ACCA考试继续教育有哪些途径?

发布时间:2021-04-09

众所周知取得ACCA会员资格的第二年,ACCA会正式要求ACCA会员遵守CPD(继续教育)的相关政策,那么,ACCA会员能够通过哪些途径完成ACCA“继续教育”呢?接下来就和51题库考试学习网一起去了解下吧!

1.单位学时途径:

需要每年完成40个与相关的学时(一个学时即为一个小时)。其中21个学时的verifiable unit需要出示的相关证明材料(CPD evidence),其余的19个non-verifiable units学时则不需要出示任何证明。

2.单位学时兼职或半退休途径:

若会员全年工作时长低于770小时,则需要通过此途径,以工作时长+单位学时的组合完成CPD,只要有合理解释,该途径所需的单位学时通常没有限定。

3.ACCA认可雇主途径:

会员所在企业如果是ACCA CPD认可雇主,则只需保留就职于该公司的在职证明以及在每年年底提交当年的Annual CPD Declaration时,在PART 1的OPTION A部分勾选“ACCA Approved Employer Route”即可。

4.其它“国际会计师联合会”成员途径:

会员如果同时隶属于其他国际财会专业团体,则ACCA官方承认会员在其他组织的继续教育有效性。

5.CPD豁免:

若会员处于离职状态,并且超过一个月,则可以申请豁免CPD。

报名注册ACCA学员,具备以下条件之一即可:

1、教育部认可的高等院校在校生(本科在校),顺利完成大一的课程考试,即可报名成为ACCA的正式学员;

2、凡具有教育部承认的大专以上学历,即可报名成为ACCA的正式学员;

3、未符合1、2项报名资格的申请者,年满16周岁的可以先申请参加FIA(Foundations in Accountancy)基础财务资格考试。在完成FAB(基础商业会计)、FMA(基础管理会计)、FFA(基础财务会计)3门课程后,可以豁免ACCAF1-F3三门课程的考试,直接进入ACCA技能课程的考试

以上就是51题库考试学习网给大家带来的关于ACCA考试继续教育的相关分享,是不是对于ACCA继续教育有了基本的认识了,还没有完成继续教育的考生赶紧行动起来吧!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) Briefly discuss how stakeholder groups (other than management and employees) may be rewarded for ‘good’

performance. (4 marks)

(b) Good performance should result in improved profitability and therefore other stakeholder groups may be rewarded for ‘good

performance’ as follows:

– Shareholders may receive increased returns on equity in the form. of increased dividends and /or capital growth.

– Customers may benefit from improved quality of products and services, and possibly lower prices.

– Suppliers may benefit from increased volumes of purchases.

– Government will benefit from increased amounts of taxation.

(b) Provide an example that illustrates a structured application of the terms contained in the above statement in

respect of a profit-seeking organisation OR a not-for-profit organisation of your own choice. (6 marks)

(b) An illustration of the features detailed above, framed in the context of a University as an organisation in the not-for-profit sector

might be as follows:

The Overall objective might well be stated in the mission statement of a University. An example of such a mission statement

might be as follows:

‘To provide a quality educational environment in a range of undergraduate and post-graduate disciplines and a quality

educational focus for students and the business community.’

More specifically, objectives may be seen as the achievement of ‘value for money’ thereby ensuring effectiveness in areas such

as:

– The provision of high added value to students;

– The establishment of a reputation for recognised expertise in specific areas of research work within the wider community;

and

– The provision of a high quality service to industry and commerce.

Strategies may focus on aspects such as:

– The recruitment and retention of high quality academic staff;

– The development of IT equipment and skills within the institution;

– The mentoring of students in order to ensure high added value and low drop-out rates in intermediate years of study;

and

– The close liaison with employers as to qualities in graduate/post-graduate employees that they will value highly.

The determinants used to measure the results of strategies might include:

– Competitiveness – cost per graduate compared to other institutions; growth in student numbers; number of staff holding

a PhD qualification;

– Financial performance – average cost per graduate; income generation from consultancy work;

– Quality – range of awards (percentages of 1st class degrees); employer responses; measures of quality of delivery of

education, advice to students, etc;

– Flexibility – variable entry and exit points to courses; modular structure; the variety of full-time, part-time and distance

learning modes;

– Resource Utilisation – staff:student ratios; quotas met by each course; accommodation filled;

– Innovation – latest IT provision in linking lecture theatres to information databases; increased provision of flexilearning/

mixed mode course provision.

The application of business change techniques might include the following:

BPR with a focus on IT developments, flexible-learning or mixed mode course provision.

JIT with a focus on moves towards student-centred uptake of educational opportunities e.g. via intranet availability of lecture

and tutorial material linked to more flexible access to staff rather than a ‘push’ system of pre-structured times of

lectures/tutorials.

TQM with a focus on moves to improve quality in all aspects of the learning environment including delivery of lectures, access

to staff and pastoral care issues.

ABM with a focus on activities on a per student basis (both planned and actual) with a view to eliminating activities that do

not add value e.g. cost per lecture per student.

(ii) the factors that should be considered in the design of a reward scheme for BGL; (7 marks)

(ii) The factors that should be considered in the design of a reward scheme for BGL.

– Whether performance targets should be set with regard to results or effort. It is more difficult to set targets for

administrative and support staff since in many instances the results of their efforts are not easily quantifiable. For

example, sales administrators will improve levels of customer satisfaction but quantifying this is extremely difficult.

