ACCA考试F7考试模拟试题(2020-08-19)

发布时间:2020-08-19

备考ACCA考试,好的学习方法很重要,但是练习也很重要,下面51题库考试学习网就给大家分享一些,ACCA考试F7考试模拟试题,备考的小伙伴赶紧来练练手吧。

1. Consolidated

financial statements are presented on the basis that the companies within the

group are treated as if they are a single (economic) entity.

Which of the following are requirements of

preparing group accounts?

(i) All subsidiaries must adopt the

accounting policies of the parent

(ii) Subsidiaries with activities which are

substantially different to the activities of other members of the group should

not be consolidated

(iii) All entity financial statements

within a group should (normally) be prepared to the same accounting year end

prior to consolidation

(iv) Unrealised profits within the group

must be eliminated from the consolidated financial statements

A All four

B (i) and (ii) only

C (i), (iii) and (iv)

D (iii) and (iv)

答案:C

2. Dempsey’s year

end is 30 September 2014. Dempsey commenced the development stage of a project

to produce a new pharmaceutical drug on 1 January 2014. Expenditure of $40,000

per month was incurred until the project was completed on 30 June 2014 when the

drug went into immediate production. The directors became confident of the

project’s success on 1 March 2014. The drug has an estimated life span of five

years; time apportionment is used by Dempsey where applicable. What amount will

Dempsey charge to profit or loss for development costs, including any

amortisation, for the year ended 30 September 2014?

A $12,000

B $98,667

C $48,000

D $88,000

答案:C

3. On 1 October

2013, Fresco acquired an item of plant under a five-year finance lease

agreement. The plant had a cash purchase cost of $25 million. The agreement had

an implicit finance cost of 10% per annum and required an immediate deposit of

$2 million and annual rentals of $6 million paid on 30 September each year for

five years. What would be the current liability for the leased plant in

Fresco’s statement of financial position as at 30 September 2014?

A $19,300,000

B $4,070,000

C $5,000,000

D $3,850,000

答案:C

4. The following

information has been taken or calculated from Fowler’s financial statements for

the year ended 30 September 2014.Fowler’s cash cycle at 30 September 2014 is 70

days.Its inventory turnover is six times. Year-end trade payables are $230,000.

Purchases on credit for the year were $2 million. Cost of sales for the year

was $1·8 million. What is Fowler’s trade receivables collection period as at 30

September 2014?

All calculations should be made to the

nearest full day. The trading year is 365 days.

A 106 days

B 89 days

C 56 days

D 51 days

答案:B

5. Which of the

following items should be capitalised within the initial carrying amount of an

item of plant?

(i) Cost of transporting the plant to the

factory

(ii) Cost of installing a new power supply

required to operate the plant

(iii) A deduction to reflect the estimated

realisable value

(iv) Cost of a three-year maintenance

agreement

(v) Cost of a three-week training course

for staff to operate the plant

A (i) and (ii) only

B (i), (ii) and (iii)

C (ii), (iii) and (iv)

D (i), (iv) and (v)

答案:A

以上是本次51题库考试学习网分享给大家的ACCA考试试题,备考的小伙伴抓紧时间练习一下吧。欲了解更多关于ACCA考试的试题,敬请关注51题库考试学习网!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(iii) cheese. (4 marks)

(iii) Cheese

■ Examine the terms of sales to Abingdon Bank – confirm the bank’s legal title (e.g. if GVF were to cease to trade

and so could not exercise buy-back option).

■ Obtain a direct confirmation from the bank of the cost of inventory sold by GVF to Abingdon Bank and the amount

re-purchased as at 30 September 2005 (the net amount being the outstanding loan).

■ Inspect the cheese as at 30 September 2005 (e.g. during the physical inventory count) paying particular attention

to the factors which indicate the age (and strength) of the cheese (e.g. its location or physical appearance).

■ Observe how the cheese is stored – if on steel shelves discuss with GVF’s management whether its net realisable

value has been reduced below cost.

