不是财会专业的,可不可以报考ACCA?了解一下吧!

发布时间:2020-03-06

了解过ACCA的同学都知道,ACCA的报考门槛并不高。原则上,只要年满16周岁就可以报考ACCA,不论任何专业都能申请成为ACCA学员。那么,不是财会专业的人,可不可以报考ACCA?51题库考试学习网带领大家一起来了解一下。

大多数非财会专业考生的基础都薄弱,甚至是零基础,所以学起来会比相关专业的同学慢很多,而且ACCA一共要考15门科目,那是不是要花费更久的时间学习备考?

其实,不然。ACCA课程体系非常完善,难度也是呈阶梯式,很适合零基础的小伙伴学习,当然如果选择自学的话,可能就会花费更多的精力和时间,效率比较低,但是,对于基础薄弱或者零基础的非财会人士来说,学好ACCA同样不在话下。

当然,对于非财会专业的考生要重视基础阶段,ACCA课程总共分为应用知识、应用技能和战略课程三大阶段,由浅入深。因此初学者一定要学好前几门基础课程,必要时要留给自己充分备考的时间,把课堂内容、教材合理的结合起来把打好基础,才能在后面阶段的更好的提升能力!

那么,如何才能更快地拿下ACCA证书呢?

1.在没有报名之前想检测一下自己的英文水平,用现有的英文水平去阅读历年真题,不用急着知道答案,先看自己能否看明白题意等等,然后给自己的水平打分。要有一个大概的粗框架。ACCA每门科目大约需要150-200小时准备。时间的长短取决于课程本身的难易、你原先对这方面知识的了解程度、时间安排的效率等诸多因素。如果你每周看书做题20-2小时,同时准备三门课要大约20周的时间。如果你觉得时间不够,就不要好高骛远,一次考两门为佳。

2.安排切实可行的计划。当你完成了ACCA考试报名并购买了教材后,根据书的厚度,练习题量的多少,安排一个切实的学习计划。但不要太笼统,比如说,“我要1个月内看完三本书”。先要看一下你自己的阅读速度,10page每小时大概是一个比较实际的速度。当然,各人情况不同,自己先测试一下。之后看一下练习题有多少题,估算一下练习时间。每道题都有分值的,如果考试的时候,10分值的题目只能分配18分钟时间。作为练习,时间可以多一些,因为除了做题,你还要分析答案。所以10分值的题可以是大约用25-30分钟,一道20-30分值的中型题,最少要一个小时。这样,整本练习册需要多少时间就基本上清楚了,也不需要全部的题目都做,以“动手做2/3,仔细阅读分析另1/3”的大概原则,或者也可以6/4开,但每一道题至少必须认真看过一遍答案。

3.ACCA历年真题要充分利用有不少题目被直接拷贝到练习册中,也有些题目是被做过略微修改。所以,到做全真题的时候会觉得很多题目都似曾相识。不过,做全真题的目的不是做题,而是让大家在真正的时间压力下感受一下考试的感觉,考验一下你答题,尤其是写字的速度。

4.基本上估算了所需的准备时间后,可以制定一个完善的计划。

5.根据实际情况调整计划进度计划不要排得太满,万一碰到工作很忙或者学习很紧张,还可以与空时相互调剂。要严格按计划执行,我的经验时至少要认真完成90-95%。另外,开始执行后的1个月左右做一次总结,根据实际情况适当调整计划的进度。

6.安排好临考前的几天计划临阵磨枪,不快也光,所以临考前的几天是很重要的。如果能请3-5天的假在家好好看书。把时间分配给做历年全真题,以及自己平时总结的study notes等。不要忘了,在仔细研究考试答案同时,别忘了仔细阅读主考出题人针对考试的评论。还有,就是student accountants中的相关文章。

好了,以上就是今天分享的内容。如果还想了解更多信息,欢迎来51题库考试学习网留言。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(ii) the recent financial performance of Merton plc from a shareholder perspective. Clearly identify any

issues that you consider should be brought to the attention of the ordinary shareholders. (15 marks)

