不清楚会计学硕士能免考几门ACCA,那就来本文了解一下吧!

发布时间:2020-02-01

众所周知,在ACCA官方公布的免试政策里面,会计学硕士是可以免考ACCA9门。那么,是不是所有学校的会计学硕士都可以免考ACCA9门呢?一起来看看下面的内容吧!

首先让我们先看一下ACCA免试政策情况。

ACCA的免试政策具体是这样的:

1.教育部认可高校毕业生:

(1)会计专业-获得学士学位,免试F1-F5;

(2)会计-辅修专业,免试F1-F3;

(3)金融-免试F1-F3;

(4)法律专业-免试F4;

(5)商务及管理专业,免试F1;

(6)MPAcc专业,免试F1-F9;

(7)MBA,免试F1-F3。

2.教育部认可高校在校生(本科)

(1)会计专业-完成第一学年课程,无免试;

(2)会计专业-完成第二学年课程,免试F1-F3;

(3)会计专业-完成第三学年课程,免试F1-F5。

3.2009年以前CICPA全科通过的,免试F1-F4和F6。2009年以后通过6+1的CICPA可以免考ACCA9科。

其次,我们应该关注一下会计学硕士免考ACCA的注意事项:

1.在校生只有顺利通过整学年的课程才能够申请免试。

2.针对在校生的部分课程免试政策只适用于会计学专业全日制大学本科的在读学生,而不适用于硕士学位或大专学历的在读学生。

3.已完成MPAcc学位大纲规定课程,还需完成论文的学员也可注册并申请免试。但须提交由学校出具的通过所有MPAcc学位大纲规定课程的成绩单,并附注“该学员已通过所有MPAcc学位大纲规定课程,论文待完成”的说明。

4.特许学位(即海外大学与中国本地大学合作而授予海外大学学位的项目)—部分完成时不能申请免试。

5.本政策适用于在中国教育部认可的高等院校全部完成或部分完成本科课程的学生,而不考虑目前居住地点。

6.欲申请牛津布鲁克斯大学学士学位的学员需放弃F7-F9的免试。

今日分享时间到此结束啦,以上信息就是51题库考试学习网针对小伙伴们的问题做出的详细解答,相信小伙伴们看过之后也有了一定的了解了吧,如果大家还有什么疑问,欢迎大家前来咨询51题库考试学习网,我们会第一时间为大家答疑解惑。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

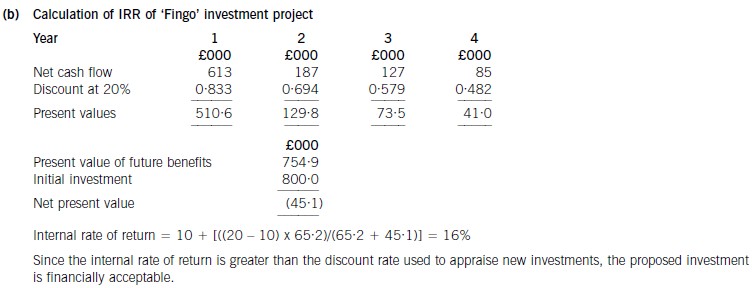

(b) Calculate the internal rate of return of the proposed investment and comment on your findings. (5 marks)

(ii) Calculate the probability of the net profit being less than £75 million. (2 marks)

3 (a) Discuss why the identification of related parties, and material related party transactions, can be difficult for

auditors. (5 marks)

3 Pulp Co

(a) Identification of related parties

Related parties and associated transactions are often difficult to identify, as it can be hard to establish exactly who, or what,

are the related parties of an entity. IAS 24 Related Party Disclosures contains definitions which in theory serve to provide a

framework for identifying related parties, but deciding whether a definition is met can be complex and subjective. For example,

related party status can be obtained via significant interest, but in reality it can be difficult to establish the extent of influence

that potential related parties can actually exert over a company.

The directors may be reluctant to disclose to the auditors the existence of related parties or transactions. This is an area of

the financial statements where knowledge is largely confined to management, and the auditors often have little choice but to

rely on full disclosure by management in order to identify related parties. This is especially the case for a close family member

of those in control or having influence over the entity, whose identity can only be revealed by management.

Identification of material related party transactions

Related party transactions may not be easy to identify from the accounting systems. Where accounting systems are not

capable of separately identifying related party transactions, management need to carry out additional analysis, which if not

done makes the transactions extremely difficult for auditors to find. For example sales made to a related party will not

necessarily be differentiated from ‘normal’ sales in the accounting systems.

Related party transactions may be concealed in whole, or in part, from auditors for fraudulent purposes. A transaction may

not be motivated by normal business considerations, for example, a transaction may be recognised in order to improve the

appearance of the financial statements by ‘window dressing’. Clearly if the management is deliberately concealing the true

nature of these items it will be extremely difficult for the auditor to discover the rationale behind the transaction and to consider

the impact on the financial statements.

Finally, materiality is a difficult concept to apply to related party transactions. Once a transaction has been identified, the

auditor must consider whether it is material. However, materiality has a particular application in this situation. ISA 550

Related Parties states that the auditor should consider the effect of a related party transaction on the financial statements.

The problem is that a transaction could occur at an abnormally small, even nil, value. Determining materiality based on

monetary value is therefore irrelevant, and the auditor should instead be alert to the unusual nature of the transaction making

it material.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-09

- 2020-05-13

- 2019-12-27

- 2020-03-07

- 2020-04-03

- 2020-05-16

- 2020-05-17

- 2020-04-10

- 2020-04-20

- 2020-03-28

- 2020-01-09

- 2020-05-16

- 2020-03-22

- 2020-01-09

- 2020-02-13

- 2020-05-14

- 2020-04-07

- 2020-01-09

- 2020-03-13

- 2020-05-16

- 2020-02-19

- 2020-02-19

- 2020-03-21

- 2020-03-18

- 2020-02-19

- 2020-03-15

- 2020-04-21

- 2020-01-09

- 2020-01-09

- 2019-12-25