– Whether rewards should be monetary or non-monetary. Money means different things to different people. In many

instances people will prefer increased job security which results from improved organisational performance and

adopt a longer term-perspective. Thus the attractiveness of employee share option schemes will appeal to such

individuals. Well designed schemes will correlate the prosperity of the organisation with that of the individuals it

employs.

– Whether the reward promise should be implicit or explicit. Explicit reward promises are easy to understand but in

many respects management will have their hands tied. Implicit reward promises such as the ‘promise’ of promotion

for good performance is also problematic since not all organisations are large enough to offer a structured career

progression. Thus in situations where not everyone can be promoted there needs to be a range of alternative reward

systems in place to acknowledge good performance and encourage commitment from the workforce.

– The size and time span of the reward. This can be difficult to determine especially in businesses such as BGL

which are subject to seasonal variations. i.e. summerhouses will invariably be purchased prior to the summer

season! Hence activity levels may vary and there remains the potential problem of assessing performance when

an organisation operates with surplus capacity.

– Whether the reward should be individual or group based. This is potentially problematic for BGL since the assembly

operatives comprise some individuals who are responsible for their own output and others who work in groups.

Similarly with regard to the sales force then the setting of individual performance targets is problematic since sales

territories will vary in terms of geographical spread and customer concentration.

– Whether the reward scheme should involve equity participation? Such schemes invariably appeal to directors and

senior managers but should arguably be open to all individuals if ‘perceptions of inequity’ are to be avoided.

– Tax considerations need to be taken into account when designing a reward scheme.

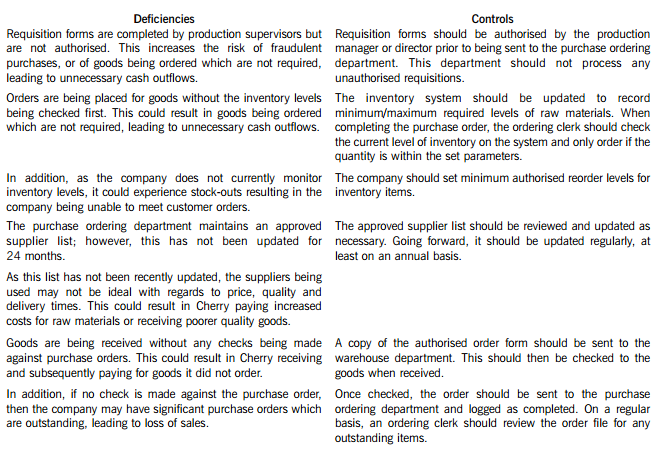

Cherry Blossom Co (Cherry) manufactures custom made furniture and its year end is 30 April. The company purchases its raw materials from a wide range of suppliers. Below is a description of Cherry’s purchasing system.

When production supervisors require raw materials, they complete a requisition form. and this is submitted to the purchase ordering department. Requisition forms do not require authorisation and no reference is made to the current inventory levels of the materials being requested. Staff in the purchase ordering department use the requisitions to raise sequentially numbered purchase orders based on the approved suppliers list, which was last updated 24 months ago. The purchasing director authorises the orders prior to these being sent to the suppliers.

When the goods are received, the warehouse department verifies the quantity to the suppliers despatch note and checks that the quality of the goods received are satisfactory. They complete a sequentially numbered goods received note (GRN) and send a copy of the GRN to the finance department.

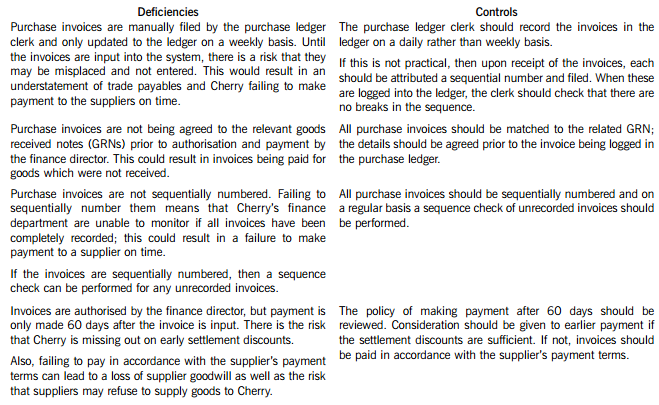

Purchase invoices are sent directly to the purchase ledger clerk, who stores them in a manual file until the end of each week. He then inputs them into the purchase ledger using batch controls and gives each invoice a unique number based on the supplier code. The invoices are reviewed and authorised for payment by the finance director, but the actual payment is only made 60 days after the invoice is input into the system.

Required:

In respect of the purchasing system of Cherry Blossom Co:

(i) Identify and explain FIVE deficiencies; and

(ii) Recommend a control to address each of these deficiencies.

Note: The total marks will be split equally between each part.

Cherry Blossom Co’s (Cherry) purchasing system deficiencies and controls

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-02-29

- 2020-01-08

- 2020-01-08

- 2020-01-08

- 2019-07-20

- 2019-07-20

- 2019-07-20

- 2020-01-08

- 2020-01-03

- 2019-07-20

- 2020-01-08

- 2019-07-20

- 2020-01-08

- 2020-01-08

- 2019-07-20

- 2020-02-29

- 2020-01-03

- 2020-01-08

- 2020-01-08

- 2021-05-23

- 2019-07-20

- 2019-07-20

- 2020-02-29

- 2020-01-08

- 2020-01-08

- 2019-07-20

- 2019-07-20

- 2020-01-08

- 2020-01-02

- 2020-01-08