■ Test check, on a sample basis, the costing records supporting the cost of batches of cheese.

■ Confirm that the cost of inventory sold to the bank is included in inventory as at 30 September 2005 and the

nature of the bank security adequately disclosed.

■ Agree the repurchase of cheese which has reached maturity at cost plus 7% per six months to purchase invoices

(or equivalent contracts) and cash book payments.

■ Test check GVF’s inventory-ageing records to production records. Confirm the carrying amount of inventory as at

30 September 2005 that will not be sold until after 30 September 2006, and agree to the amount disclosed in

the notes to inventory as a ‘non-current’ portion.

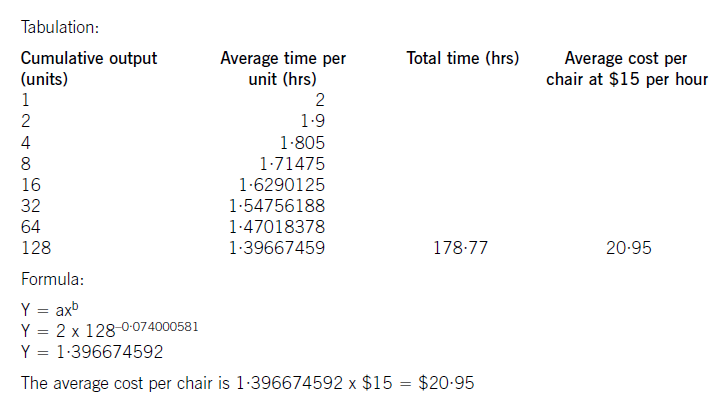

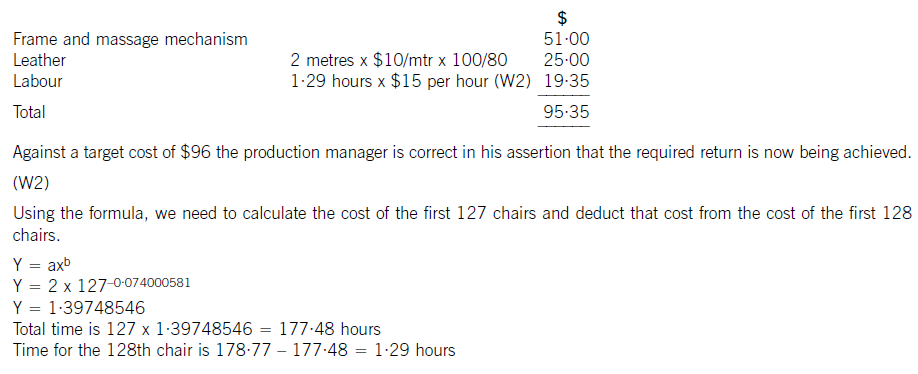

Big Cheese Chairs (BCC) manufactures and sells executive leather chairs. They are considering a new design of massaging chair to launch into the competitive market in which they operate.

They have carried out an investigation in the market and using a target costing system have targeted a competitive selling price of $120 for the chair. BCC wants a margin on selling price of 20% (ignoring any overheads).

The frame. and massage mechanism will be bought in for $51 per chair and BCC will upholster it in leather and assemble it ready for despatch.

Leather costs $10 per metre and two metres are needed for a complete chair although 20% of all leather is wasted in the upholstery process.

The upholstery and assembly process will be subject to a learning effect as the workers get used to the new design.

BCC estimates that the first chair will take two hours to prepare but this will be subject to a learning rate (LR) of 95%.

The learning improvement will stop once 128 chairs have been made and the time for the 128th chair will be the time for all subsequent chairs. The cost of labour is $15 per hour.

The learning formula is shown on the formula sheet and at the 95% learning rate the value of b is -0·074000581.

