) Discuss the benefits and risks for Moonstar Co associated with the securitisation arrangement that the non-executive director has proposed. (6 marks)

(c) (i) Discuss the suitability of Sukuk finance to fund the investment, including an assessment of its appeal to potential investors. (4 marks)

(ii) Discuss whether a Mudaraba contract would be an appropriate method of financing the investment and discuss why the bank may have concerns about providing finance by this method. (4 marks)

(a) An annual cash flow account compares the estimated cash flows receivable from the property against the liabilities within the securitisation process. The swap introduces leverage into the arrangement.

The holders of the certificates are expected to receive $3·17million on $18 million, giving them a return of 17·6%. If the cash flows are 5% lower than the non-executive director has predicted, annual revenue received will fall to $20·90 million, reducing the balance available for the subordinated certificates to $2·07 million, giving a return of 11·5% on the subordinated certificates, which is below the returns offered on the B and C-rated loan notes. The point at which the holders of the certificates will receive nothing and below which the holders of the C-rated loan notes will not receive their full income will be an annual income of $18·83 million (a return of 9·4%), which is 14·4% less than the income that the non-executive director has forecast.

(b) Benefits

The finance costs of the securitisation may be lower than the finance costs of ordinary loan capital. The cash flows from the commercial property development may be regarded as lower risk than Moonstar Co’s other revenue streams. This will impact upon the rates that Moonstar Co is able to offer borrowers.

The securitisation matches the assets of the future cash flows to the liabilities to loan note holders. The non-executive director is assuming a steady stream of lease income over the next 10 years, with the development probably being close to being fully occupied over that period.

The securitisation means that Moonstar Co is no longer concerned with the risk that the level of earnings from the properties will be insufficient to pay the finance costs. Risks have effectively been transferred to the loan note holders.

Risks

Not all of the tranches may appeal to investors. The risk-return relationship on the subordinated certificates does not look very appealing, with the return quite likely to be below what is received on the C-rated loan notes. Even the C-rated loan note holders may question the relationship between the risk and return if there is continued uncertainty in the property sector.

If Moonstar Co seeks funding from other sources for other developments, transferring out a lower risk income stream means that the residual risks associated with the rest of Moonstar Co’s portfolio will be higher. This may affect the availability and terms of other borrowing.

It appears that the size of the securitisation should be large enough for the costs to be bearable. However Moonstar Co may face unforeseen costs, possibly unexpected management or legal expenses.

(c) (i) Sukuk finance could be appropriate for the securitisation of the leasing portfolio. An asset-backed Sukuk would be the same kind of arrangement as the securitisation, where assets are transferred to a special purpose vehicle and the returns and repayments are directly financed by the income from the assets. The Sukuk holders would bear the risks and returns of the relationship.

The other type of Sukuk would be more like a sale and leaseback of the development. Here the Sukuk holders would be guaranteed a rental, so it would seem less appropriate for Moonstar Co if there is significant uncertainty about the returns from the development.

The main issue with the asset-backed Sukuk finance is whether it would be as appealing as certainly the A-tranche of the securitisation arrangement which the non-executive director has proposed. The safer income that the securitisation offers A-tranche investors may be more appealing to investors than a marginally better return from the Sukuk. There will also be costs involved in establishing and gaining approval for the Sukuk, although these costs may be less than for the securitisation arrangement described above.

(ii) A Mudaraba contract would involve the bank providing capital for Moonstar Co to invest in the development. Moonstar Co would manage the investment which the capital funded. Profits from the investment would be shared with the bank, but losses would be solely borne by the bank. A Mudaraba contract is essentially an equity partnership, so Moonstar Co might not face the threat to its credit rating which it would if it obtained ordinary loan finance for the development. A Mudaraba contract would also represent a diversification of sources of finance. It would not require the commitment to pay interest that loan finance would involve.

Moonstar Co would maintain control over the running of the project. A Mudaraba contract would offer a method of obtaining equity funding without the dilution of control which an issue of shares to external shareholders would bring. This is likely to make it appealing to Moonstar Co’s directors, given their desire to maintain a dominant influence over the business.

The bank would be concerned about the uncertainties regarding the rental income from the development. Although the lack of involvement by the bank might appeal to Moonstar Co's directors, the bank might not find it so attractive. The bank might be concerned about information asymmetry – that Moonstar Co’s management might be reluctant to supply the bank with the information it needs to judge how well its investment is performing.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-10

- 2020-01-10

- 2020-05-21

- 2020-04-07

- 2020-05-13

- 2020-04-18

- 2020-01-10

- 2019-07-20

- 2020-04-21

- 2020-05-08

- 2020-02-21

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-09

- 2020-02-27

- 2019-01-04

- 2020-01-09

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-04-11

- 2020-05-02

- 2020-05-16

- 2019-03-27

- 2020-04-22

- 2021-07-23

- 2020-01-09