请问什么情况下陕西省考生ACCA国际会计师证书会被注销呢?

发布时间:2020-01-09

目前,有不少通过自己的努力已经考过ACCA考试进入证书申请阶段的同学出现了新的疑问:ACCA证书有有效年限吗?怎么样才能一直保持ACCA会员资格呢?有些什么规定会导致取消ACCA会员资格导致证书被吊销呢?接下来,51题库考试学习网一一解答大家心中的疑惑,避免在领证之路上出现一些不必要的意外。

首先,ACCA证书是不会过期的,拿到了ACCA证书就是终身有效的,但终身有效的前提是:只要成为ACCA会员以后每年维持ACCA年费的正常支付,就可以保持ACCA资格。

需要注意的是:但是在成为ACCA会员之前,ACCA考试的时候成绩是有有效期的。

ACCA有效期新规显示,ACCAF阶段不再设有时间限制,从P阶段通过第一门开始算有七年有效期,如果七年内没有全部通过,成绩将全部作废,意思是就是在七年之后你就需要重新考试你已经考过的科目了。

以下是关于ACCA P阶段有效期的官方原文:

ACCA学员有七年的时间通过专业阶段的考试(即P1、P2和P3,以及P4-P7中的任选两门)。如果学员不能在七年内通过所有专业阶段考试,超过七年的已通过专业阶段科目的成绩将作废,须重新考试。七年时限从学员通过第一门专业阶段考试之日算起。

当然你必须要遵守以下的一些规定,否则你的ACCA会员资格会被取消,导致你无法正常领取证书:

1.最首要的就是,在ACCA学员阶段需要注意的是千万不要在考试的时候出现作弊的情况,一旦发现就会被取消ACCA会员资格

2.违反职业道德将会被直接除名。何为违反职业道德呢?其实就是类似于做假账之类的情况发生,无论是什么情况,出于知情或者不知情的情况下,一旦被发现,自己的ACCA职业生涯就宣告结束~

3.要维持ACCA会员资格只需要按时缴纳年费即可。那么不按时缴纳年费呢?首先你的ACCA会员资格将会暂时被取消,您的ACCA账户也将被冻结。当然这个也是暂时的,你只要及时的申请补缴信息,成功缴费就可以恢复会员的身份了。如果不需要ACCA会员这个头衔可以通过不缴纳年费这个方法来实现。

ACCA会不会和国内会计证书一样需要继续教育来继续维持会员资格呢?

答案是否定的。和国内会计证书不一样,国内会计证首先是有时间年限的,是需要继续教育来维持证书年限的,而ACCA并没有开设继续教育等课程,学员需要维持会员资格只需要按时缴纳年费即可。但是ACCA后续有许多拓展课程,例如obu学士学位,UCL伦敦大学硕士学位等等,都是在ACCA学习过程中可以考的。

那如果不小心没有按时缴费造成了账户被冻结的情况应该怎么办呢?

很简单,写封邮件向官方解释一下情况,并表达想恢复ACCA会员资格的意愿,并通过官方回复的渠道补交年费和一定数额的罚金即可回复ACCA会员资格了。温馨提示一下,由于ACCA官方是在英国,所以办理的时限可能会很长,因此建各位考生还是按时缴纳会费,避免不必要的影响。

以上就是关于ACCA考试证书申请流程和后续注意事宜的相关内容,希望对大家有所帮助,最后再次恭喜成功通过ACCA全科考试的同学们,成功上岸~

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(iii) assesses TSC in terms of financial performance, competitiveness, service quality, resource utilisation,

flexibility and innovation and discusses the interrelationships between these terms, incorporating

examples from within TSC; and (10 marks)

(iii) The terms listed may be seen as representative of the dimensions of performance. The dimensions may be analysed into

results and determinants.

The results may be measured by focusing on financial performance and competitiveness. Financial performance may

be measured in terms of revenue and profit as shown in the data in the appendix of the question in respect of TSC. The

points system in part (a) of the answer shows which depots have achieved or exceeded the target set. In addition,

liquidity is another aspect of the measurement of financial performance. The points total in part (a) showed that

Leonardotown and Michaelangelotown depots appear to have the best current record in aspects of credit control.

