注意!2020年9月ACCA考试早报名时间来了

发布时间:2020-04-17

相信大家都或多或少的听说过ACCA。那么什么是ACCA呢?由51题库考试学习网为您进行解答。ACCA是目前财经领域认可度最高的资格证书,也是世界上拥有学员和会员最多的,为此还被我国称之为“国际注册会计师”。你知道2020年9月ACCA考试早报名时间来了吗?,那不知道的朋友们请一定要继续看下去!

2020年9月ACCA考季将在9月7日-9月11日间进行,计划参考本次考季考试的考生们,请提前完成考试科目的在线报名及缴费。

一、9月ACCA报名时间

提前报名时段:5月5日-5月11日

常规报考时段:5月12日-7月27日

截止报名时段:7月28日-8月3日

知道2020年9月ACCA考试早报名时间了,那关于ACCA的其他内容你知道吗?要不接着看下去吧!

缴费情况:

在ACCA官网缴费是支持使用银联卡和支付宝的。但ACCA总部推荐学员使用双币信用卡在线考试报名。这样将可以及时确认报名成功并且可以享受提前考试报名时段的优惠价格。 但如果在我们缴纳ACCA报名费时,网页显示报名成功,但未收到银行扣款通知怎么办?如果其他步骤都没有出错,并且有显示报考成功的话,有可能是由于因为报名时ACCA使用的信用卡预授权消费,信用卡发卡行会先把你这笔缴费款冻结住,一般银行过1-2个工作日会跟ACCA官方对账,确定这笔款项真的没问题时,才会把费用真正扣除。所以,当出现上述情况时,先检查自己的各项信息,没错的话,可以过两天再查询具体情况吧!

就业前景:

国际知名机构建立了密切的合作关系,包括跨国企业、各国地方企业、其他会计师组织、教育机构、以及联合国、世界银行等世界性组织。全球共有7000多家ACCA认证雇主,其中在中国有超过700家ACCA认证雇主,这些认证雇主企业将优先录用及提升ACCA会员及毕业生。

ACCA未来的就业方向和行业主要集中在以下公司:

国际国内大型银行及投资银行:花旗银行、汇丰银行、渣打银行、中国工商银行、中国银行等。

保险及金融投资机构:中国国际金融公司、美国高盛、美国友邦保险、鼎辉投资等。

国际知名企业:可口可乐(中国)有限公司、微软(中国)有限公司、西门子中国有限公司等。

中国大型国有及民营企业:中国移动通信集团、中国石油天然气集团、阿里巴巴、联想集团等。

国际知名咨询企业及会计师事务所:麦肯锡、埃森哲、四大国际会计师事务所。

以上就是由51题库考试学习网为您带来的有关AACA的相关信息了,想要获取更多信息的同学,请持续关注51题库考试学习网。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

One of your audit clients is Tye Co a company providing petrol, aviation fuel and similar oil based products to the government of the country it is based in. Although the company is not listed on any stock exchange, it does follow best practice regarding corporate governance regulations. The audit work for this year is complete, apart from the matter referred to below.

As part of Tye Co’s service contract with the government, it is required to hold an emergency inventory reserve of 6,000 barrels of aviation fuel. The inventory is to be used if the supply of aviation fuel is interrupted due to unforeseen events such as natural disaster or terrorist activity.

This fuel has in the past been valued at its cost price of $15 a barrel. The current value of aviation fuel is $120 a barrel. Although the audit work is complete, as noted above, the directors of Tye Co have now decided to show the ‘real’ value of this closing inventory in the financial statements by valuing closing inventory of fuel at market value, which does not comply with relevant accounting standards. The draft financial statements of Tye Co currently show a profit of approximately $500,000 with net assets of $170 million.

Required:

(a) List the audit procedures and actions that you should now take in respect of the above matter. (6 marks)

(b) For the purposes of this section assume from part (a) that the directors have agreed to value inventory at

$15/barrel.

