2020年ACCA考试审计与认证业务(基础)精选考点(6)

发布时间:2020-10-18

今日51题库考试学习网为大家带来“2020年ACCA考试审计与认证业务(基础)精选考点(6)”的相关知识点,各位辛勤备考的小伙伴一起来看看吧。

从四个方面去考虑审计风险:

1. 风险评估程序

ISA 315 gives an overview of the procedures

that the auditor should follow in order to obtain an understanding sufficient

to assess audit risks, and these risks must then be considered when designing

the audit plan. ISA 315 goes on to require that the auditor shall perform risk

assessment procedures to provide a basis for the identification and assessment

of risks of material misstatement at the financial statement and assertion

levels. ISA 315 goes on to identify the following three risk assessment

procedures:

Making inquiries of management and others

within the entity

Auditors must have discussions with the

client’s management about its objectives and expectations, and its plans for

achieving those goals.

Analytical procedures

Analytical procedures performed as risk

assessment procedures should help the auditor in identifying unusual

transactions or positions. They may identify aspects of the entity of which the

auditor was unaware, and may assist in assessing the risks of material

misstatement in order to provide a basis for designing and implementing

responses to the assessed risks.

Observation and inspection

Observation and inspection may also provide

information about the entity and its environment. Examples of such audit

procedures can potentially cover a very broad area, including observation or

inspection of the entity’s operations, documents, and reports prepared by

management, and of the entity’s premises and plant facilities.

ISA 315 requires that risk assessment

procedures should, at a minimum, comprise a combination of the above three

procedures, and the standard also requires that the engagement partner and

other key engagement team members should discuss the susceptibility of the

entity’s financial statements to material misstatement. Key risks can be

identified at any stage of the audit process, and ISA 315 requires that the

engagement partner should also determine which matters are to be communicated

to those engagement team members not involved in the discussion.

2. 理解一个实体

ISA 315 gives detailed guidance about the

understanding required of the entity and its environment by auditors, including

the entity’s internal control systems. Understanding of the entity and its

environment is important for the auditor in order to help identify the risks of

material misstatement, to provide a basis for designing and implementing

responses to assessed risk (see reference below to ISA 330, The Auditor’s

Responses to Assessed Risks), and to ensure that sufficient appropriate audit

evidence is collected. Given that the focus of this article is audit risk,

however, students should ensure that they also make themselves familiar with

the concept of internal control, and the components of internal control

systems.

3. 定义和评估重要风险和可能导致重大误报的风险

In exercising judgement as to which risks

are significant risks, the auditor is required to consider the following:

Whether the risk is a risk of fraud.

Whether the risk is related to recent

significant economic, accounting or other developments, and therefore requires

specific attention.

The complexity of transactions.

Whether the risk involves significant

transactions with related parties.

The degree of subjectivity in the

measurement of financial information related to the risk, especially those

measurements involving a wide range of measurement uncertainty.

Whether the risk involves significant

transactions that are outside the normal course of business for the entity, or

that otherwise appear to be unusual.

4. ISA 330 和风险的反馈

The requirements of ISA 330, The Auditor’s

Responses to Assessed Risks, will be covered in a future article, but

essentially ISA 330 gives guidance about the nature and extent of the testing

required, based on the risk assessment findings.

以上就是51题库考试学习网带给大家的全部内容,相信小伙伴们都了解清楚。预祝大家在ACCA考试中取得满意的成绩,如果想要了解更多关于ACCA考试的资讯,敬请关注51题库考试学习网!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(c) You have just been advised of management’s intention to publish its yearly marketing report in the annual report

that will contain the financial statements for the year ending 31 December 2005. Extracts from the marketing

report include the following:

‘Shire Oil Co sponsors national school sports championships and the ‘Shire Ward’ at the national teaching

hospital. The company’s vision is to continue its investment in health and safety and the environment.

‘Our health and safety, security and environmental policies are of the highest standard in the energy sector. We

aim to operate under principles of no-harm to people and the environment.

‘Shire Oil Co’s main contribution to sustainable development comes from providing extra energy in a cleaner and

more socially responsible way. This means improving the environmental and social performance of our

operations. Regrettably, five employees lost their lives at work during the year.’

Required:

Suggest performance indicators that could reflect the extent to which Shire Oil Co’s social and environmental

responsibilities are being met, and the evidence that should be available to provide assurance on their

accuracy. (6 marks)

(c) Social and environmental responsibilities

Performance indicators

■ Absolute ($) and relative (%) level of investment in sports sponsorship, and funding to the Shire Ward.

■ Increasing number of championship events and participating schools/students as compared with prior year.

■ Number of medals/trophies sponsored at events and/or number awarded to Shire sponsored schools/students.

■ Number of patients treated (successfully) a week/month. Average bed occupancy (daily/weekly/monthly and cumulative

to date).

■ Staffing levels (e.g. of volunteers for sports events, Shire Ward staff and the company):

? ratio of starters to leavers/staff turnover;

? absenteeism (average number of days per person per annum).

