速看:山西省2020年9月ACCA考试常规报名结束时间是哪一天

发布时间:2020-07-04

各位小伙伴注意了,山西省2020年9月ACCA考试报名正在火热进行中,本次考试常规报名的截止日期是:7月27日。小伙伴们要注意安排好自己的考试计划。

以下是山西省9月份ACCA考试报名的具体费用详情。

注册相关ACCA官方提示:

ACCA 注重学员学习的独立性,很多事项是由ACCA英国总部直接与学员联系。为避免由于疏忽造成延误,特此列出以下注意事项,请学员关注:

1、您在完成网上注册、上传了符合要求的完整材料且在线缴费成功之后,将在三周左右收到英国总部确认注册成功的电子邮件;如果您是采用邮寄的方式递送材料到英国,英国总部的处理时间会相对较长,大概需要六周左右时间才能收到英国的确认邮件。

2、ACCA注册报名没有截止日期。您申请注册成功后,才能根据所处的考试报名时段申请参加ACCA的考试。如有任何问题(有关注册材料、免试及费用问题)需要联系总部解决,请发邮件到ACCA CONNECT:http://www.accaglobal.com/en/footertoolbar/contact-us.html。

以上就是今天分享的全部内容,希望各位报考的小伙伴们能保持良好的心态,积极的学习态度,51题库考试学习网祝你们顺利通过考试!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(d) Sirus raised a loan with a bank of $2 million on 1 May 2007. The market interest rate of 8% per annum is to

be paid annually in arrears and the principal is to be repaid in 10 years time. The terms of the loan allow Sirus

to redeem the loan after seven years by paying the full amount of the interest to be charged over the ten year

period, plus a penalty of $200,000 and the principal of $2 million. The effective interest rate of the repayment

option is 9·1%. The directors of Sirus are currently restructuring the funding of the company and are in initial

discussions with the bank about the possibility of repaying the loan within the next financial year. Sirus is

uncertain about the accounting treatment for the current loan agreement and whether the loan can be shown as

a current liability because of the discussions with the bank. (6 marks)

Appropriateness of the format and presentation of the report and quality of discussion (2 marks)

Required:

Draft a report to the directors of Sirus which discusses the principles and nature of the accounting treatment of

the above elements under International Financial Reporting Standards in the financial statements for the year

ended 30 April 2008.

(d) Repayment of the loan

If at the beginning of the loan agreement, it was expected that the repayment option would not be exercised, then the effective

interest rate would be 8% and at 30 April 2008, the loan would be stated at $2 million in the statement of financial position

with interest of $160,000 having been paid and accounted for. If, however, at 1 May 2007, the option was expected to be

exercised, then the effective interest rate would be 9·1% and at 30 April 2008, the cash interest paid would have been

$160,000 and the interest charged to the income statement would have been (9·1% x $2 million) $182,000, giving a

statement of financial position figure of $2,022,000 for the amount of the financial liability. However, IAS39 requires the

carrying amount of the financial instrument to be adjusted to reflect actual and revised estimated cash flows. Thus, even if

the option was not expected to be exercised at the outset but at a later date exercise became likely, then the carrying amount

would be revised so that it represented the expected future cash flows using the effective interest rate. As regards the

discussions with the bank over repayment in the next financial year, if the loan was shown as current, then the requirements

of IAS1 ‘Presentation of Financial Statements’ would not be met. Sirus has an unconditional right to defer settlement for longer

than twelve months and the liability is not due to be legally settled in 12 months. Sirus’s discussions should not be considered

when determining the loan’s classification.

It is hoped that the above report clarifies matters.

(ii) The percentage change in revenue, total costs and net assets during the year ended 31 May 2008 that

would have been required in order to have achieved a target ROI of 20% by the Beetown centre. Your

answer should consider each of these three variables in isolation. State any assumptions that you make.

(6 marks)

(ii) The ROI of Beetown is currently 13·96%. In order to obtain an ROI of 20%, operating profit would need to increase to

(20% x $3,160,000) = $632,000, based on the current level of net assets. Three alternative ways in which a target

ROI of 20% could be achieved for the Beetown centre are as follows:

(1) Attempts could be made to increase revenue by attracting more clients while keeping invested capital and operating

profit per $ of revenue constant. Revenue would have to increase to $2,361,644, assuming that the current level

of profitability is maintained and fixed costs remain unchanged. The current rate of contribution to revenue is

$2,100,000 – $567,000 = $1,533,000/$2,100,000 = 73%. Operating profit needs to increase by $191,000

in order to achieve an ROI of 20%. Therefore, revenue needs to increase by $191,000/0·73 = $261,644 =

12·46%.

