ACCA F1知识点:企业组织及企业组织结构和规划

发布时间:2021-02-13

想了解ACCA考试常见考点的考生赶紧和51题库考试学习网一起去了解下ACCA考试F1常见考点吧!

acca F1知识点:企业组织及企业组织结构和规划

正式及非正式企业组织

(a)解释非正式组织及其与正式组织的关系

非正式组织的存在 P122

(b)描述非正式组织对企业的影响

企业组织结构和规划

(a)描述组织被地理区域和产品结构化的不同方式:企业家型、功能型、矩阵型、事业部制型、部门型 P124

(b)解释基本组织结构的概念:执行与管理的分离、控制范围和权利链、高大而扁平的组织

(c)解释战略层、战术层、操作层在Anthony hierarchy组织中的特点

(d)解释中央集权制和非集权制及罗列他们的优点和缺点

以上就是51题库考试学习网带给大家的全部内容,希望能够帮到大家!预祝大家在ACCA考试中取得满意的成绩,如果想要了解更多关于ACCA考试的资讯,敬请关注51题库考试学习网!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(d) Draft a letter for Tim Blake to send to WM’s investors to include the following:

(i) why you believe robust internal controls to be important; and

(ii) proposals on how internal systems might be improved in the light of the overestimation of mallerite at

WM.

Note: four professional marks are available within the marks allocated to requirement (d) for the structure,

content, style. and layout of the letter.

(16 marks)

You will be aware of the importance of accurate resource valuation to Worldwide Minerals (WM). Unfortunately, I have to

inform. you that the reserve of mallerite, one of our key minerals in a new area of exploration, was found to have been

overestimated after the purchase of a mine. It has been suggested that this information may have an effect on shareholder

value and so I thought it appropriate to write to inform. you of how the board intends to respond to the situation.

In particular, I would like to address two issues. It has been suggested that the overestimation arose because of issues with

the internal control systems at WM. I would firstly like to reassure you of the importance that your board places on sound

internal control systems and then I would like to highlight improvements to internal controls that we shall be implementing

to ensure that the problem should not recur.

(i) Importance of internal control

Internal control systems are essential in all public companies and Worldwide Minerals (WM) is no exception. If anything,

WM’s strategic position makes internal control even more important, operating as it does in many international situations

and dealing with minerals that must be guaranteed in terms of volume, grade and quality. Accordingly, your board

recognises that internal control underpins investor confidence. Investors have traditionally trusted WM’s management

because they have assumed it capable of managing its internal operations. This has, specifically, meant becoming aware

of and controlling known risks. Risks would not be known about and managed without adequate internal control

systems. Internal control, furthermore, helps to manage quality throughout the organisation and it provides

management with information on internal operations and compliance. These features are important in ensuring quality

at all stages in the WM value chain from the extraction of minerals to the delivery of product to our customers. Linked

to this is the importance of internal control in helping to expose and improve underperforming internal operations.

Finally, internal control systems are essential in providing information for internal and external reporting upon which, in

turn, investor confidence rests.

(ii) Proposals to improve internal systems at WM

As you may be aware, mineral estimation and measurement can be problematic, particularly in some regions. Indeed,

there are several factors that can lead to under or overestimation of reserves valuations as a result of geological survey

techniques and regional cultural/social factors. In the case of mallerite, however, the issues that have been brought to

the board’s attention are matters of internal control and it is to these that I would now like to turn.

In first instance, it is clear from the fact that the overestimate was made that we will need to audit geological reports at

an appropriate (and probably lower) level in the organisation in future.

Once a claim has been made about a given mineral resource level, especially one upon which investor returns might

depend, appropriate systems will be instituted to ask for and obtain evidence that such reserves have been correctly and

accurately quantified.

We will recognise that single and verbal source reports of reserve quantities may not necessarily be accurate. This was

one of the apparent causes of the overestimation of mallerite. A system of auditing actual reserves rather than relying

on verbal evidence will rectify this.

The purchase of any going concern business, such as the mallerite mine, is subject to due diligence. WM will be

examining its procedures in this area to ensure that they are fit for purpose in the way that they may not have been in

respect of the purchase of the mallerite mine. I will be taking all appropriate steps to ensure that all of these internal

control issues can be addressed in future.

Thank you for your continued support of Worldwide Minerals and I hope the foregoing goes some way to reassure you

that the company places the highest value on its investors and their loyalty.

Yours faithfully,

Tim Blake

Chairman

(ii) Can we entertain our clients as a gesture of goodwill or is corporate hospitality ruled out? (3 marks)

Required:

For EACH of the three FAQs, explain the threats to objectivity that may arise and the safeguards that should

be available to manage them to an acceptable level.

NOTE: The mark allocation is shown against each of the three questions.

(ii) Corporate hospitality

A partner in an audit firm is obviously in a position to influence the conduct and outcome of an audit. Therefore a

partner being on ‘too friendly’ terms with an audit client creates a familiarity threat. Other members of the audit team

may not exert as much influence on the audit.

A self-interest threat may also be perceived (e.g. if corporate hospitality is provided to keep a prestigious client).

There is no absolute prohibition against corporate hospitality provided:

■ the value attached to such hospitality is ‘insignificant’; and

■ the ‘frequency, nature and cost’ of the hospitality is reasonable.