1 Withdrawal of the new licence would not create a going concern issue.

2 May also be described as ‘exploration and evaluation’ costs or ‘discovery and assessment’.

■ Number of:

– breaches of health and safety regulations and environmental regulations;

– oil spills;

– accidents and employee fatalities;

– insurance claims.

Evidence

Tutorial note: As there is a wide range of performance indicators that candidates could suggest, there is always a wide range

of possible sources of audit evidence. As the same evidence may contribute to providing assurance on more than one

measure they are not tabulated here, to avoid duplication. However, candidates may justifiably adopt a tabular layout. Also

note, that where measures may be expressed as evidence (e.g. trophies awarded) marks should be awarded only once.

■ Actual level of investment ($) compared with budget and budget compared with prior period.

Tutorial note: Would expect actual to be at least greater than prior year if performance in these areas (health and

safety) has improved.

■ Physical evidence of favourable increases on prior year, for example:

? medals/cups sponsored;

? number of beds available.

■ Increase in favourable press coverage/reports of sponsored events. (Decrease in adverse press about

accidents/fatalities.)

■ Independent surveys (e.g. by marine conservation organisations, welfare groups, etc) comparing Shire favourably with

other oil producers.

■ A reduction in fines paid compared with budget (and prior year).

■ Reduction in legal fees and claims being settled as evidenced by fee notes and correspondence files.

■ Amounts settled on insurance claims and level of insurance cover as compared with prior period.

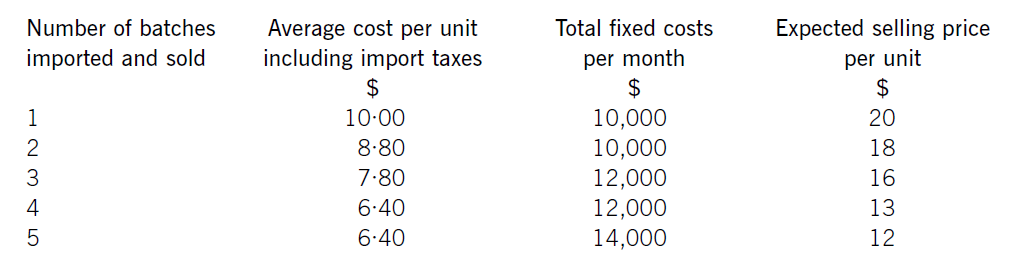

Jewel Co is setting up an online business importing and selling jewellery headphones. The cost of each set of headphones varies depending on the number purchased, although they can only be purchased in batches of 1,000 units. It also has to pay import taxes which vary according to the quantity purchased.

Jewel Co has already carried out some market research and identified that sales quantities are expected to vary depending on the price charged. Consequently, the following data has been established for the first month:

Required:

(a) Calculate how many batches Jewel Co should import and sell. (6 marks)

(b) Explain why Jewel Co could not use the algebraic method to establish the optimum price for its product.

(4 marks)

(b)Thealgebraicmodelrequiresseveralassumptionstobetrue.First,theremustbeaconsistentrelationshipbetweenprice(P)anddemand(Q),sothatademandequationcanbeestablished,usuallyintheform.P=a–bQ.Here,althoughthereisaclearrelationshipbetweenthetwo,itisnotaperfectlylinearrelationshipandsomorecomplicatedtechniquesarerequiredtocalculatethedemandequation.ItalsocannotbeassumedthatalinearrelationshipwillholdforallvaluesofPandQotherthanthefivegiven.Similarly,theremustbeaclearrelationshipbetweendemandandmarginalcost,usuallysatisfiedbyconstantvariablecostperunitandconstantfixedcosts.Thechangingvariablecostsperunitagaincomplicatetheissue,butitisthechangesinfixedcostswhichmakethealgebraicmethodlessusefulinJewel’scase.Thealgebraicmodelisonlysuitableforcompaniesoperatinginamonopolyanditisnotclearherewhetherthisisthecase,butitseemsunlikely,soany‘optimum’pricemightbecomeirrelevantifJewel’scompetitorschargesignificantlylowerprices.Othermoregeneralfactorsnotconsideredbythealgebraicmodelarepoliticalfactorswhichmightaffectimports,socialfactorswhichmayaffectcustomertastesandeconomicfactorswhichmayaffectexchangeratesorcustomerspendingpower.Thereliabilityoftheestimatesthemselves–forsalesprices,variablecostsandfixedcosts–couldalsobecalledintoquestion.

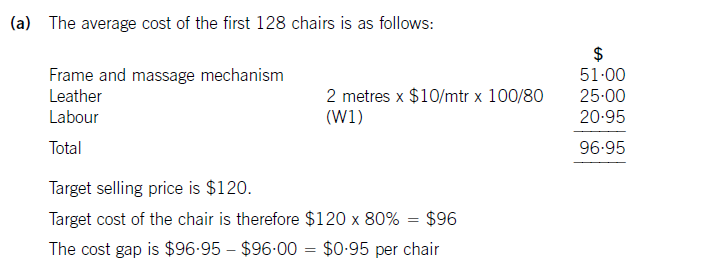

Big Cheese Chairs (BCC) manufactures and sells executive leather chairs. They are considering a new design of massaging chair to launch into the competitive market in which they operate.