15

Competitiveness may be measured in terms of sales growth but also in terms of market share, number of new

customers, etc. In the TSC statistics available in (a) we only have data for the current quarter. This shows that three of

the four depots listed have achieved increased revenue compared to target.

The determinants are the factors which may be seen to contribute to the achievement of the results. Quality, resource

utilisation, flexibility and innovation are cited by Fitzgerald and Moon as examples of factors that should contribute to

the achievement of the results in terms of financial performance and competitiveness. In TSC a main quality issue

appears to be customer care and service delivery. The statistics in the points table in part (a) of the answer show that

the Raphaeltown depot appears to have a major problem in this area. It has only achieved one point out of the six

available in this particular segment of the statistics.

Resource utilisation for TSC may be measured by the level of effective use of drivers and vehicles. To some extent, this

is highlighted by the statistics relating to customer care and service delivery. For example, late collection of consignments

from customers may be caused by a shortage of vehicles and/or drivers. Such shortages could be due to staff turnover,

sickness, etc or problems with vehicle maintenance.

Flexibility may be an issue. There may, for example, be a problem with vehicle availability. Possibly an increased focus

on sources for short-term sub-contracting of vehicles/collections/deliveries might help overcome delay problems.

The ‘target v actual points system’ may be seen as an example of innovation by the company. This gives a detailed set

of measures that should provide an incentive for improvement at all depots. The points system may illustrate the extent

of achievement/non-achievement of company strategies for success. For example TSC may have a customer care

commitment policy which identifies factors that should be achieved on a continuing basis. For example, timely collection

of consignments, misdirected consignments re-delivered at no extra charge, prompt responses to customer claims and

compensation for customers.

(ii) the strategy of the business regarding its treasury policies. (3 marks)

(Marks will be awarded in part (b) for the identification and discussion of relevant points and for the style. of the

report.)

(ii) Strategy of the business regarding its treasury policies

Treasury policies are reviewed regularly by the Board. It is group policy to account for all financial instruments as cash

flow hedges. As a result, changes in the fair values of financial instruments are deferred in reserves to the extent the

hedge is effective and released to profit or loss in the time periods in which the hedged item impacts profit or loss.

The Group contracts fixed rate currency swaps and issues floating to fixed rate interest rate swaps to meet the objective

of protecting borrowing costs. The cash flow effects of the interest rate swaps match the cash flows on the underlying

instruments so that there is no net cash flow effect from movements in market interest rates. If the interest rate swaps

had not been transacted there could have been an increase in the annual net interest payable to the Group. The strategy

of the group is to minimise the exposure to interest rate fluctuations.

