ACCA考试一定要过英语四六级吗?

发布时间:2021-03-11

ACCA考试一定要过英语四六级吗?

最佳答案

没有要求四六级,由于ACCA专业资格考试全世界统一标准,教材、试卷、答题全用英语,所以建议想报名的学员先看看教材,再在ACCA网站上看一看历届试题,然后决定是否报考。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

2 Your firm was appointed as auditor to Indigo Co, an iron and steel corporation, in September 2005. You are the

manager in charge of the audit of the financial statements of Indigo, for the year ending 31 December 2005.

Indigo owns office buildings, a workshop and a substantial stockyard on land that was leased in 1995 for 25 years.

Day-to-day operations are managed by the chief accountant, purchasing manager and workshop supervisor who

report to the managing director.

All iron, steel and other metals are purchased for cash at ‘scrap’ prices determined by the purchasing manager. Scrap

metal is mostly high volume. A weighbridge at the entrance to the stockyard weighs trucks and vans before and after

the scrap metals that they carry are unloaded into the stockyard.

Two furnaces in the workshop melt down the salvageable scrap metal into blocks the size of small bricks that are then

stored in the workshop. These are sold on both credit and cash terms. The furnaces are now 10 years old and have

an estimated useful life of a further 15 years. However, the furnace linings are replaced every four years. An annual

provision is made for 25% of the estimated cost of the next relining. A by-product of the operation of the furnaces is

the production of ‘clinker’. Most of this is sold, for cash, for road surfacing but some is illegally dumped.

Indigo’s operations are subsidised by the local authority as their existence encourages recycling and means that there

is less dumping of metal items. Indigo receives a subsidy calculated at 15% of the market value of metals purchased,

as declared in a quarterly return. The return for the quarter to 31 December 2005 is due to be submitted on

21 January 2006.

Indigo maintains manual inventory records by metal and estimated quality. Indigo counted inventory at 30 November

2005 with the intention of ‘rolling-forward’ the purchasing manager’s valuation as at that date to the year-end

quantities per the manual records. However, you were not aware of this until you visited Indigo yesterday to plan

your year-end procedures.

During yesterday’s tour of Indigo’s premises you saw that:

(i) sheets of aluminium were strewn across fields adjacent to the stockyard after a storm blew them away;

(ii) much of the vast quantity of iron piled up in the stockyard is rusty;

(iii) piles of copper and brass, that can be distinguished with a simple acid test, have been mixed up.

The count sheets show that metal quantities have increased, on average, by a third since last year; the quantity of

aluminium, however, is shown to be three times more. There is no suitably qualified metallurgical expert to value

inventory in the region in which Indigo operates.

The chief accountant disappeared on 1 December, taking the cash book and cash from three days’ sales with him.

The cash book was last posted to the general ledger as at 31 October 2005. The managing director has made an

allegation of fraud against the chief accountant to the police.

The auditor’s report on the financial statements for the year ended 31 December 2004 was unmodified.

Required:

(a) Describe the principal audit procedures to be carried out on the opening balances of the financial statements

of Indigo Co for the year ending 31 December 2005. (6 marks)

2 INDIGO CO

(a) Opening balances – principal audit procedures

Tutorial note: ‘Opening balances’ means those account balances which exist at the beginning of the period. The question

clearly states that the prior year auditor’s report was unmodified therefore any digression into the prior period opinion being

other than unmodified or the prior period not having been audited will not earn marks.

■ Review of the application of appropriate accounting policies in the financial statements for the year ended 31 December

2004 to ensure consistent with those applied in 2005.

■ Where permitted (e.g. if there is a reciprocal arrangement with the predecessor auditor to share audit working papers

on a change of appointment), a review of the prior period audit working papers.

Tutorial note: There is no legal, ethical or other professional duty that requires a predecessor auditor to make available

its working papers.