They have carried out an investigation in the market and using a target costing system have targeted a competitive selling price of $120 for the chair. BCC wants a margin on selling price of 20% (ignoring any overheads).

The frame. and massage mechanism will be bought in for $51 per chair and BCC will upholster it in leather and assemble it ready for despatch.

Leather costs $10 per metre and two metres are needed for a complete chair although 20% of all leather is wasted in the upholstery process.

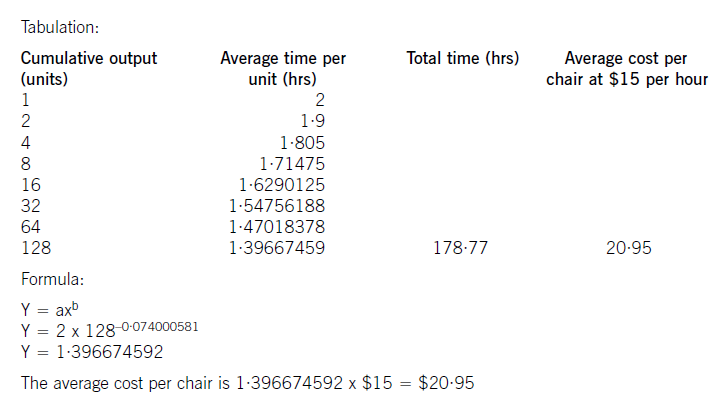

The upholstery and assembly process will be subject to a learning effect as the workers get used to the new design.

BCC estimates that the first chair will take two hours to prepare but this will be subject to a learning rate (LR) of 95%.

The learning improvement will stop once 128 chairs have been made and the time for the 128th chair will be the time for all subsequent chairs. The cost of labour is $15 per hour.

The learning formula is shown on the formula sheet and at the 95% learning rate the value of b is -0·074000581.

Required:

(a) Calculate the average cost for the first 128 chairs made and identify any cost gap that may be present at

that stage. (8 marks)

(b) Assuming that a cost gap for the chair exists suggest four ways in which it could be closed. (6 marks)

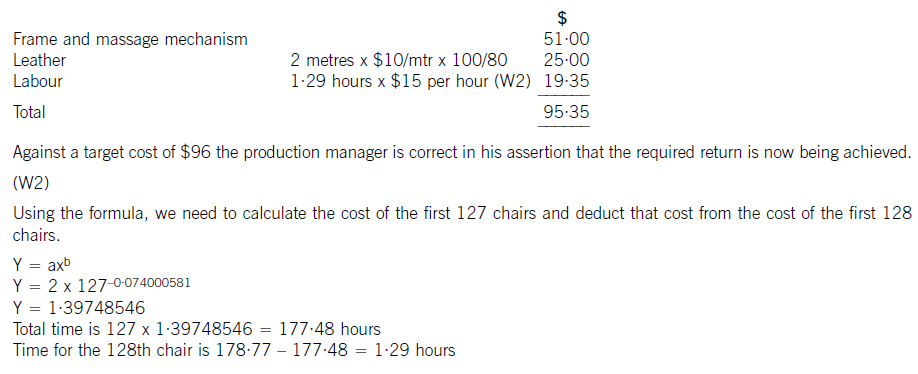

The production manager denies any claims that a cost gap exists and has stated that the cost of the 128th chair will be low enough to yield the required margin.

(c) Calculate the cost of the 128th chair made and state whether the target cost is being achieved on the 128th chair. (6 marks)

(W1)

The cost of the labour can be calculated using learning curve principles. The formula can be used or a tabular approach would

also give the average cost of 128 chairs. Both methods are acceptable and shown here.

(b) To reduce the cost gap various methods are possible (only four are needed for full marks)

– Re-design the chair to remove unnecessary features and hence cost

– Negotiate with the frame. supplier for a better cost. This may be easier as the volume of sales improve as suppliers often

are willing to give discounts for bulk buying. Alternatively a different frame. supplier could be found that offers a better

price. Care would be needed here to maintain the required quality

– Leather can be bought from different suppliers or at a better price also. Reducing the level of waste would save on cost.

Even a small reduction in waste rates would remove much of the cost gap that exists

– Improve the rate of learning by better training and supervision

– Employ cheaper labour by reducing the skill level expected. Care would also be needed here not to sacrifice quality or

push up waste rates.

(c) The cost of the 128th chair will be:

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-10-18

- 2020-10-09

- 2020-10-09

- 2020-10-09

- 2020-10-09

- 2020-10-09

- 2020-10-18

- 2020-10-18

- 2020-10-18

- 2020-10-18

- 2020-10-09

- 2020-10-09

- 2020-10-09

- 2019-01-04

- 2020-10-09

- 2020-10-18

- 2020-10-09

- 2020-10-18

- 2020-10-18

- 2020-10-18

- 2020-10-09

- 2020-10-18

- 2020-10-09

- 2020-10-09

- 2019-01-04

- 2020-10-09

- 2020-10-18

- 2020-10-18

- 2020-10-09

- 2020-10-09