我是北京林业大学毕业,报考了ACCA这个就业前...

发布时间:2021-06-04

我是北京林业大学毕业,报考了ACCA这个就业前景怎么样啊?

最佳答案

ACCA作为全球规模最大的专业会计师组织,被公认为“国际财会界的通行证”。如今财会业的现状是,财务会计已经达到饱和,因此拥有ACCA证书的管理会计型人才一直都十分受到世界500强企业和国际国内大型知名企业的青睐。在中国,共有超过400家的国际国内知名企业是ACCA的“认可雇主企业”,如BP石油、联合利华、可口可乐、空客公司、GE等,ACCA在这些企业就职都可以获得很好的个人职业发展。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(iii) How items not dealt with by an IFRS for SMEs should be treated. (5 marks)

(iii) The treatment of items not dealt with by an IFRS for SMEs

IFRSs for SMEs would not necessarily deal with all the recognition and measurement issues facing an entity but the key

issues should revolve around the nature of the recognition, measurement and disclosure of the transactions of SMEs. In

the case where the item is not dealt with by the standards there are three alternatives:

(a) the entity can look to the full IFRS to resolve the issue

(b) management’s judgement can be used with reference to the Framework and consistency with other IFRSs for SMEs

(c) existing practice could be used.

The first approach is more likely to result in greater consistency and comparability. However, this approach may also

increase the burden on SMEs as it can be argued that they are subject to two sets of standards.

An SME may wish to make a disclosure required by a full IFRS which is not required by the SME standard, or a

measurement principle is simplified or exempted in the SME standard, or the IFRS may give a choice between two

measurement options and the SME standard does not allow choice. Thus the issue arises as to whether SMEs should

be able to choose to comply with a full IFRS for some items and SME standards for other items, allowing an SME to

revert to IFRS on a principle by principle basis. The problem which will arise will be a lack of consistency and

comparability of SME financial statements.

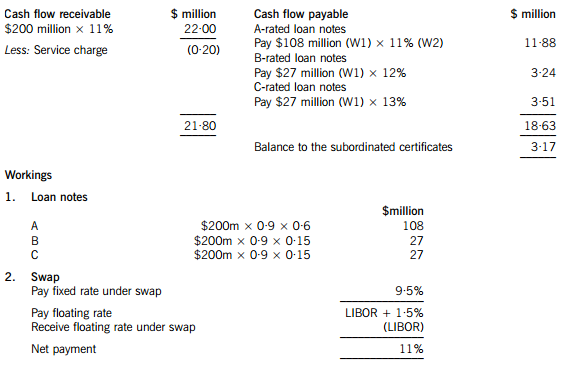

Moonstar Co is a property development company which is planning to undertake a $200 million commercial property development. Moonstar Co has had some difficulties over the last few years, with some developments not generating the expected returns and the company has at times struggled to pay its finance costs. As a result Moonstar Co’s credit rating has been lowered, affecting the terms it can obtain for bank finance. Although Moonstar Co is listed on its local stock exchange, 75% of the share capital is held by members of the family who founded the company. The family members who are shareholders do not wish to subscribe for a rights issue and are unwilling to dilute their control over the company by authorising a new issue of equity shares. Moonstar Co’s board is therefore considering other methods of financing the development, which the directors believe will generate higher returns than other recent investments, as the country where Moonstar Co is based appears to be emerging from recession.

Securitisation proposals

One of the non-executive directors of Moonstar Co has proposed that it should raise funds by means of a securitisation process, transferring the rights to the rental income from the commercial property development to a special purpose vehicle. Her proposals assume that the leases will generate an income of 11% per annum to Moonstar Co over a ten-year period. She proposes that Moonstar Co should use 90% of the value of the investment for a collateralised loan obligation which should be structured as follows:

– 60% of the collateral value to support a tranche of A-rated floating rate loan notes offering investors LIBOR plus 150 basis points

– 15% of the collateral value to support a tranche of B-rated fixed rate loan notes offering investors 12%

– 15% of the collateral value to support a tranche of C-rated fixed rate loan notes offering investors 13%

– 10% of the collateral value to support a tranche as subordinated certificates, with the return being the excess of receipts over payments from the securitisation process

The non-executive director believes that there will be sufficient demand for all tranches of the loan notes from investors. Investors will expect that the income stream from the development to be low risk, as they will expect the property market to improve with the recession coming to an end and enough potential lessees to be attracted by the new development.

The non-executive director predicts that there would be annual costs of $200,000 in administering the loan. She acknowledges that there would be interest rate risks associated with the proposal, and proposes a fixed for variable interest rate swap on the A-rated floating rate notes, exchanging LIBOR for 9·5%.

However the finance director believes that the prediction of the income from the development that the non-executive director has made is over-optimistic. He believes that it is most likely that the total value of the rental income will be 5% lower than the non-executive director has forecast. He believes that there is some risk that the returns could be so low as to jeopardise the income for the C-rated fixed rate loan note holders.

Islamic finance

Moonstar Co’s chief executive has wondered whether Sukuk finance would be a better way of funding the development than the securitisation.

Moonstar Co’s chairman has pointed out that a major bank in the country where Moonstar Co is located has begun to offer a range of Islamic financial products. The chairman has suggested that a Mudaraba contract would be the most appropriate method of providing the funds required for the investment.

Required:

(a) Calculate the amounts in $ which each of the tranches can expect to receive from the securitisation arrangement proposed by the non-executive director and discuss how the variability in rental income affects the returns from the securitisation. (11 marks)

(b) Discuss the benefits and risks for Moonstar Co associated with the securitisation arrangement that the non-executive director has proposed. (6 marks)

(c) (i) Discuss the suitability of Sukuk finance to fund the investment, including an assessment of its appeal to potential investors. (4 marks)

(ii) Discuss whether a Mudaraba contract would be an appropriate method of financing the investment and discuss why the bank may have concerns about providing finance by this method. (4 marks)

(a) An annual cash flow account compares the estimated cash flows receivable from the property against the liabilities within the securitisation process. The swap introduces leverage into the arrangement.