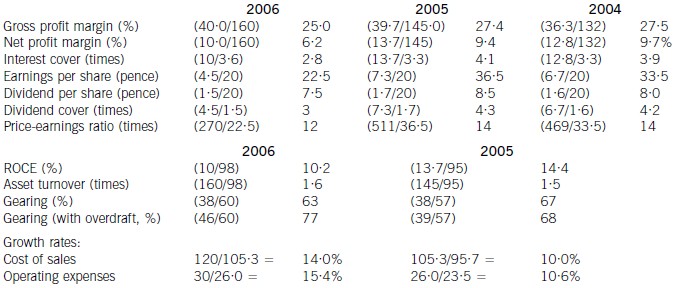

(ii) Discussion of financial performance

It is clear that 2006 has been a difficult year for Merton plc. There are very few areas of interest to shareholders where

anything positive can be found to say.

Profitability

Return on capital employed has declined from 14·4% in 2005, which compared favourably with the sector average of

12%, to 10·2% in 2006. Since asset turnover has improved from 1·5 to 1·6 in the same period, the cause of the decline

is falling profitability. Gross profit margin has fallen each year from 27·5% in 2004 to 25% in 2006, equal to the sector

average, despite an overall increase in turnover during the period of 10% per year. Merton plc has been unable to keep

cost of sales increases (14% in 2006 and 10% in 2005) below the increases in turnover. Net profit margin has declined

over the same period from 9·7% to 6·2%, compared to the sector average of 8%, because of substantial increases in

operating expenses (15·4% in 2006 and 10·6% in 2005). There is a pressing need here for Merton plc to bring cost

of sales and operating costs under control in order to improve profitability.

Gearing and financial risk

Gearing as measured by debt/equity has fallen from 67% (2005) to 63% (2006) because of an increase in

shareholders’ funds through retained profits. Over the same period the overdraft has increased from £1m to £8m and

cash balances have fallen from £16m to £1m. This is a net movement of £22m. If the overdraft is included, gearing

has increased to 77% rather than falling to 63%.

None of these gearing levels compare favourably with the average gearing for the sector of 50%. If we consider the large

increase in the overdraft, financial risk has clearly increased during the period. This is also evidenced by the decline in

interest cover from 4·1 (2005) to 2·8 (2006) as operating profit has fallen and interest paid has increased. In each year

interest cover has been below the sector average of eight and the current level of 2·8 is dangerously low.

Share price

As the return required by equity investors increases with increasing financial risk, continued increases in the overdraft

will exert downward pressure on the company’s share price and further reductions may be expected.

Investor ratios

Earnings per share, dividend per share and dividend cover have all declined from 2005 to 2006. The cut in the dividend

per share from 8·5 pence per share to 7·5 pence per share is especially worrying. Although in its announcement the

company claimed that dividend growth and share price growth was expected, it could have chosen to maintain the

dividend, if it felt that the current poor performance was only temporary. By cutting the dividend it could be signalling

that it expects the poor performance to continue. Shareholders have no guarantee as to the level of future dividends.

This view could be shared by the market, which might explain why the price-earnings ratio has fallen from 14 times to

12 times.

Financing strategy

Merton plc has experienced an increase in fixed assets over the last period of £10m and an increase in stocks and

debtors of £21m. These increases have been financed by a decline in cash (£15m), an increase in the overdraft (£7m)

and an increase in trade credit (£6m). The company is following an aggressive strategy of financing long-term

investment from short-term sources. This is very risky, since if the overdraft needed to be repaid, the company would

have great difficulty in raising the funds required.

A further financing issue relates to redemption of the existing debentures. The 10% debentures are due to be redeemed

in two years’ time and Merton plc will need to find £13m in order to do this. It does not appear that this sum can be

raised internally. While it is possible that refinancing with debt paying a lower rate of interest may be possible, the low

level of interest cover may cause concern to potential providers of debt finance, resulting in a higher rate of interest. The

Finance Director of Merton plc needs to consider the redemption problem now, as thought is currently being given to

raising a substantial amount of new equity finance. This financing choice may not be available again in the near future,

forcing the company to look to debt finance as a way of effecting redemption.

Overtrading

The evidence produced by the financial analysis above is that Merton plc is showing some symptoms of overtrading

(undercapitalisation). The board are suggesting a rights issue as a way of financing an expansion of business, but it is

possible that a rights issue will be needed to deal with the overtrading problem. This is a further financing issue requiring

consideration in addition to the redemption of debentures mentioned earlier.

