经验分享|备考ACCA考试四种必备心态

发布时间:2019-12-06

对于备考ACCA的考生朋友们,复习的安排应该劳逸结合,养成规律的生活习惯,每天安排一定的时间锻炼身体,放松自己,选择一些适合自己的运动方式,不仅可以愉悦身心,而且可以增强体质,有助于我们保持一个强劲的竞争优势积极迎考。要对自己的复习有信心,胜利属于有充分准备的人,不要给自己施加太大的压力。在考试期间要抛开一切杂念,考完一门后就不用去想其结果,而是调整心情考虑如何应对下一门,直到考试科目全部结束。如果能做到如此,坚持到最后,相信会得到一个满意的结果。接下来,51题库考试学习网就来给各位考生朋友们分享一下备考ACCA考试的四种必备心态!

一、恒定心

无论在备考中还是考试时遇到何种困难,一定要坚持下去。

二、吃苦心

不经历风雨怎么见彩虹,没有人能随随便便成功,既然选择了考试的道路,就要作好吃苦的准备,无论怎样辛苦,为了以后能更幸福的生活,一定要先吃苦,“吃得苦中苦方为人上人”,切记。

三、喜悦心

痛苦着去学习不如快乐着去学习,学习是快乐的、是愉悦的。请各位考生每天都要保持一颗愉快的心情,早上起来说的第一句话是“今天真是个好天气,我今天心情真好!”。

四、自信心

经常告诉自己我要成功,我一定会成功的!遇到难题的时候最好告诉自己我一定会把难题攻克的,我一定会战胜困难的。考生在考前复习阶段,往往会产生焦躁不安,心绪不宁,信心不足,担心忧虑等等不良的心理状况。所以请各位考生要不断的自我提示,“不计得失只讲过程,享受过程是快乐的”,考生不能总是患得患失,复习到最后了,考生的任务就是全力去考试,其它的事情与我无关,保持这样的良好心态一直到考试结束,就胜利了!

农民朋友常说“手中有粮,心里不慌”,各位考生朋友就应该是“胸有成竹,考试不慌”。所有的ACCA考试,大家都应该保持一种劳逸结合,放下包袱、轻松备考的心态来应战!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

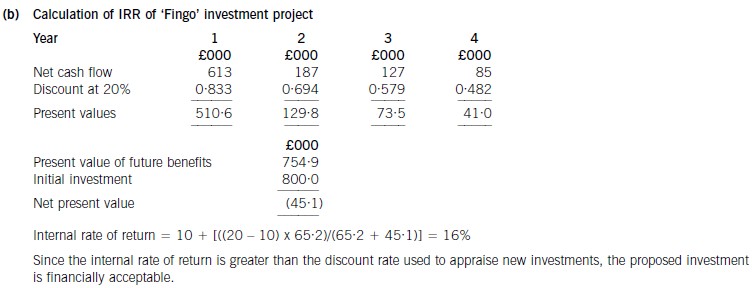

(b) Calculate the internal rate of return of the proposed investment and comment on your findings. (5 marks)

(c) With specific reference to Hugh Co, discuss the objective of a review engagement and contrast the level of

assurance provided with that provided in an audit of financial statements. (6 marks)

(c) The objective of a review engagement is to enable the auditor to obtain moderate assurance as to whether the financial

statements have been prepared in accordance with an identified financial reporting framework. This is defined in ISRE 2400

Engagements to Review Financial Statements.

In order to obtain this assurance, it is necessary to gather evidence using analytical procedures and enquiries with

management. Detailed substantive procedures will not be performed unless the auditor has reason to believe that the

information may be materially misstated.

The auditor should approach the engagement with a high degree of professional scepticism, looking for circumstances that

may cause the financial statements to be misstated. For example, in Hugh Co, the fact that the preparer of the financial

statements is part-qualified may lead the auditor to believe that there is a high inherent risk that the figures are misstated.

As a result of procedures performed, the auditor’s objective is to provide a clear written expression of negative assurance on

the financial statements. In a review engagement the auditor would state that ‘we are not aware of any material modifications

that should be made to the financial statements….’

