快来浏览本文!ACCA笔考应该使用什么样的笔答题

发布时间:2020-01-10

截止到2020年,ACCA 战略阶段考试依旧沿用着笔考的模式,那么,在准备这类考试时,我们需要用哪类笔进行答题呢?今天51题库考试学习网给大家普及一下。

ACCA考试要用黑色圆珠笔!!不限牌子不限笔头粗细,只要你用得顺手写得顺畅就行!!大家平时做练习时可以开始习惯下了,考试多备几支,有备无患!

因现在ACCA现在用的是扫描系统,你的做答将扫描回英国而不是再像过去邮寄回英国,如果不按照ACCA的要求用笔,会影响扫描的效果,从而影响考试成绩.

ACCA考试一定要用黑色圆珠笔,不可以用黑色中性笔(水笔),中性笔不能保证都能扫描成功,之前已经有学员通过邮件向ACCA总部确认过中性笔的问题,总部和负责扫描的公司确认过了,希望大家注意不要因此影响我们的考试成绩。

ACCA的相关内容,一起了解一下。

★全面完善的课程体系

ACCA的课程使学员全面掌握财务、财务管理、审计、税务及经营战略等方面的专业知识,提升分析能力并拓宽战略思维。

★理论与实际的密切结合

ACCA的专业资格是理论知识与实际经验的高度紧密结合。新考试大纲充分表达了雇主和专业人士的意见,反映了现代商务社会对财会人员的要求。

★对专业价值和职业操守的重点强调

ACCA创举性地开设了在线职业操守训练课程,它给予学员一系列的职业操守的理念,并设置了多个自我测试题,检验学员职业操守的价值观和行为。取得ACCA会员资格要完成三个“E”,即通过考试、完成在线职业操守训练课程、并取得三年相关工作经验。

★国际标准与本地实情的和谐统一

ACCA考试大纲以国际会计准则/国际财务报告准则和国际审计准则作为依据设计考试内容,并提供了包括中国在内的40多种不同国家和地区的法律与税务方面的试卷,这使得ACCA成为最切合中国实际的国际性会计师资格。

★公平一致的考试标准

ACCA的专业资格考试采用全球统一标准,即统一教材、统一考试、统一评卷,最后会员取得全球统一的证书。

★遍布全球的考点网络

学员在一个国家向ACCA注册后,可根据需要在全球350多个考点中选择、更换适合自己的考试中心。

★认证与学位的相互补充

ACCA在全球范围内寻求与优秀院校的广泛合作。满足一定的条件后,ACCA学员将有机会获得英国牛津-布鲁克斯大学应用会计理学士学位。

今日分享时间到此结束啦,如果大家觉得意犹未尽,还想了解更多内容的话,敬请关注51题库考试学习网。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) Calculate the value of the closing stocks of finished goods at the end of the three-month period, and the value

of cost of sales for the period. (3 marks)

(b) Opening stock of finished goods = £69,800

Closing stock of finished goods = 2,000 x 18·66 = £37,320

Cost of sales for three-month period = 69,800 + 2,262,380 – 37,320 = £2,294,860

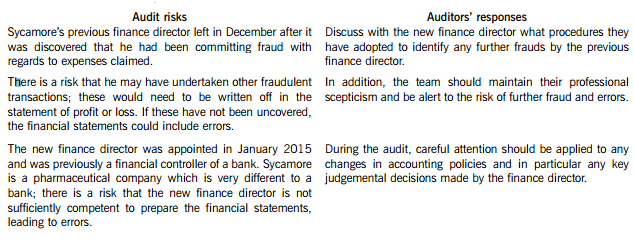

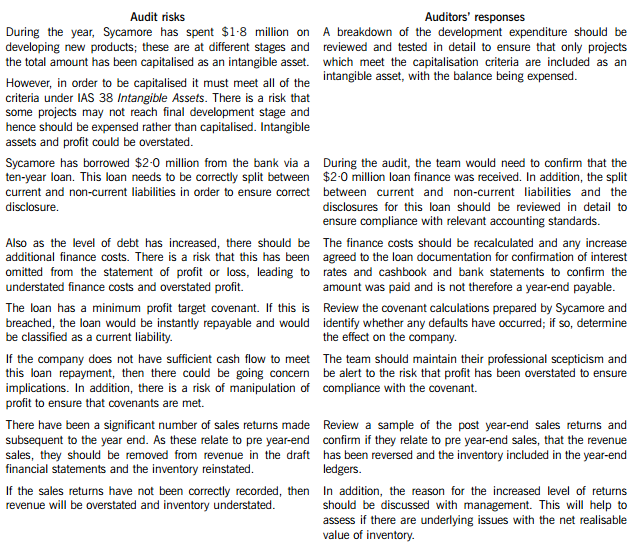

You are the audit supervisor of Maple & Co and are currently planning the audit of an existing client, Sycamore Science Co (Sycamore), whose year end was 30 April 2015. Sycamore is a pharmaceutical company, which manufactures and supplies a wide range of medical supplies. The draft financial statements show revenue of $35·6 million and profit before tax of $5·9 million.