■ Current period audit procedures that provide evidence concerning the existence, measurement and completeness of

rights and obligations. For example:

? after-date receipts (in January 2005 and later) confirming the recoverable amount of trade receivables at

31 December 2004;

? similarly, after-date payments confirming the completeness of trade and other payables (for services);

? after-date sales of inventory held at 31 December 2004;

? review of January 2005 bank reconciliation (confirming clearance of reconciling items at 31 December 2004).

■ Analytical procedures on ratios calculated month-on-month from 31 December 2004 to date and further investigation

of any distortions identified at the beginning of the current reporting period. For example:

? inventory turnover (by category of metal);

? average collection payment;

? average payment period;

? gross profit percentage (by metal).

■ Examination of historic accounting records for non-current assets and liabilities (if necessary). For example:

? agreeing balances on asset registers to the client’s trial balance as at 31 December 2004;

? agreeing statements of balances on loan accounts to the financial statements as at 31 December 2004.

■ If the above procedures do not provide sufficient evidence, additional substantive procedures should be performed. For

example, if additional evidence is required concerning inventory at 31 December 2004, cut-off tests may be

reperformed.

(b) Discuss the key issues which will need to be addressed in determining the basic components of an

internationally agreed conceptual framework. (10 marks)

Appropriateness and quality of discussion. (2 marks)

(b) There are several issues which have to be addressed if an international conceptual framework is to be successfully developed.

These are:

(i) Objectives

Agreement will be required as to whether financial statements are to be produced for shareholders or a wide range of

users and whether decision usefulness is the key criteria or stewardship. Additionally there is the question of whether

the objective is to provide information in making credit and investment decisions.

(ii) Qualitative Characteristics

The qualities to be sought in making decisions about financial reporting need to be determined. The decision usefulness

of financial reports is determined by these characteristics. There are issues concerning the trade-offs between relevance

and reliability. An example of this concerns the use of fair values and historical costs. It has been argued that historical

costs are more reliable although not as relevant as fair values. Additionally there is a conflict between neutrality and the

traditions of prudence or conservatism. These characteristics are constrained by materiality and benefits that justify

costs.

(iii) Definitions of the elements of financial statements

The principles behind the definition of the elements need agreement. There are issues concerning whether ‘control’

should be included in the definition of an asset or become part of the recognition criteria. Also the definition of ‘control’

is an issue particularly with financial instruments. For example, does the holder of a call option ‘control’ the underlying

asset? Some of the IASB’s standards contravene its own conceptual framework. IFRS3 requires the capitalisation of

goodwill as an asset despite the fact that it can be argued that goodwill does not meet the definition of an asset in the

Framework. IAS12 requires the recognition of deferred tax liabilities that do not meet the liability definition. Similarly

equity and liabilities need to be capable of being clearly distinguished. Certain financial instruments could either be

liabilities or equity. For example obligations settled in shares.

(iv) Recognition and De-recognition

The principles of recognition and de-recognition of assets and liabilities need reviewing. Most frameworks have

recognition criteria, but there are issues over the timing of recognition. For example, should an asset be recognised when

a value can be placed on it or when a cost has been incurred? If an asset or liability does not meet recognition criteria

when acquired or incurred, what subsequent event causes the asset or liability to be recognised? Most frameworks do

not discuss de-recognition. (The IASB’s Framework does not discuss the issue.) It can be argued that an item should be

de-recognised when it does not meet the recognition criteria, but financial instruments standards (IAS39) require other

factors to occur before financial assets can be de-recognised. Different attributes should be considered such as legal

ownership, control, risks or rewards.

(v) Measurement

More detailed discussion of the use of measurement concepts, such as historical cost, fair value, current cost, etc are

required and also more guidance on measurement techniques. Measurement concepts should address initial

measurement and subsequent measurement in the form. of revaluations, impairment and depreciation which in turn

gives rise to issues about classification of gains or losses in income or in equity.

(vi) Reporting entity

Issues have arisen over what sorts of entities should issue financial statements, and which entities should be included

in consolidated financial statements. A question arises as to whether the legal entity or the economic unit should be the

reporting unit. Complex business arrangements raise issues over what entities should be consolidated and the basis

upon which entities are consolidated. For example, should the basis of consolidation be ‘control’ and what does ‘control’

mean?