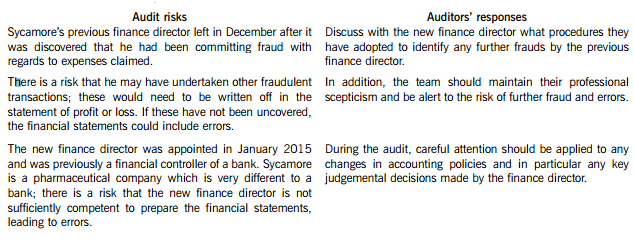

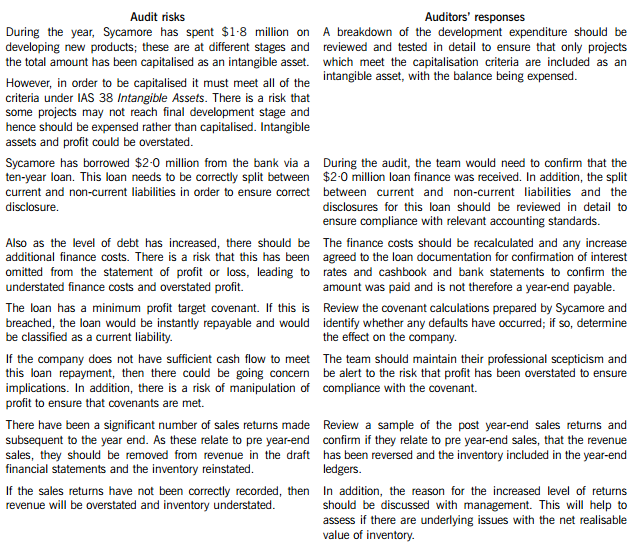

You are the audit supervisor of Maple & Co and are currently planning the audit of an existing client, Sycamore Science Co (Sycamore), whose year end was 30 April 2015. Sycamore is a pharmaceutical company, which manufactures and supplies a wide range of medical supplies. The draft financial statements show revenue of $35·6 million and profit before tax of $5·9 million.

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

(a) Fraud responsibility

Maple & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error.

In order to fulfil this responsibility, Maple & Co is required to identify and assess the risks of material misstatement of the financial statements due to fraud.

They need to obtain sufficient appropriate audit evidence regarding the assessed risks of material misstatement due to fraud, through designing and implementing appropriate responses. In addition, Maple & Co must respond appropriately to fraud or suspected fraud identified during the audit.

When obtaining reasonable assurance, Maple & Co is responsible for maintaining professional scepticism throughout the audit, considering the potential for management override of controls and recognising the fact that audit procedures which are effective in detecting error may not be effective in detecting fraud.

To ensure that the whole engagement team is aware of the risks and responsibilities for fraud and error, ISAs require that a discussion is held within the team. For members not present at the meeting, Sycamore’s audit engagement partner should determine which matters are to be communicated to them.

(b) Audit risks and auditors’ responses

(c) (i) Review engagements

Review engagements are often undertaken as an alternative to an audit, and involve a practitioner reviewing financial data, such as six-monthly figures. This would involve the practitioner undertaking procedures to state whether anything has come to their attention which causes the practitioner to believe that the financial data is not in accordance with the financial reporting framework.

A review engagement differs to an external audit in that the procedures undertaken are not nearly as comprehensive as those in an audit, with procedures such as analytical review and enquiry used extensively. In addition, the practitioner does not need to comply with ISAs as these only relate to external audits.

(ii) Levels of assurance

The level of assurance provided by audit and review engagements is as follows:

External audit – A high but not absolute level of assurance is provided, this is known as reasonable assurance. This provides comfort that the financial statements present fairly in all material respects (or are true and fair) and are free of material misstatements.

Review engagements – where an opinion is being provided, the practitioner gathers sufficient evidence to be satisfied that the subject matter is plausible; in this case negative assurance is given whereby the practitioner confirms that nothing has come to their attention which indicates that the subject matter contains material misstatements.

(b) Identify and explain the financial statement risks to be taken into account in planning the final audit.

(12 marks)

(b) Financial statement risks

Tutorial note: Note the timeframe. Financial statements for the year to 30 June 2006 are draft. Certain misstatements

may therefore exist due to year-end procedures not yet having taken place.

Revenue/(Receivables)

■ Revenue has increased by 11·8% ((161·5 – 144·4)/144·4 × 100). Overstatement could arise if rebates due to customers

have not yet been accounted for in full (as they are calculated in arrears). If rebates have still to be accounted for trade

receivables will be similarly overstated.

Materials expense

■ Materials expense has increased by 17·8% ((88.0 – 74·7)/74·7 × 100). This is more than the increase in revenue. This

could be legitimate (e.g. if fuel costs have increased significantly). However, the increase could indicate misclassification

of:

– revenue expenditure (see fall in other expenses below);

– capital expenditure (e.g. on overhauls or major refurbishment) as revenue;

– finance lease payments as operating lease.

Depreciation/amortisation

■ This has fallen by 10·5% ((8·5 – 9·5)/9·5 × 100). This could be valid (e.g. if Yates has significant assets already fully

depreciated or the asset base is lower since last year’s restructuring). However, there is a risk of understatement if, for

example:

– not all assets have been depreciated (or depreciated at the wrong rates, or only for 11 months of the year);

– cost of non-current assets is understated (e.g. due to failure to recognise capital expenditure)1;

– impairment losses have not been recognised (as compared with the prior year).