(2) Attempts could be made to decrease the level of operating costs by, for example, increasing the efficiency of

maintenance operations. This would have the effect of increasing operating profit per $ of revenue. This would

require that revenue and invested capital were kept constant. Total operating costs would need to fall by $191,000

in order to obtain an ROI of 20%. This represents a percentage decrease of 191,000/1,659,000 = 11·5%. If fixed

costs were truly fixed, then variable costs would need to fall to a level of $376,000, which represents a decrease

of 33·7%.

(3) Attempts could be made to decrease the net asset base of HFG by, for example, reducing debtor balances and/or

increasing creditor balances, while keeping turnover and operating profit per $ of revenue constant. Net assets

would need to fall to a level of ($441,000/0·2) = $2,205,000, which represents a percentage decrease

amounting to $3,160,000 – $2,205,000 = 955,000/3,160,000 = 30·2%.

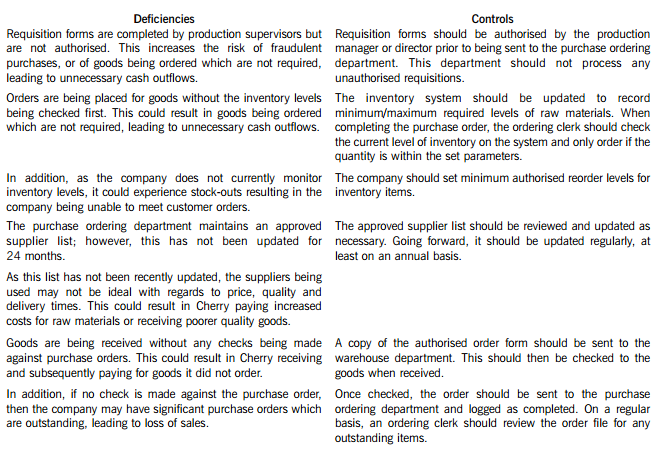

Cherry Blossom Co (Cherry) manufactures custom made furniture and its year end is 30 April. The company purchases its raw materials from a wide range of suppliers. Below is a description of Cherry’s purchasing system.

When production supervisors require raw materials, they complete a requisition form. and this is submitted to the purchase ordering department. Requisition forms do not require authorisation and no reference is made to the current inventory levels of the materials being requested. Staff in the purchase ordering department use the requisitions to raise sequentially numbered purchase orders based on the approved suppliers list, which was last updated 24 months ago. The purchasing director authorises the orders prior to these being sent to the suppliers.

When the goods are received, the warehouse department verifies the quantity to the suppliers despatch note and checks that the quality of the goods received are satisfactory. They complete a sequentially numbered goods received note (GRN) and send a copy of the GRN to the finance department.

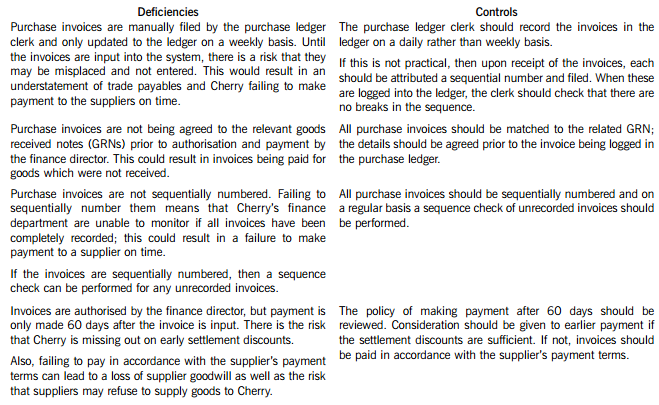

Purchase invoices are sent directly to the purchase ledger clerk, who stores them in a manual file until the end of each week. He then inputs them into the purchase ledger using batch controls and gives each invoice a unique number based on the supplier code. The invoices are reviewed and authorised for payment by the finance director, but the actual payment is only made 60 days after the invoice is input into the system.

Required:

In respect of the purchasing system of Cherry Blossom Co:

(i) Identify and explain FIVE deficiencies; and

(ii) Recommend a control to address each of these deficiencies.

Note: The total marks will be split equally between each part.

Cherry Blossom Co’s (Cherry) purchasing system deficiencies and controls

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-09-03

- 2021-02-13

- 2021-04-09

- 2021-09-12

- 2020-01-10

- 2020-09-03

- 2021-01-13

- 2020-01-08

- 2020-03-06

- 2021-04-17

- 2020-08-12

- 2020-01-10

- 2020-01-10

- 2020-08-12

- 2020-02-22

- 2020-01-09

- 2021-01-13

- 2020-04-15

- 2019-03-16

- 2020-09-03

- 2020-01-10

- 2020-01-09

- 2020-01-10

- 2021-01-13

- 2021-01-29

- 2021-04-04

- 2020-09-03

- 2020-03-05

- 2019-12-29

- 2020-01-09