(vii) Presentation and disclosure

Financial reporting should provide information that enables users to assess the amounts, timing and uncertainty of the

entity’s future cash flows, its assets, liabilities and equity. It should provide management explanations and the limitations

of the information in the reports. Discussions as to the boundaries of presentation and disclosure are required.

(b) Explain how the use of SWOT analysis may be of assistance to the management of Diverse Holdings Plc.

(3 marks)

(b) The use of SWOT analysis will focus management attention on current strengths and weaknesses of each subsidiary company

which will be of assistance in the formulating of the business strategy of Diverse Holdings Plc. It will also enable management

to monitor trends and developments in the constantly changing environments of their subsidiaries. Each trend or development

may be classified as an opportunity or a threat that will provide a stimulus for an appropriate management response.

Management can make an assessment of the feasibility of required actions in order that the company may capitalise upon

opportunities whilst considering how best to negate or minimise the effect of any threats.

A SWOT analysis should assist the management of Diverse Holdings Plc as they must identify their strengths, weaknesses,

opportunities and threats. These may be classified as follows:

Strengths which appear to include both OFL and HTL.

Weaknesses which must include PSL and its limited outlets, which generate little growth and could collapse overnight. KAL

is also a weakness due to its declining profitability.

Opportunities where OFT, HTL and OPL are operating in growth markets.

Threats from which KAL is suffering.

If these four categories are identified and analysed then the group should be strengthened.

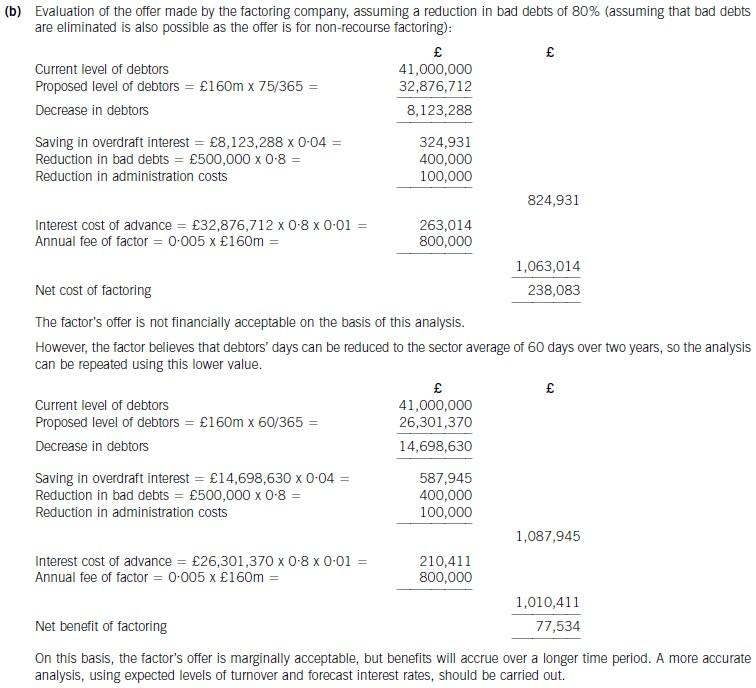

(b) Determine whether the factoring company’s offer can be recommended on financial grounds. Assume a

working year of 365 days and base your analysis on financial information for 2006. (8 marks)

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2021-04-23

- 2021-03-12

- 2021-02-15

- 2021-03-10

- 2021-04-23

- 2021-03-10

- 2021-04-16

- 2021-03-11

- 2021-03-11

- 2021-03-12

- 2021-06-06

- 2021-06-29

- 2021-05-07

- 2021-03-12

- 2021-03-12

- 2021-04-02

- 2021-03-12

- 2021-03-12

- 2021-02-23

- 2021-12-30

- 2021-04-21

- 2021-03-11

- 2021-06-05

- 2021-11-17

- 2021-03-10

- 2021-03-11

- 2021-04-24

- 2021-01-01

- 2021-03-12

- 2021-11-06