ACCA和USCPA怎么选择,一起来看看本篇文章吧!

发布时间:2020-04-24

ACCA和USCPA怎么选择?ACCA和USCPA的区别有哪些?今天就跟随51题库考试学习网一起来看看吧。

ACCA和USCPA的区别有哪些

1科目不同:ACCA考试科目一共有14门,即使本科生免试5门,也要考9门。USCPA只考4门,分为财务会计及报告、法规、商业环境及理论和审计。

2周期不同:由于ACCA科目较多,因此通过的周期较长,最长可达10年。USCPA采用计算机考试,每年有4个Windows,每个Window为2个月,通常4-6个月可以通过4门的考试拿到资格。

3适用范围不同:ACCA适用于UK GAAP和国际会计准则,USCPA适用于US GAAP。

那么acca和uscpa究竟应该怎么选?

USCPA考试有学分要求,考试周期短易通过:更适合留学生和上班族,还可以免考ACCA八门。

从报考要求来看,USCPA对学历和学分都有要求,必须是已经获得或即将取得学士学位,且需要修满150个学分(个别州:缅因州、加州等除外),所以大学的时候可以先学起来;

而从考试周期来看,USCPA显然就轻松多了,共计4门科目,且除了3、6、9、12月及节假日均可预约报考。采用计算机考试,最快4-6个月就可以通过4门的考试。美国的留学生更无需多言,为了就业考出USCPA几乎成为商科生的“标配”。

从职业发展角度来说,美国是世界上最大的经济体,相应的财务要求最高,USCPA是美国的注册会计师,GAAP准则一直引领者国际会计的发展趋势,且具备全球签字权。美资公司在世界分布广泛,因此USCPA在国际认可度高,全球就业之广,在世界各地享有与众不同的威望,收入也高。对移民和留学北美、欧洲、澳洲都是最佳的加分证照。USCPA持证人一般从事内部审计师、法规遵从经理、财务分析师、外部审计师等,对职场人士来说,是升职加薪的必备执照。

ACCA考试门槛较低,无特殊要求,考试周期长,更适合时间充裕的大学生。

ACCA和USCPA一样,都是全英文考试。ACCA大学即可报考,在毕业时通过全科,在应届毕业生中,薪资很有竞争力。

但是ACCA共有14门考试科目,分为两个部分,第一部分为基础阶段,共9门,主要涉及财务会计和管理会计方面的核心知识;第二部分为专业阶段,共4门,引入了作为未来的高级会计师所必须的更高级的职业技能和知识技能,相当于硕士阶段的课程难度。科目之多也直接导致了整个考试战线的相对拉长。尽管可以早早报名,ACCA也并非那么容易拿下的。

USCPA和ACCA,这两个证书对于财务人来说,都有不错的辅助作用。鉴于商业和会计业务渐渐全球化的趋势,具备一个国际化的财务证书,对于年轻财会人才在职业方面的发展和提升,具有极其关键的重要性。

获得美国注册会计师资质,能够极大地提升个人价值,不论在美国或国际的会计师事务所、本土或海外的美国公司。身为美国注册会计师,即代表着自身对自己国家和美国财务领域的了解与熟练。加上它广泛应用和签字权,自然能够为财务人的职业发展,创造更多的机遇,带来更大的优势。

愉快的时光总是很短暂,以上就是今天51题库考试学习网为大家分享的全部内容,如有其他疑问请继续关注51题库考试学习网!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(ii) consignment inventory; and (3 marks)

(ii) Consignment inventory

■ Agree terms of sale to dealers to confirm the ‘principal – agent’ relationship between Pavia and dealers.

■ Inspect proforma invoices for vehicles sent on consignment to dealers to confirm number of vehicles with dealers

at the year end.

■ Obtain direct confirmation from dealers of vehicles unsold at the year end.

■ Physically inspect vehicles sold on consignment before the year end that are returned unsold by dealers after the

year end (if any) for evidence of impairment.

■ Perform. cutoff tests on sales to dealers/trade receivables/vehicle inventory.

■ If goods on consignment are treated as inventory agree their unit costs to be the same as for other vehicles in

inventory.

(c) insider dealing. (5 marks)

(c) Insider dealing

Explanation of term

Insider dealing means using ‘inside information’ (i.e. price-sensitive information relating to the issuer of securities) to gain

advantage when ‘dealing’ (i.e. acquiring or disposing) in securities.

Ethical risks

Insider dealing is a potential area of conflict and contention for accountants in industry and commerce (i.e. employed

professional accountants) in particular (because of their exposure to price-sensitive information).

Acts of insider dealing contravene the fundamental principles of integrity and confidentiality:

■ integrity – a professional accountant should be honest;

■ confidentiality – a professional accountant should respect the confidentiality of information acquired during the course

of performing professional services and should not use or disclose it without proper and specific authority.

