ACCA证书零基础可以考吗?

发布时间:2021-10-21

众所周知ACCA证书的含金量很高,每年越来越多的同学都纷沓而至报考学习ACCA,那么零基础的同学是否可以学习呢?今天51题库考试学习网就带大家一起来看看!

ACCA考试零基础也可以学习,ACCA本身的课程设置就是由浅入深,F1-F3都是财会方面的基础知识。

学习建议

零基础学生党:建议工作日早上学习2小时,以讲师授课为主,记笔记为辅;晚上学习3小时,以知识点梳理为主,做题练习为辅。周末学习6小时,以整理错题,巩固复习为主。

零基础上班族:建议工作日下班后学习2小时,以讲师授课为主,结合工作实际流程记忆知识点。周末学习6小时,以做题练习为主,在题目中复习巩固知识点。

学习方法

一、学习知识点(建议5周)

理解记忆知识点

充分利用学习资料,例如讲义、教材、练习册等,系统学习面授课程,理解知识要点并认真梳理。如果您在学习中遇到任何关于知识点和练习册的疑问,都可以咨询专业老师,问题别攒着。

勤练习,多思考

通过讲师提炼的重难点练习题,把生活场景融入到对题目的理解上,进一步加深对知识点的理解和记忆,在实际题目中掌握答题规律。

二、考前冲刺(3周)

罗列复习纲要,对知识点进行复述式记忆

在整理复习的过程中,记录讲师提到的重要知识点,在复习时进行自查。在整理错题的时候,在对应重要知识点前记录问号,发现薄弱知识点,进行答疑或再次梳理,以便对知识点有整体把握。根据冲刺串讲课程,复习精要知识点,力求在老师的指导下,复述相关概念。

整理错题

整理第一阶段的错题,寻找教材中对应的知识点内容,巧妙地运用知识理解题意,加深印象。

三、模拟考试(1周)

制定备考计划

包括各科特点,梳理备考要点,考试题型分析,相关考官文章的重点解析等。

严格控制时间

利用2小时时间,对官方样卷和模拟题进行仿真训练。一个考点无法解答时,可以先选择一个备选项,做好标记,在题目全部答完还有剩余时间的情况下,复查题目。

相信大家对备考ACCA的方法都有了基本了解,零基础的同学只要肯花时间学习,都是可以考过的,今天分享就到这里了,更多ACCA相关资讯,敬请关注51题库考试学习网!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(c) Lamont owns a residential apartment above its head office. Until 31 December 2006 it was let for $3,000 a

month. Since 1 January 2007 it has been occupied rent-free by the senior sales executive. (6 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Lamont Co for the year ended

31 March 2007.

NOTE: The mark allocation is shown against each of the three issues.

(c) Rent-free accommodation

(i) Matters

■ The senior sales executive is a member of Lamont’s key management personnel and is therefore a related party.

■ The occupation of Lamont’s residential apartment by the senior sales executive is therefore a related party

transaction, even though no price is charged (IAS 24 Related Party Disclosures).

■ Related party transactions are material by nature and information about them should be disclosed so that users of

financial statements understand the potential effect of related party relationships on the financial statements.

■ The provision of ‘housing’ is a non-monetary benefit that should be included in the disclosure of key management

personnel compensation (within the category of short-term employee benefits).

■ The financial statements for the year ended 31 March 2007 should disclose the arrangement for providing the

senior sales executive with rent-free accommodation and its fair value (i.e. $3,000 per month).

Tutorial note: Since no price is charged for the transaction, rote-learned disclosures such as ‘the amount of outstanding

balances’ and ‘expense recognised in respect of bad debts’ are irrelevant.

(ii) Audit evidence

■ Physical inspection of the apartment to confirm that it is occupied.

■ Written representation from the senior sales executive that he is occupying the apartment free of charge.

■ Written representation from the management board confirming that there are no related party transactions requiring

disclosure other than those that have been disclosed.

■ Inspection of the lease agreement with (or payments received from) the previous tenant to confirm the $3,000

monthly rental value.