Required:

(a) Calculate the average cost for the first 128 chairs made and identify any cost gap that may be present at

that stage. (8 marks)

(b) Assuming that a cost gap for the chair exists suggest four ways in which it could be closed. (6 marks)

The production manager denies any claims that a cost gap exists and has stated that the cost of the 128th chair will be low enough to yield the required margin.

(c) Calculate the cost of the 128th chair made and state whether the target cost is being achieved on the 128th chair. (6 marks)

(W1)

The cost of the labour can be calculated using learning curve principles. The formula can be used or a tabular approach would

also give the average cost of 128 chairs. Both methods are acceptable and shown here.

(b) To reduce the cost gap various methods are possible (only four are needed for full marks)

– Re-design the chair to remove unnecessary features and hence cost

– Negotiate with the frame. supplier for a better cost. This may be easier as the volume of sales improve as suppliers often

are willing to give discounts for bulk buying. Alternatively a different frame. supplier could be found that offers a better

price. Care would be needed here to maintain the required quality

– Leather can be bought from different suppliers or at a better price also. Reducing the level of waste would save on cost.

Even a small reduction in waste rates would remove much of the cost gap that exists

– Improve the rate of learning by better training and supervision

– Employ cheaper labour by reducing the skill level expected. Care would also be needed here not to sacrifice quality or

push up waste rates.

(c) The cost of the 128th chair will be:

(b) Explain THREE problems in undertaking a performance comparison of GBC and TTC and also explain THREE

items of additional information that would be of assistance in assessing the operating and financial

performance of GBC and TTC. (6 marks)

(b) The relative performance of GBC and TTC is difficult to assess due to the following:

(i) They would appear to have differing objectives. GBC provides free transport for senior citizens and charges lower fares

than TTC. GBC also uses environmentally friendly fuel. Each of these factors inhibits a direct comparison of the two

organisations.

(ii) The organisations are funded differently. It is evident that TTC uses loan finance to fund operations which gives rise to

interest charges which are not incurred by GBC. On the other hand GBC is funded by the government.

(iii) TTC has higher fixed asset values which precipitate much higher depreciation charges.

(iv) There is also a lack of non-financial performance indicators such as the number of on-time arrivals, number of accidents,

complaints re passenger dissatisfaction, staff turnover, adherence to relevant legislation, convenience of pick-up/drop-off

points etc.

The following items of additional information would assist in assessing the financial and operating performance of the two

companies:

(1) The number of staff employed by each organisation would assist in the assessment of the financial and operating

performance. Ratios such as revenue generated per employee and operating costs per employee might provide useful

comparators of financial and operating efficiency.

(2) Safety and accident records of each organisation would give an indication of the reliability and safety afforded to

passengers by each organisation. Passenger safety is of paramount importance to all passenger transport businesses.

(3) Records of late/cancelled buses together with the number of complaints received from the passengers would provide an

indication of the efficiency of the service provided by each organisation.

(4) The accessibility of the services, location of pick-up/drop-off points would provide an indication of the flexibility of service

delivery provided by each organisation.

(5) The comfort, cleanliness and age of the respective bus fleets would provide a further indication of the level of service

quality provided by each organisation.

(6) The fuel emission levels of the buses operated by each organisation would provide an indication of the extent of their

‘social responsibility’.

Notes: (i) Only three items of additional information were required.

(ii) Alternative relevant discussion and examples would be acceptable.

(a) Contrast the role of internal and external auditors. (8 marks)

(b) Conoy Co designs and manufactures luxury motor vehicles. The company employs 2,500 staff and consistently makes a net profit of between 10% and 15% of sales. Conoy Co is not listed; its shares are held by 15 individuals, most of them from the same family. The maximum shareholding is 15% of the share capital.

The executive directors are drawn mainly from the shareholders. There are no non-executive directors because the company legislation in Conoy Co’s jurisdiction does not require any. The executive directors are very successful in running Conoy Co, partly from their training in production and management techniques, and partly from their ‘hands-on’ approach providing motivation to employees.