This is normally referred to as an opinion of ‘negative assurance’.

Negative assurance means that the auditor has performed limited procedures and has concluded that the financial statements

appear reasonable. The user of the financial statements gains some comfort that the figures have been subject to review, but

only a moderate level of assurance is provided. The user may need to carry out additional procedures of their own if they

want to rely on the financial statements. For example, if Hugh Co were to use the financial statements as a means to raise

further bank finance, the bank would presumably perform, or require Hugh Co to perform, additional procedures to provide

a higher level of assurance as to the validity of the figures contained in the financial statements.

In comparison, in an audit, a high level of assurance is provided. The auditors provide an opinion of positive, but not absolute

assurance. The user is assured that the figures are free from material misstatement and that the auditor has based the opinion

on detailed procedures.

(c) Suggest ways in which each of the six problems chosen in (a) above may be overcome. (6 marks)

(c) Ways in which each of the problems might be overcome are as follows:

Meeting only the lowest targets

– To overcome the problem there must be some additional incentive. This could be through a change in the basis of bonus

payment which currently only provides an incentive to achieve the 100,000 tonnes of output.

Using more resources than necessary

– Overcoming the problem may require a change in the bonus system which currently does not provide benefit from any

output in excess of 100,000 tonnes. This may not be perceived as sufficiently focused in order to achieve action. It may

be that engendering a culture of continuous improvement would help ensure that employees actively sought ways of

reducing idle time levels.

Making the bonus – whatever it takes

– It is likely that efforts to change the ‘work ethos’ at all levels is required, while not necessarily removing the concept of

a bonus payable to all employees for achievement of targets. This may require the fostering of a culture for success within

the company. Dissemination of information to all staff relating to trends in performance, meeting targets, etc may help

to improve focus on continuous improvement.

Competing against other divisions, business units and departments

– The problem may need some input from the directors of TRG. For example, could a ‘dual-cost’ transfer pricing system

be explained to management at both the Bettamould division and also the Division with spare capacity in order to

overcome resistance to problems on transfer pricing and its impact on divisional budgets and reported results? In this

way it may be possible for the Bettamould division to source some of its input materials at a lower cost (particularly from

TRG’s viewpoint) and yet be acceptable to the management at the supplying division.

Ensuring that what is in the budget is spent

– In order to overcome the problem it may be necessary to educate management into acceptance of aspects of budgeting

such as the need to consider the committed, engineered and discretionary aspects of costs. For example, it may be

possible to reduce the number of salaried staff involved in the current quality checking of 25% of throughput on a daily

basis.

Providing inaccurate forecasts

– In order to overcome this problem there must be an integrated approach to the budget setting process. This may be

achieved to some extent through all aspects of the budget having to be agreed by all functions involved. For example,

engineers as well as production line management in reaching the agreed link between percentage process losses and

the falling efficiency of machinery due to age. In addition, TRC may insist an independent audit of aspects of budget

revisions by group staff.

Meeting the target but not beating it

– To overcome the problem may require that the bonus system should be altered to reflect any failure to control costs per

tonne at the budget level.

Avoiding risks

– In order to overcome such problems, TRC would have to provide some guarantees to Bettamould management that the

supply would be available during the budget period at the initially agreed price and that the quality would be maintained

at the required level. This would remove the risk element that the management of the Bettamould division may consider

currently exists.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-10

- 2020-05-06

- 2020-01-10

- 2020-01-10

- 2020-01-14

- 2020-04-14

- 2020-01-10

- 2020-01-09

- 2020-03-08

- 2019-11-27

- 2021-05-08

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-04-15

- 2021-06-19

- 2020-09-03

- 2020-01-10

- 2020-01-31

- 2020-01-29

- 2021-05-08

- 2020-04-14

- 2020-02-02

- 2020-04-17

- 2020-01-10

- 2020-03-07

- 2020-01-10

- 2020-05-14

- 2020-01-09

- 2020-05-09