Having investigated the matter in part (a) above, the directors present you with an amended set of financial

statements showing the emergency reserve stated not at 6,000 barrels, but reported as 60,000 barrels. The final financial statements now show a profit following the inclusion of another 54,000 barrels of oil in inventory. When queried about the change from 6,000 to 60,000 barrels of inventory, the finance director stated that this change was made to meet expected amendments to emergency reserve requirements to be published in about six months time. The inventory will be purchased this year, and no liability will be shown in the financial statements for this future purchase. The finance director also pointed out that part of Tye Co’s contract with the government requires Tye Co to disclose an annual profit and that a review of bank loans is due in three months. Finally the finance director stated that if your audit firm qualifies the financial statements in respect of the increase in inventory, they will not be recommended for re-appointment at the annual general meeting. The finance director refuses to amend the financial statements to remove this ‘fictitious’ inventory.

Required:

(i) State the external auditor’s responsibilities regarding the detection of fraud; (4 marks)

(ii) Discuss to which groups the auditors of Tye Co could report the ‘fictitious’ aviation fuel inventory;

(6 marks)

(iii) Discuss the safeguards that the auditors of Tye Co can use in an attempt to overcome the intimidation

threat from the directors of Tye Co. (4 marks)

(a)Valuationofaviationinventory–ReviewGAAPtoensurethattherearenoexceptionsforaviationfuelorinventoryheldforemergencypurposeswhichwouldsuggestamarketvaluationshouldbeused.–Calculatethedifferenceinvaluation.Theerrorininventoryvaluationis$105*6,000barrelsor$630k,whichisamaterialamountcomparedtoprofit.–Reviewprioryearworkingpaperstodeterminewhetherasimilarsituationoccurredlastyearandascertaintheoutcomeatthatstage.–Discussthematterwiththedirectorstoobtainreasonswhytheybelievethatmarketvalueshouldbeusedfortheinventorythisyear.–Warnthedirectorsthatinyouropinion,aviationfuelshouldbevaluedatthelowerofcostornetrealisablevalue(thatis$15/barrel)andthatusingmarketvaluewillresultinamodificationtotheauditreport.–Ifthedirectorsnowamendthefinancialstatementstoshowinventoryvaluedatcost,thenconsidermentioningtheissueintheweaknessletteranddonotmodifytheauditreportinrespectofthismatter.–Ifthedirectorswillnotamendthefinancialstatements,quantifytheeffectofthedisagreementinthevaluationmethod–thesumof$630,000ismaterialtothefinancialstatementsasTyeCo’sincomestatementfigureisdecreasedfromasmalllosstoalossof$130,000althoughnetassetsdecreasebyonlyabout0·3%.–ObtainamanagementrepresentationletterfromthedirectorsofTyeCoconfirmingthatmarketvalueistobeusedfortheemergencyinventoryofaviationfuel.–Ifthedirectorswillnotamendthefinancialstatements,drafttherelevantsectionsoftheauditreport,showingaqualificationonthegroundsofdisagreementwiththeaccountingpolicyforvaluationofinventory.(b)(i)ExternalauditorresponsibilitiesregardingdetectionoffraudOverallresponsibilityofauditorTheexternalauditorisprimarilyresponsiblefortheauditopiniononthefinancialstatementsfollowingtheinternationalauditingstandards(ISAs).ISA240(Redrafted)TheAuditor’sResponsibilitiesRelatingtoFraudinanAuditofFinancialStatementsisrelevanttoauditworkregardingfraud.Themainfocusofauditworkisthereforetoensurethatthefinancialstatementsshowatrueandfairview.Thedetectionoffraudisthereforenotthemainfocusoftheexternalauditor’swork.Anauditorisresponsibleforobtainingreasonableassurancethatthefinancialstatementsasawholearefreefrommaterialmisstatement,whethercausedbyfraudorerror.Theauditorisresponsibleformaintaininganattitudeofprofessionalscepticismthroughouttheaudit,consideringthepotentialformanagementoverrideofcontrolsandrecognisingthefactthatauditproceduresthatareeffectivefordetectingerrormaynotbeeffectivefordetectingfraud.MaterialityISA240statesthattheauditorshouldreduceauditrisktoanacceptablylowlevel.Therefore,inreachingtheauditopinionandperformingauditwork,theexternalauditortakesintoaccounttheconceptofmateriality.Inotherwords,theexternalauditorisnotresponsibleforcheckingallthetransactions.Auditproceduresareplannedtohaveareasonablelikelihoodofidentifyingmaterialfraud.DiscussionamongtheauditteamAdiscussionisrequiredamongtheengagementteamplacingparticularemphasisonhowandwheretheentity’sfinancialstatementsmaybesusceptibletomaterialmisstatementduetofaud,includinghowfraudmightoccur.IdentificationoffraudInsituationswheretheexternalauditordoesdetectfraud,thentheauditorwillneedtoconsidertheimplicationsfortheentireaudit.Inotherwords,theexternalauditorhasaresponsibilitytoextendtestingintootherareasbecausetheriskofprovidinganincorrectauditopinionwillhaveincreased.(ii)GroupstoreportfraudtoReporttoauditcommitteeDisclosethesituationtotheauditcommitteeastheyarechargedwithmaintainingahighstandardofgovernanceinthecompany.Thecommitteeshouldbeabletodiscussthesituationwiththedirectorsandrecommendthattheytakeappropriateactione.g.amendthefinancialstatements.ReporttogovernmentAsTyeCoisactingunderagovernmentcontract,andtheover-statementofinventorywillmeanTyeCobreachesthatcontract(thereportedprofitbecomingaloss),thentheauditormayhavetoreportthesituationdirectlytothegovernment.TheauditorofTyeConeedstoreviewthecontracttoconfirmthereportingrequiredunderthatcontract.ReporttomembersIfthefinancialstatementsdonotshowatrueandfairviewthentheauditorneedstoreportthisfacttothemembersofTyeCo.Theauditreportwillbequalifiedwithanexceptfororadverseopinion(dependingonmateriality)andinformationconcerningthereasonforthedisagreementgiven.Inthiscasetheauditorislikelytostatefactuallytheproblemofinventoryquantitiesbeingincorrect,ratherthanstatingorimplyingthatthedirectorsareinvolvedinfraud.ReporttoprofessionalbodyIftheauditorisuncertainastothecorrectcourseofaction,advicemaybeobtainedfromtheauditor’sprofessionalbody.Dependingontheadvicereceived,theauditormaysimplyreporttothemembersintheauditreport,althoughresignationandtheconveningofageneralmeetingisanotherreportingoption.(iii)Intimidationthreat–safeguardsInresponsetotheimpliedthreatofdismissaliftheauditreportismodifiedregardingthepotentialfraud/error,thefollowingsafeguardsareavailabletotheauditor.DiscusswithauditcommitteeThesituationcanbediscussedwiththeauditcommittee.Astheauditcommitteeshouldcomprisenon-executivedirectors,theywillbeabletodiscussthesituationwiththefinancedirectorandpointoutclearlytheauditor’sopinion.Theycanalsoremindthedirectorsasawholethattheappointmentoftheauditorrestswiththemembersontherecommendationoftheauditcommittee.Iftherecommendationoftheauditcommitteeisrejectedbytheboard,goodcorporategovernancerequiresdisclosureofthereasonforrejection.ObtainsecondpartnerreviewTheengagementpartnercanaskasecondpartnertoreviewtheworkingpapersandotherevidencerelatingtotheissueofpossiblefraud.Whilethisactiondoesnotresolvetheissue,itdoesprovideadditionalassurancethatthefindingsandactionsoftheengagementpartnerarevalid.ResignationIfthematterisserious,thentheauditorcanconsiderresignationratherthannotbeingre-appointed.Resignationhastheadditionalsafeguardthattheauditorcannormallyrequirethedirectorstoconveneageneralmeetingtoconsiderthecircumstancesoftheresignation.

(b) (i) Discusses the principles involved in accounting for claims made under the above warranty provision.