14 Alpha buys goods from Beta. At 30 June 2005 Beta’s account in Alpha’s records showed $5,700 owing to Beta.

Beta submitted a statement to Alpha as at the same date showing a balance due of $5,200.

Which of the following could account fully for the difference?

A Alpha has sent a cheque to Beta for $500 which has not yet been received by Beta.

B The credit side of Beta’s account in Alpha’s records has been undercast by $500.

C An invoice for $250 from Beta has been treated in Alpha’s records as if it had been a credit note.

D Beta has issued a credit note for $500 to Alpha which Alpha has not yet received.

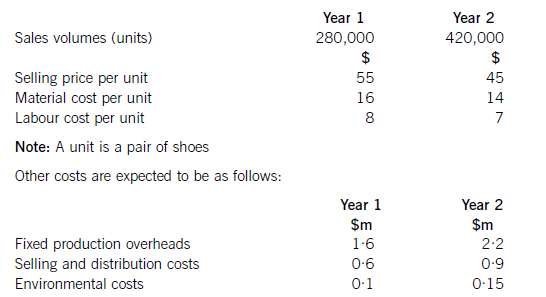

Shoe Co, a shoe manufacturer, has developed a new product called the ‘Smart Shoe’ for children, which has a built-in tracking device. The shoes are expected to have a life cycle of two years, at which point Shoe Co hopes to introduce a new type of Smart Shoe with even more advanced technology. Shoe Co plans to use life cycle costing to work out the total production cost of the Smart Shoe and the total estimated profit for the two-year period.

Shoe Co has spent $5·6m developing the Smart Shoe. The time spent on this development meant that the company missed out on the opportunity of earning an estimated $800,000 contribution from the sale of another product.

The company has applied for and been granted a ten-year patent for the technology, although it must be renewed each year at a cost of $200,000. The costs of the patent application were $500,000, which included $20,000 for the salary costs of Shoe Co’s lawyer, who is a permanent employee of the company and was responsible for preparing the application.

The following information is also available for the next two years:

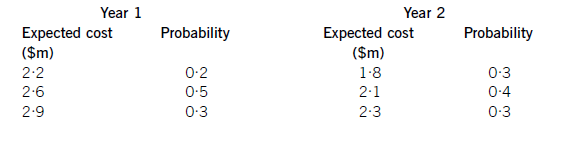

Shoe Co is still negotiating with marketing companies with regard to its advertising campaign, so is uncertain as to what the total marketing costs will be each year. However, the following information is available as regards the probabilities of the range of costs which are likely to be incurred:

Required:

Applying the principles of life cycle costing, calculate the total expected profit for Shoe Co for the two-year period.

(10 marks)

Totalsalesrevenue=(280,000x$55)+(420,000x$45)=$15·4m+18·9m=$34·3m.NoteTheexpectedprofithasbeencalculatedusinglifecyclecostingnotrelevantcosting.Hence,the$20,000salarycostincludedinpatentcostsshouldbeincludedinthelifecyclecost.Similarly,theopportunitycostof$800,000isnotincludedusinglifecyclecostingwhereasifrelevantcostingwasbeingusedtodecideonaparticularcourseofaction,theopportunitycostwouldbeincluded.Working1Expectedmarketingcostinyear1:(0·2x$2·2m)+(0·5x$2·6m)+(0·3x$2·9m)=$2·61mExpectedmarketingcostyear2:(0·3x$1·8m)+(0·4x$2·1m)+(0·3x$2·3m)=$2·07mTotalexpectedmarketingcost=$4·68m

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-10

- 2020-04-07

- 2019-12-28

- 2020-04-25

- 2020-01-10

- 2021-10-02

- 2019-04-11

- 2020-02-05

- 2020-09-03

- 2020-01-01

- 2020-03-31

- 2020-03-27

- 2020-04-20

- 2020-01-05

- 2021-10-07

- 2020-05-19

- 2020-01-10

- 2020-03-11

- 2020-05-13

- 2020-01-10

- 2020-01-15

- 2021-10-17

- 2020-04-12

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-03-07

- 2021-02-14

- 2020-01-10

- 2020-03-19