Tutorial note: Depreciation on vehicles and transport equipment represents only 7% of cost. If all items were being

depreciated on a straight-line basis over eight years this should be 12·5%. The depreciation on other equipment looks more

reasonable as it amounts to 14% which would be consistent with an average age of vehicles of seven years (i.e. in the middle

of the range 3 – 13 years).

Other expenses

■ These have fallen by 15·5% ((19·6 – 23·2)/23·2 × 100). They may have fallen (e.g. following the restructuring) or may be

understated due to:

– expenses being misclassified as materials expense;

– underestimation of accrued expenses (especially as the financial reporting period has not yet expired).

Intangibles

■ Intangible assets have increased by $1m (16% on the prior year). Although this may only just be material to the

financial statements as a whole (see (a)) this is the net movement, therefore additions could be material.

■ Internally-generated intangibles will be overstated if:

– any of the IAS 38 recognition criteria cannot be demonstrated;

– any impairment in the year has not yet been written off in accordance with IAS 36 ‘Impairment of Assets’.

Tangible assets

■ The net book value of property (at cost) has fallen by 5%, vehicles are virtually unchanged (increased by just 2·5%)

and other equipment (though the least material category) has fallen by 20·4%.

■ Vehicles and equipment may be overstated if:

– disposals have not been recorded;

– depreciation has been undercharged (e.g. not for a whole year);

– impairments have not yet been accounted for.

■ Understatement will arise if finance leases are treated as operating leases.

Receivables

■ Trade receivables have increased by just 2·2% (although sales increased by 11·8%) and may be understated due to a

cutoff error resulting in overstatement of cash receipts.

■ There is a risk of overstatement if sufficient allowances have not been made for the impairment of individually significant

balances and for the remainder assessed on a portfolio or group basis.

Restructuring provision

■ The restructuring provision that was made last year has fallen/been utilised by 10·2%. There is a risk of overstatement

if the provision is underutilised/not needed for the purpose for which it was established.

Finance lease liabilities

■ Although finance lease liabilities have increased (by $1m) there is a greater risk of understatement than overstatement

if leased assets are not recognised on the balance sheet (i.e. capitalised).

■ Disclosure risk arises if the requirements of IAS 17 ‘Leases’ (e.g. in respect of minimum lease payments) are not met.

Trade payables

■ These have increased by only 5·3% compared with the 17·8% increase in materials expense. There is a risk of

understatement as notifications (e.g. suppliers’ invoices) of liabilities outstanding at 30 June 2006 may have still to be

received (the month of June being an unexpired period).

Other (employee) liabilities

■ These may be understated as they have increased by only 7·5% although staff costs have increased by 14%. For

example, balances owing in respect of outstanding holiday entitlements at the year end may not yet be accurately

estimated.

Tutorial note: Credit will be given to other financial statements risks specific to the scenario. For example, ‘time-sensitive

delivery schedules’ might give rise to penalties or claims, that could result in understated provisions or undisclosed

contingent liabilities. Also, given that this is a new audit and the result has changed significantly (from loss to profit) might

suggest a risk of misstatement in the opening balances (and hence comparative information).

1 Tutorial note: This may be unlikely as other expenses have fallen also.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2019-07-19

- 2020-05-20

- 2020-05-08

- 2020-03-24

- 2020-05-17

- 2020-03-25

- 2020-05-17

- 2020-03-07

- 2020-05-20

- 2020-04-01

- 2020-03-01

- 2020-05-15

- 2020-04-23

- 2020-01-09

- 2020-04-29

- 2020-04-20

- 2020-01-09

- 2020-03-05

- 2020-02-19

- 2020-01-31

- 2019-12-28

- 2020-02-21

- 2020-01-09

- 2020-05-10

- 2020-01-01

- 2020-04-03

- 2020-01-31

- 2020-03-07

- 2020-05-09

- 2020-04-07