Conclusion

Ordinary shareholders need to be aware of the following issues.

1. Profitability has fallen over the last year due to poor cost control

2. A substantial increase in the overdraft over the last year has caused gearing to increase

3. It is possible that the share price will continue to fall

4. The dividend cut may warn of continuing poor performance in the future

5. A total of £13m of debentures need redeeming in two year’s time

6. A large amount of new finance is needed for working capital and debenture redemption

Appendix: Analysis of key ratios and financial information

10 Which of the following factors would cause a company’s gearing ratio to fall?

1 A bonus issue of ordinary shares.

2 A rights issue of ordinary shares.

3 An issue of loan notes.

4 An upward revaluation of non-current assets.

A 1 and 3

B 2 and 3

C 1 and 4

D 2 and 4

6 Charles and Jane Miro, aged 31 and 34 years respectively, have been married for ten years and have two children

aged six and eight years. Charles is a teacher but for the last five years he has stayed at home to look after their

children. Jane works as a translator for Speak Write Ltd.

Speak Write Ltd was formed and began trading on 6 April 2006. It provides translation services to universities. Jane,

who ceased employment with Barnham University to found the company, owns 100% of its ordinary share capital

and is its only employee.

Speak Write Ltd has translated documents for four different universities since it began trading. Its biggest client is

Barnham University which represents 70% of the company’s gross income. It is estimated that the company’s gross

fee income for its first 12 months of trading will be £110,000. Speak Write Ltd usually agrees fixed fees in advance

with its clients although it charges for some projects by reference to the number of days taken to do the work. None

of the universities makes any payment to Speak Write Ltd in respect of Jane being on holiday or sick.

All of the universities insist that Jane does the work herself. Jane carries out the work for three of the universities in

her office at home using a computer and specialised software owned by Speak Write Ltd. The work she does for

Barnham University is done in the university’s library on one of its computers as the documents concerned are too

delicate to move.

The first set of accounts for Speak Write Ltd will be drawn up for the year ending 5 April 2007. It is estimated that

the company’s tax adjusted trading profit for this period will be £52,500. This figure is after deducting Jane’s salary

of £4,000 per month and the related national insurance contributions but before any adjustments required by the

application of the personal service companies (IR 35) legislation. The company has no other sources of income or

capital gains.

Jane has not entered into any communication with HM Revenue and Customs (HMRC) with respect to the company

and wants to know:

– When the corporation tax computation should be submitted and when the tax is due.

– When the corporation tax computation can be regarded as having been agreed by HMRC.

Charles and Jane have requested a meeting to discuss the family’s finances. In particular, they wish to consider the

shortfall in the family’s annual income and any other related issues if Jane were to die. Their mortgage is covered

by a term assurance policy but neither of them have made any pension contributions or carried out any other long

term financial planning.

Jane has estimated that her annual after tax income from Speak Write Ltd, on the assumption that she extracts all of

the company’s profits, will be £58,000. Charles owns two investment properties that together generate after tax

income of £8,500. He estimates that he could earn £28,000 after tax if he were to return to work.

The couple’s annual surplus income, after payment of all household expenditure including mortgage payments of

£900 per month, is £21,000. Charles and Jane have no other sources of income.

Required:

(a) Write a letter to Jane setting out:

(i) the arguments that HMRC could put forward, based only on the facts set out above, in support of

applying the IR 35 legislation to Speak Write Ltd; and

(ii) the additional income tax and national insurance contributions that would be payable, together with

their due date of payment, if HMRC applied the IR 35 legislation to all of the company’s income in

2006/07. (11 marks)

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-09

- 2020-01-10

- 2020-01-09

- 2020-02-20

- 2020-05-01

- 2020-01-10

- 2020-10-09

- 2019-07-21

- 2020-05-17

- 2020-03-05

- 2020-03-19

- 2020-01-10

- 2020-03-11

- 2020-01-08

- 2020-03-13

- 2020-03-06

- 2020-03-04

- 2020-01-10

- 2020-01-09

- 2019-12-27

- 2020-08-13

- 2020-03-04

- 2019-07-21

- 2020-04-18

- 2020-04-21

- 2020-01-09

- 2020-01-10

- 2020-03-04

- 2020-01-09

- 2020-01-08