The board are considering a significant expansion of the company. However, the company’s bankers are

concerned with the standard of financial reporting as the financial director (FD) has recently left Conoy Co. The board are delaying provision of additional financial information until a new FD is appointed.

Conoy Co does have an internal audit department, although the chief internal auditor frequently comments that the board of Conoy Co do not understand his reports or provide sufficient support for his department or the internal control systems within Conoy Co. The board of Conoy Co concur with this view. Anders & Co, the external auditors have also expressed concern in this area and the fact that the internal audit department focuses work on control systems, not financial reporting. Anders & Co are appointed by and report to the board of Conoy Co.

The board of Conoy Co are considering a proposal from the chief internal auditor to establish an audit committee.

The committee would consist of one executive director, the chief internal auditor as well as three new appointees.

One appointee would have a non-executive seat on the board of directors.

Required:

Discuss the benefits to Conoy Co of forming an audit committee. (12 marks)

(a)Roleofinternalandexternalauditors–differencesObjectivesThemainobjectiveofinternalauditistoimproveacompany’soperations,primarilyintermsofvalidatingtheefficiencyandeffectivenessoftheinternalcontrolsystemsofacompany.Themainobjectiveoftheexternalauditoristoexpressanopiniononthetruthandfairnessofthefinancialstatements,andotherjurisdictionspecificrequirementssuchasconfirmingthatthefinancialstatementscomplywiththereportingrequirementsincludedinlegislation.ReportingInternalauditreportsarenormallyaddressedtotheboardofdirectors,orotherpeoplechargedwithgovernancesuchastheauditcommittee.Thosereportsarenotpubliclyavailable,beingconfidentialbetweentheinternalauditorandtherecipient.Externalauditreportsareprovidedtotheshareholdersofacompany.Thereportisattachedtotheannualfinancialstatementsofthecompanyandisthereforepubliclyavailabletotheshareholdersandanyreaderofthefinancialstatements.ScopeofworkTheworkoftheinternalauditornormallyrelatestotheoperationsoftheorganisation,includingthetransactionprocessingsystemsandthesystemstoproducetheannualfinancialstatements.Theinternalauditormayalsoprovideotherreportstomanagement,suchasvalueformoneyauditswhichexternalauditorsrarelybecomeinvolvedwith.Theworkoftheexternalauditorrelatesonlytothefinancialstatementsoftheorganisation.However,theinternalcontrolsystemsoftheorganisationwillbetestedastheseprovideevidenceonthecompletenessandaccuracyofthefinancialstatements.RelationshipwithcompanyInmostorganisations,theinternalauditorisanemployeeoftheorganisation,whichmayhaveanimpactontheauditor’sindependence.However,insomeorganisationstheinternalauditfunctionisoutsourced.Theexternalauditorisappointedbytheshareholdersofanorganisation,providingsomedegreeofindependencefromthecompanyandmanagement.(b)BenefitsofauditcommitteeinConoyCoAssistancewithfinancialreporting(nofinanceexpertise)TheexecutivedirectorsofConoyCodonotappeartohaveanyspecificfinancialskills–asthefinancialdirectorhasrecentlyleftthecompanyandhasnotyetbeenreplaced.ThismaymeanthatfinancialreportinginConoyCoislimitedorthattheothernon-financialdirectorsspendasignificantamountoftimekeepinguptodateonfinancialreportingissues.AnauditcommitteewillassistConoyCobyprovidingspecialistknowledgeoffinancialreportingonatemporarybasis–atleastoneofthenewappointeesshouldhaverelevantandrecentfinancialreportingexperienceundercodesofcorporategovernance.ThiswillallowtheexecutivedirectorstofocusonrunningConoyCo.EnhanceinternalcontrolsystemsTheboardofConoyCodonotnecessarilyunderstandtheworkoftheinternalauditor,ortheneedforcontrolsystems.ThismeansthatinternalcontrolwithinConoyComaybeinadequateorthatemployeesmaynotrecognisetheimportanceofinternalcontrolsystemswithinanorganisation.TheauditcommitteecanraiseawarenessoftheneedforgoodinternalcontrolsystemssimplybybeingpresentinConoyCoandbyeducatingtheboardontheneedforsoundcontrols.Improvingtheinternalcontrol‘climate’willensuretheneedforinternalcontrolsisunderstoodandreducecontrolerrors.RelianceonexternalauditorsConoyCo’sinternalauditorscurrentlyreporttotheboardofConoyCo.Aspreviouslynoted,thelackoffinancialandcontrolexpertiseontheboardwillmeanthatexternalauditorreportsandadvicewillnotnecessarilybeunderstood–andtheboardmayrelytoomuchonexternalauditorsIfConoyCoreporttoanauditcommitteethiswilldecreasethedependenceoftheboardontheexternalauditors.Theauditcommitteecantaketimetounderstandtheexternalauditor’scomments,andthenviathenon-executivedirector,ensurethattheboardtakeactiononthosecomments.AppointmentofexternalauditorsAtpresent,theboardofConoyCoappointtheexternalauditors.Thisraisesissuesofindependenceastheboardmaybecometoofamiliarwiththeexternalauditorsandsoappointonthisfriendshipratherthanmerit.Ifanauditcommitteeisestablished,thenthiscommitteecanrecommendtheappointmentoftheexternalauditors.Thecommitteewillhavethetimeandexpertisetoreviewthequalityofserviceprovidedbytheexternalauditors,removingtheindependenceissue.Corporategovernancerequirements–bestpracticeConoyCodonotneedtofollowcorporategovernancerequirements(thecompanyisnotlisted).However,notfollowingthoserequirementsmaystarttohaveadverseeffectsonConoy.Forexample,ConoyCo’sbankisalreadyconcernedaboutthelackoftransparencyinreporting.EstablishinganauditcommitteewillshowthattheboardofConoyCoarecommittedtomaintainingappropriateinternalsystemsinthecompanyandprovidingthestandardofreportingexpectedbylargecompanies.Obtainingthenewbankloanshouldalsobeeasierasthebankwillbesatisfiedwithfinancialreportingstandards.Givennonon-executives–independentadvicetoboardCurrentlyConoyCodoesnothaveanynon-executivedirectors.Thismeansthatthedecisionsoftheexecutivedirectorsarenotbeingchallengedbyotherdirectorsindependentofthecompanyandwithlittleornofinancialinterestinthecompany.Theappointmentofanauditcommitteewithonenon-executivedirectorontheboardofConoyCowillstarttoprovidesomenon-executiveinputtoboardmeetings.Whilenotsufficientintermsofcorporategovernancerequirements(aboutequalnumbersofexecutiveandnon-executivedirectorsareexpected)itdoesshowtheboardofConoyCoareattemptingtoestablishappropriategovernancesystems.AdviceonriskmanagementFinally,thereareothergeneralareaswhereConoyCowouldbenefitfromanauditcommittee.Forexample,lackofcorporategovernancestructuresprobablymeansConoyCodoesnothaveariskmanagementcommittee.Theauditcommitteecanalsoprovideadviceonriskmanagement,helpingtodecreasetheriskexposureofthecompany.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2019-01-04

- 2019-01-04

- 2020-08-19

- 2020-08-19

- 2020-08-19

- 2020-08-19

- 2020-08-19

- 2019-01-04

- 2020-08-19

- 2020-08-19

- 2020-08-19

- 2019-01-04

- 2020-08-19

- 2020-08-19

- 2020-08-19

- 2019-01-04

- 2020-08-19

- 2019-01-04

- 2020-08-19

- 2020-08-19

- 2020-08-19

- 2020-08-19

- 2020-08-19

- 2019-01-04

- 2020-08-19

- 2019-01-04

- 2020-08-19

- 2020-08-19

- 2020-08-19

- 2019-01-04