(6 marks)

(ii) Shows the accounting treatment for the above warranty provision under IAS37 ‘Provisions, Contingent

Liabilities and Contingent Assets’ for the year ended 31 October 2007. (3 marks)

Appropriateness of the format and presentation of the report and communication of advice. (2 marks)

(b) Provisions – IAS37

An entity must recognise a provision under IAS37 if, and only if:

(a) a present obligation (legal or constructive) has arisen as a result of a past event (the obligating event)

(b) it is probable (‘more likely than not’), that an outflow of resources embodying economic benefits will be required to settle

the obligation

(c) the amount can be estimated reliably

An obligating event is an event that creates a legal or constructive obligation and, therefore, results in an enterprise having

no realistic alternative but to settle the obligation. A constructive obligation arises if past practice creates a valid expectation

on the part of a third party. If it is more likely than not that no present obligation exists, the enterprise should disclose a

contingent liability, unless the possibility of an outflow of resources is remote.

The amount recognised as a provision should be the best estimate of the expenditure required to settle the present obligation

at the balance sheet date, that is, the amount that an enterprise would rationally pay to settle the obligation at the balance

sheet date or to transfer it to a third party. This means provisions for large populations of events such as warranties, are

measured at a probability weighted expected value. In reaching its best estimate, the entity should take into account the risks

and uncertainties that surround the underlying events.

Expected cash outflows should be discounted to their present values, where the effect of the time value of money is material

using a risk adjusted rate (it should not reflect risks for which future cash flows have been adjusted). If some or all of the

expenditure required to settle a provision is expected to be reimbursed by another party, the reimbursement should be

recognised as a separate asset when, and only when, it is virtually certain that reimbursement will be received if the entity

settles the obligation. The amount recognised should not exceed the amount of the provision. In measuring a provision future

events should be considered. The provision for the warranty claim will be determined by using the expected value method.

The past event which causes the obligation is the initial sale of the product with the warranty given at that time. It would be

appropriate for the company to make a provision for the Year 1 warranty of $280,000 and Year 2 warranty of $350,000,

which represents the best estimate of the obligation (see Appendix 2). Only if the insurance company have validated the

counter claim will Macaljoy be able to recognise the asset and income. Recovery has to be virtually certain. If it is virtually

certain, then Macaljoy may be able to recognise the asset. Generally contingent assets are never recognised, but disclosed

where an inflow of economic benefits is probable.

The company could discount the provision if it was considered that the time value of money was material. The majority of

provisions will reverse in the short term (within two years) and, therefore, the effects of discounting are likely to be immaterial.

In this case, using the risk adjusted rate (IAS37), the provision would be reduced to $269,000 in Year 1 and $323,000 in

Year 2. The company will have to determine whether this is material.

Appendix 1

The accounting for the defined benefit plan is as follows:

(ii) the recent financial performance of Merton plc from a shareholder perspective. Clearly identify any

issues that you consider should be brought to the attention of the ordinary shareholders. (15 marks)

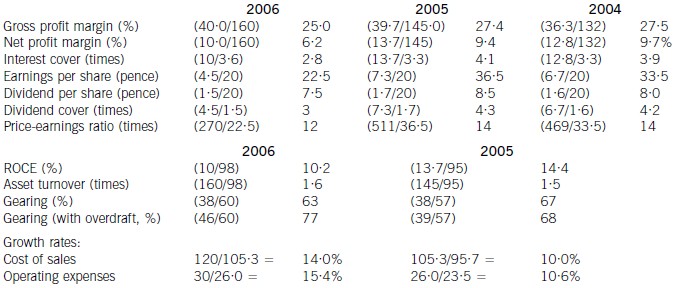

(ii) Discussion of financial performance

It is clear that 2006 has been a difficult year for Merton plc. There are very few areas of interest to shareholders where

anything positive can be found to say.

Profitability

Return on capital employed has declined from 14·4% in 2005, which compared favourably with the sector average of

12%, to 10·2% in 2006. Since asset turnover has improved from 1·5 to 1·6 in the same period, the cause of the decline

is falling profitability. Gross profit margin has fallen each year from 27·5% in 2004 to 25% in 2006, equal to the sector

average, despite an overall increase in turnover during the period of 10% per year. Merton plc has been unable to keep

cost of sales increases (14% in 2006 and 10% in 2005) below the increases in turnover. Net profit margin has declined

over the same period from 9·7% to 6·2%, compared to the sector average of 8%, because of substantial increases in

operating expenses (15·4% in 2006 and 10·6% in 2005). There is a pressing need here for Merton plc to bring cost

of sales and operating costs under control in order to improve profitability.