Thus, flying the directors of an audit client for weekends away could be seen as significant. Similarly, entertaining an

audit client on a regular basis could be seen as unacceptable.

Partners and staff of Boleyn will need to be objective in their assessments of the significance or reasonableness of the

hospitality offered. (Would ‘a reasonable and informed third party’ conclude that the hospitality will or is likely to be

seen to impair your objectivity?)

If they have any doubts they should discuss the matter in the first instance with the audit engagement partner, who

should refer the matter to the ethics partner if in doubt.

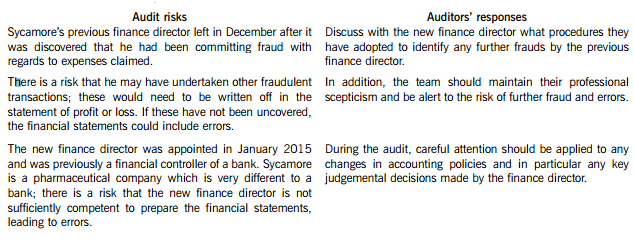

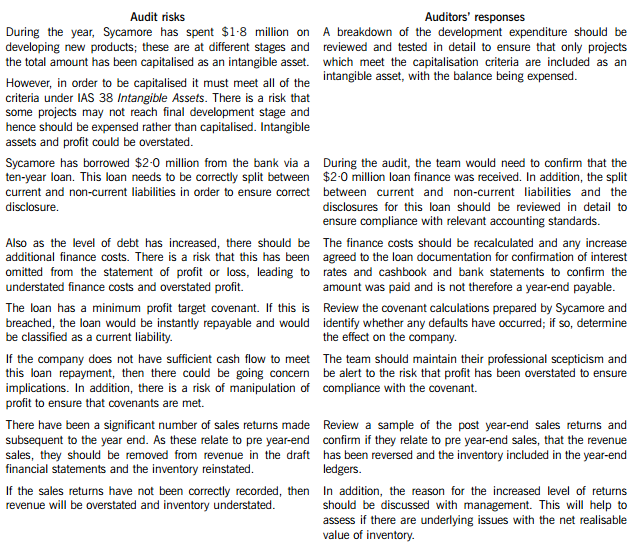

You are the audit supervisor of Maple & Co and are currently planning the audit of an existing client, Sycamore Science Co (Sycamore), whose year end was 30 April 2015. Sycamore is a pharmaceutical company, which manufactures and supplies a wide range of medical supplies. The draft financial statements show revenue of $35·6 million and profit before tax of $5·9 million.

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

(a) Fraud responsibility

Maple & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error.

In order to fulfil this responsibility, Maple & Co is required to identify and assess the risks of material misstatement of the financial statements due to fraud.

They need to obtain sufficient appropriate audit evidence regarding the assessed risks of material misstatement due to fraud, through designing and implementing appropriate responses. In addition, Maple & Co must respond appropriately to fraud or suspected fraud identified during the audit.

When obtaining reasonable assurance, Maple & Co is responsible for maintaining professional scepticism throughout the audit, considering the potential for management override of controls and recognising the fact that audit procedures which are effective in detecting error may not be effective in detecting fraud.

To ensure that the whole engagement team is aware of the risks and responsibilities for fraud and error, ISAs require that a discussion is held within the team. For members not present at the meeting, Sycamore’s audit engagement partner should determine which matters are to be communicated to them.

(b) Audit risks and auditors’ responses

(c) (i) Review engagements

Review engagements are often undertaken as an alternative to an audit, and involve a practitioner reviewing financial data, such as six-monthly figures. This would involve the practitioner undertaking procedures to state whether anything has come to their attention which causes the practitioner to believe that the financial data is not in accordance with the financial reporting framework.

A review engagement differs to an external audit in that the procedures undertaken are not nearly as comprehensive as those in an audit, with procedures such as analytical review and enquiry used extensively. In addition, the practitioner does not need to comply with ISAs as these only relate to external audits.

(ii) Levels of assurance

The level of assurance provided by audit and review engagements is as follows:

External audit – A high but not absolute level of assurance is provided, this is known as reasonable assurance. This provides comfort that the financial statements present fairly in all material respects (or are true and fair) and are free of material misstatements.

Review engagements – where an opinion is being provided, the practitioner gathers sufficient evidence to be satisfied that the subject matter is plausible; in this case negative assurance is given whereby the practitioner confirms that nothing has come to their attention which indicates that the subject matter contains material misstatements.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2019-03-17

- 2019-07-03

- 2021-02-13

- 2020-10-12

- 2021-02-14

- 2020-10-12

- 2021-02-13

- 2020-10-12

- 2021-02-14

- 2021-02-13

- 2021-02-13

- 2021-02-13

- 2021-02-13

- 2020-10-12

- 2020-09-05

- 2020-10-12

- 2020-10-12

- 2020-10-12

- 2021-02-13

- 2020-10-12

- 2020-10-12

- 2021-02-13

- 2020-09-05

- 2021-02-13

- 2021-02-13

- 2019-03-17

- 2020-09-05

- 2020-10-12

- 2020-10-12

- 2020-10-12