Professional accountants in public practice who become privy to price-sensitive information will similarly be in breach of their

duties of integrity and confidentiality if they get involved in insider dealing. Also, the reputation of individual practitioners and

their firms may be put at risk by allegations of insider dealing even though they have no involvement with the practice. For

example, if an auditor does not detect when an entity’s management is involved in insider dealing.

Sufficiency of current ethical guidance

Relevant current ethical guidance, that is covered by the principles of integrity and confidentiality, is sufficient to explain the

ethical risks of insider dealing but cannot prevent its practice. Even where there are laws to prosecute insider dealing,

penalties (such as seven years in jail and/or unlimited fines) have been ineffective in combating insider dealing.

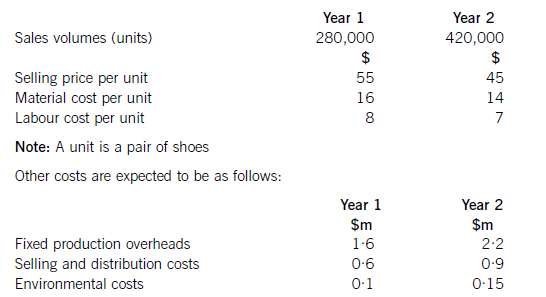

Shoe Co, a shoe manufacturer, has developed a new product called the ‘Smart Shoe’ for children, which has a built-in tracking device. The shoes are expected to have a life cycle of two years, at which point Shoe Co hopes to introduce a new type of Smart Shoe with even more advanced technology. Shoe Co plans to use life cycle costing to work out the total production cost of the Smart Shoe and the total estimated profit for the two-year period.

Shoe Co has spent $5·6m developing the Smart Shoe. The time spent on this development meant that the company missed out on the opportunity of earning an estimated $800,000 contribution from the sale of another product.

The company has applied for and been granted a ten-year patent for the technology, although it must be renewed each year at a cost of $200,000. The costs of the patent application were $500,000, which included $20,000 for the salary costs of Shoe Co’s lawyer, who is a permanent employee of the company and was responsible for preparing the application.

The following information is also available for the next two years:

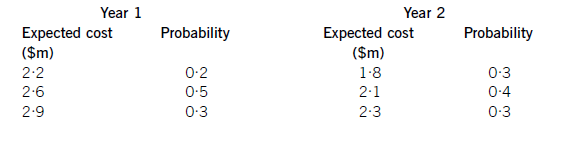

Shoe Co is still negotiating with marketing companies with regard to its advertising campaign, so is uncertain as to what the total marketing costs will be each year. However, the following information is available as regards the probabilities of the range of costs which are likely to be incurred:

Required:

Applying the principles of life cycle costing, calculate the total expected profit for Shoe Co for the two-year period.

(10 marks)

Totalsalesrevenue=(280,000x$55)+(420,000x$45)=$15·4m+18·9m=$34·3m.NoteTheexpectedprofithasbeencalculatedusinglifecyclecostingnotrelevantcosting.Hence,the$20,000salarycostincludedinpatentcostsshouldbeincludedinthelifecyclecost.Similarly,theopportunitycostof$800,000isnotincludedusinglifecyclecostingwhereasifrelevantcostingwasbeingusedtodecideonaparticularcourseofaction,theopportunitycostwouldbeincluded.Working1Expectedmarketingcostinyear1:(0·2x$2·2m)+(0·5x$2·6m)+(0·3x$2·9m)=$2·61mExpectedmarketingcostyear2:(0·3x$1·8m)+(0·4x$2·1m)+(0·3x$2·3m)=$2·07mTotalexpectedmarketingcost=$4·68m

(b) Describe five major barriers to good communication. (10 marks)

Part (b):

Barriers to communication include the personal background of the people communicating, including language differences between

staff, management and customers. The use of jargon, especially by professional and technical staff, differences in education levels

can be a substantial barrier throughout the organisation. Communication ‘noise’ is a barrier not always recognised. This is where

the message is confused by extraneous matters not relevant to that particular communication. Different levels of education and

experience can lead to different perception of individuals, leading to conflict within the organisation, between individuals and

between departments. Similarly, another barrier often not recognised is communication overload; too much information being

communicated at one time leading to confusion. Distances involved and the subsequent use of different communication facilities

is a barrier, leading to misunderstandings based on problems noted above. Finally, and perhaps most importantly, distortion of the

information transmitted.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2019-07-20

- 2020-01-10

- 2020-04-30

- 2020-04-18

- 2020-03-13

- 2020-05-06

- 2020-01-10

- 2020-03-13

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-05-14

- 2020-01-31

- 2019-11-27

- 2020-03-07

- 2020-05-14

- 2020-04-16

- 2020-05-15

- 2020-01-10

- 2020-05-21

- 2020-02-01

- 2020-01-10

- 2020-03-11

- 2020-01-29

- 2020-01-09

- 2020-04-23

- 2020-02-20

- 2019-07-20

- 2020-03-07

- 2020-04-28