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

(a) Fraud responsibility

Maple & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error.

In order to fulfil this responsibility, Maple & Co is required to identify and assess the risks of material misstatement of the financial statements due to fraud.

They need to obtain sufficient appropriate audit evidence regarding the assessed risks of material misstatement due to fraud, through designing and implementing appropriate responses. In addition, Maple & Co must respond appropriately to fraud or suspected fraud identified during the audit.

When obtaining reasonable assurance, Maple & Co is responsible for maintaining professional scepticism throughout the audit, considering the potential for management override of controls and recognising the fact that audit procedures which are effective in detecting error may not be effective in detecting fraud.

To ensure that the whole engagement team is aware of the risks and responsibilities for fraud and error, ISAs require that a discussion is held within the team. For members not present at the meeting, Sycamore’s audit engagement partner should determine which matters are to be communicated to them.

(b) Audit risks and auditors’ responses

(c) (i) Review engagements

Review engagements are often undertaken as an alternative to an audit, and involve a practitioner reviewing financial data, such as six-monthly figures. This would involve the practitioner undertaking procedures to state whether anything has come to their attention which causes the practitioner to believe that the financial data is not in accordance with the financial reporting framework.

A review engagement differs to an external audit in that the procedures undertaken are not nearly as comprehensive as those in an audit, with procedures such as analytical review and enquiry used extensively. In addition, the practitioner does not need to comply with ISAs as these only relate to external audits.

(ii) Levels of assurance

The level of assurance provided by audit and review engagements is as follows:

External audit – A high but not absolute level of assurance is provided, this is known as reasonable assurance. This provides comfort that the financial statements present fairly in all material respects (or are true and fair) and are free of material misstatements.

Review engagements – where an opinion is being provided, the practitioner gathers sufficient evidence to be satisfied that the subject matter is plausible; in this case negative assurance is given whereby the practitioner confirms that nothing has come to their attention which indicates that the subject matter contains material misstatements.

(c) Briefly outline the corporation tax (CT) issues that Tay Limited should consider when deciding whether to

acquire the shares or the assets of Tagus LDA. You are not required to discuss issues relating to transfer

pricing. (7 marks)

(c) (1) Acquisition of shares

Status

The acquisition of shares in Tagus LDA will add another associated company to the group. This may have an adverse

effect on the rates of corporation tax paid by the two existing group companies, particularly Tay Limited.

Taxation of profits

Profits will be taxed in Portugal. Any profits remitted to the UK as dividends will be taxable as Schedule D Case V income,

but will attract double tax relief. Double tax relief will be available against two types of tax suffered in Portugal. Credit

will be given for any tax withheld on payments from Tagus LDA to Tay Limited and relief will also be available for the

underlying tax as Tay Limited owns at least 10% of the voting power of Tagus LDA. The underlying tax is the tax

attributable to the relevant profits from which the dividend was paid. Double tax relief is given at the lower rate of the

UK tax and the foreign tax (withholding and underlying taxes) suffered.

Losses

As Tagus LDA is a non-UK resident company, losses arising in Tagus LDA cannot be group relieved against profits of the

two UK companies. Similarly, any UK trading losses cannot be used against profits generated by Tagus LDA.

(2) Acquisition of assets

Status

The business of Tagus will be treated as a branch of Tay Limited i.e. an extension of the UK company’s activities. The

number of associated companies will be unaffected.

Taxation of profits

Tay Limited will be treated as having a permanent establishment in Portugal. Profits attributable to the Tagus business

will thus still be taxed in Portugal. In addition, the profits will be taxed in the UK as trading income. Double tax relief

will be available for the tax already suffered in Portugal at the lower of the two rates.

Capital allowances will be available. As the assets in question will not previously have been subject to a claim for UK

capital allowances, there will be no cost restriction and the consideration attributable to each asset will form. the basis

for the capital allowance claim.

Losses

The Tagus trade is part of Tay Limited’s trade, so any losses incurred by the Portuguese trade will automatically be offset

against the trading profits of the UK trade, and vice versa.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-10

- 2020-03-13

- 2021-05-07

- 2020-01-10

- 2020-04-08

- 2020-01-10

- 2020-01-09

- 2021-09-12

- 2020-04-28

- 2020-02-29

- 2020-01-09

- 2020-01-09

- 2020-04-15

- 2020-04-10

- 2020-01-10

- 2020-04-10

- 2020-05-20

- 2020-01-29

- 2020-01-29

- 2020-02-14

- 2020-01-10

- 2020-03-07

- 2020-03-07

- 2020-02-28

- 2019-03-17

- 2020-01-10

- 2019-03-30

- 2020-04-11

- 2020-04-18

- 2020-03-18