Gearing and financial risk

Gearing as measured by debt/equity has fallen from 67% (2005) to 63% (2006) because of an increase in

shareholders’ funds through retained profits. Over the same period the overdraft has increased from £1m to £8m and

cash balances have fallen from £16m to £1m. This is a net movement of £22m. If the overdraft is included, gearing

has increased to 77% rather than falling to 63%.

None of these gearing levels compare favourably with the average gearing for the sector of 50%. If we consider the large

increase in the overdraft, financial risk has clearly increased during the period. This is also evidenced by the decline in

interest cover from 4·1 (2005) to 2·8 (2006) as operating profit has fallen and interest paid has increased. In each year

interest cover has been below the sector average of eight and the current level of 2·8 is dangerously low.

Share price

As the return required by equity investors increases with increasing financial risk, continued increases in the overdraft

will exert downward pressure on the company’s share price and further reductions may be expected.

Investor ratios

Earnings per share, dividend per share and dividend cover have all declined from 2005 to 2006. The cut in the dividend

per share from 8·5 pence per share to 7·5 pence per share is especially worrying. Although in its announcement the

company claimed that dividend growth and share price growth was expected, it could have chosen to maintain the

dividend, if it felt that the current poor performance was only temporary. By cutting the dividend it could be signalling

that it expects the poor performance to continue. Shareholders have no guarantee as to the level of future dividends.

This view could be shared by the market, which might explain why the price-earnings ratio has fallen from 14 times to

12 times.

Financing strategy

Merton plc has experienced an increase in fixed assets over the last period of £10m and an increase in stocks and

debtors of £21m. These increases have been financed by a decline in cash (£15m), an increase in the overdraft (£7m)

and an increase in trade credit (£6m). The company is following an aggressive strategy of financing long-term

investment from short-term sources. This is very risky, since if the overdraft needed to be repaid, the company would

have great difficulty in raising the funds required.

A further financing issue relates to redemption of the existing debentures. The 10% debentures are due to be redeemed

in two years’ time and Merton plc will need to find £13m in order to do this. It does not appear that this sum can be

raised internally. While it is possible that refinancing with debt paying a lower rate of interest may be possible, the low

level of interest cover may cause concern to potential providers of debt finance, resulting in a higher rate of interest. The

Finance Director of Merton plc needs to consider the redemption problem now, as thought is currently being given to

raising a substantial amount of new equity finance. This financing choice may not be available again in the near future,

forcing the company to look to debt finance as a way of effecting redemption.

Overtrading

The evidence produced by the financial analysis above is that Merton plc is showing some symptoms of overtrading

(undercapitalisation). The board are suggesting a rights issue as a way of financing an expansion of business, but it is

possible that a rights issue will be needed to deal with the overtrading problem. This is a further financing issue requiring

consideration in addition to the redemption of debentures mentioned earlier.

Conclusion

Ordinary shareholders need to be aware of the following issues.

1. Profitability has fallen over the last year due to poor cost control

2. A substantial increase in the overdraft over the last year has caused gearing to increase

3. It is possible that the share price will continue to fall

4. The dividend cut may warn of continuing poor performance in the future

5. A total of £13m of debentures need redeeming in two year’s time

6. A large amount of new finance is needed for working capital and debenture redemption

Appendix: Analysis of key ratios and financial information

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-03-22

- 2020-01-30

- 2020-01-10

- 2020-05-08

- 2020-03-13

- 2020-04-10

- 2020-01-10

- 2020-01-09

- 2020-04-18

- 2020-05-17

- 2020-05-17

- 2020-01-10

- 2021-06-25

- 2020-01-09

- 2020-01-08

- 2020-01-08

- 2019-07-21

- 2020-01-09

- 2020-01-10

- 2020-01-10

- 2021-06-25

- 2020-01-09

- 2020-01-10

- 2020-04-07

- 2020-04-11

- 2020-03-27

- 2020-03-13

- 2020-02-29

- 2020-01-14

- 2020-03-27