The holders of the certificates are expected to receive $3·17million on $18 million, giving them a return of 17·6%. If the cash flows are 5% lower than the non-executive director has predicted, annual revenue received will fall to $20·90 million, reducing the balance available for the subordinated certificates to $2·07 million, giving a return of 11·5% on the subordinated certificates, which is below the returns offered on the B and C-rated loan notes. The point at which the holders of the certificates will receive nothing and below which the holders of the C-rated loan notes will not receive their full income will be an annual income of $18·83 million (a return of 9·4%), which is 14·4% less than the income that the non-executive director has forecast.

(b) Benefits

The finance costs of the securitisation may be lower than the finance costs of ordinary loan capital. The cash flows from the commercial property development may be regarded as lower risk than Moonstar Co’s other revenue streams. This will impact upon the rates that Moonstar Co is able to offer borrowers.

The securitisation matches the assets of the future cash flows to the liabilities to loan note holders. The non-executive director is assuming a steady stream of lease income over the next 10 years, with the development probably being close to being fully occupied over that period.

The securitisation means that Moonstar Co is no longer concerned with the risk that the level of earnings from the properties will be insufficient to pay the finance costs. Risks have effectively been transferred to the loan note holders.

Risks

Not all of the tranches may appeal to investors. The risk-return relationship on the subordinated certificates does not look very appealing, with the return quite likely to be below what is received on the C-rated loan notes. Even the C-rated loan note holders may question the relationship between the risk and return if there is continued uncertainty in the property sector.

If Moonstar Co seeks funding from other sources for other developments, transferring out a lower risk income stream means that the residual risks associated with the rest of Moonstar Co’s portfolio will be higher. This may affect the availability and terms of other borrowing.

It appears that the size of the securitisation should be large enough for the costs to be bearable. However Moonstar Co may face unforeseen costs, possibly unexpected management or legal expenses.

(c) (i) Sukuk finance could be appropriate for the securitisation of the leasing portfolio. An asset-backed Sukuk would be the same kind of arrangement as the securitisation, where assets are transferred to a special purpose vehicle and the returns and repayments are directly financed by the income from the assets. The Sukuk holders would bear the risks and returns of the relationship.

The other type of Sukuk would be more like a sale and leaseback of the development. Here the Sukuk holders would be guaranteed a rental, so it would seem less appropriate for Moonstar Co if there is significant uncertainty about the returns from the development.

The main issue with the asset-backed Sukuk finance is whether it would be as appealing as certainly the A-tranche of the securitisation arrangement which the non-executive director has proposed. The safer income that the securitisation offers A-tranche investors may be more appealing to investors than a marginally better return from the Sukuk. There will also be costs involved in establishing and gaining approval for the Sukuk, although these costs may be less than for the securitisation arrangement described above.

(ii) A Mudaraba contract would involve the bank providing capital for Moonstar Co to invest in the development. Moonstar Co would manage the investment which the capital funded. Profits from the investment would be shared with the bank, but losses would be solely borne by the bank. A Mudaraba contract is essentially an equity partnership, so Moonstar Co might not face the threat to its credit rating which it would if it obtained ordinary loan finance for the development. A Mudaraba contract would also represent a diversification of sources of finance. It would not require the commitment to pay interest that loan finance would involve.

Moonstar Co would maintain control over the running of the project. A Mudaraba contract would offer a method of obtaining equity funding without the dilution of control which an issue of shares to external shareholders would bring. This is likely to make it appealing to Moonstar Co’s directors, given their desire to maintain a dominant influence over the business.

The bank would be concerned about the uncertainties regarding the rental income from the development. Although the lack of involvement by the bank might appeal to Moonstar Co's directors, the bank might not find it so attractive. The bank might be concerned about information asymmetry – that Moonstar Co’s management might be reluctant to supply the bank with the information it needs to judge how well its investment is performing.

(b) Briefly explain the two types of informal communication known as the grapevine and rumour. (6 marks)

(b) The grapevine and rumour are the two main types of informal communication.

The grapevine is probably the best known type of informal communication. All organisations have a grapevine and it will thrive if there is lack of information and consequently employees will make assumptions about events. In addition, insecurity,gossip about issues and fellow employees, personal animosity between employees or managers or new information that has not yet reached the formal communication system, will all drive the grapevine.

Rumours are the other main informal means of communication and are often active if there is a lack of formal communication.A rumour is inevitably a communication not based on verified facts and may therefore be true or false. Rumours travel quickly(often quicker than both the formal system and the grapevine) and can influence those who hear them and cause confusion,especially if bad news is the basis of the rumour. Managers must ensure that the formal communication system is such that rumours can be stopped, especially since they can have a serious negative effect on employees.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2021-03-12

- 2021-06-10

- 2021-04-24

- 2021-06-05

- 2021-05-12

- 2021-03-10

- 2021-06-24

- 2021-03-12

- 2021-03-11

- 2021-03-12

- 2021-01-02

- 2021-03-11

- 2021-07-19

- 2021-05-11

- 2021-05-08

- 2021-03-12

- 2021-04-15

- 2021-05-25

- 2021-06-01

- 2021-01-05

- 2021-05-25

- 2021-05-06

- 2021-03-10

- 2021-05-09

- 2021-05-21

- 2021-04-14

- 2021-05-12

- 2021-03-12

- 2021-03-12

- 2021-03-11