ACCA考试14门科目之间的关系是怎样的呢?

发布时间:2021-03-10

ACCA考试14门科目之间的关系是怎样的呢?

最佳答案

各个科目互为基础和延伸

ACCA F1 Accountant in Business企业会计

ACCA这门课程主要介绍了企业结构和目的以及会计系统的功能,通过这门课的学习,你将能够了解经济,法律法规对于企业财务,人员,环境,信息等方面的规定及影响。会计系统作为企业重要部分将如何处理并提供合理计划。并涉及了企业管理信息系统和会计,审计,内部控制等方面的关系。

F1→P3 F1讲的是企业的内部环境和外部环境是怎样的,P3讲的是内外部环境的变化,对企业来说是更有利了,还是有很多负面的效果,针对企业的内外部环境,企业应当采用怎样的战略。

F1→P1 F1是对职业道德,企业社会责任的简单介绍,P1是集中深入的介绍。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

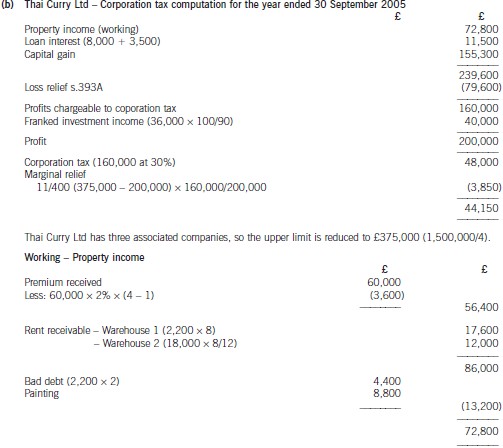

(b) Assuming that Thai Curry Ltd claims relief for its trading loss against total profits under s.393A ICTA 1988,calculate the company’s corporation tax liability for the year ended 30 September 2005. (10 marks)

(iii) Tyre has entered into two new long lease property agreements for two major retail outlets. Annual rentals are paid

under these agreements. Tyre has had to pay a premium to enter into these agreements because of the outlets’

location. Tyre feels that the premiums paid are justifiable because of the increase in revenue that will occur

because of the outlets’ location. Tyre has analysed the leases and has decided that one is a finance lease and

one is an operating lease but the company is unsure as to how to treat this premium. (5 marks)

Required:

Advise the directors of Tyre on how to treat the above items in the financial statements for the year ended

31 May 2006.

(The mark allocation is shown against each of the above items)

(iii) Retail outlets

The two new long lease agreements have been separately classified as an operating lease and a finance lease. The lease

premium paid for a finance lease should be capitalised and recognised as an asset under the lease. IAS17 ‘Leases’ says that

costs identified as directly attributable to a finance lease are added to the amount recognised as an asset. It will be included

in the present value calculation of the minimum lease payments. The finance lease will be recognised at its fair value or if

lower the present value of the minimum lease payments. The premium will be depreciated as part of the asset’s value over

the shorter of the lease term and the asset’s useful life. Initially, a finance lease liability will be set up which is equal to the

value of the leased asset.

The operating lease premium will be spread over the lease term on a straight line basis unless some other method is more

representative. The premium will be effectively treated as a prepayment of rent and is amortised over the life of the agreement.

3 (a) Financial statements often contain material balances recognised at fair value. For auditors, this leads to additional

audit risk.

Required:

Discuss this statement. (7 marks)

3 Poppy Co

(a) Balances held at fair value are frequently recognised as material items in the statement of financial position. Sometimes it is

required by the financial reporting framework that the measurement of an asset or liability is at fair value, e.g. certain

categories of financial instruments, whereas it is sometimes the entity’s choice to measure an item using a fair value model

rather than a cost model, e.g. properties. It is certainly the case that many of these balances will be material, meaning that

the auditor must obtain sufficient appropriate evidence that the fair value measurement is in accordance with the

requirements of financial reporting standards. ISA 540 (Revised and Redrafted) Auditing Accounting Estimates Including Fair

Value Accounting Estimates and Related Disclosures and ISA 545 Auditing Fair Value Measurements and Disclosures

contain guidance in this area.

As part of the understanding of the entity and its environment, the auditor should gain an insight into balances that are stated

at fair value, and then assess the impact of this on the audit strategy. This will include an evaluation of the risk associated

with the balance(s) recognised at fair value.

Audit risk comprises three elements; each is discussed below in the context of whether material balances shown at fair value

will lead to increased risk for the auditor.

Inherent risk

Many measurements based on estimates, including fair value measurements, are inherently imprecise and subjective in

nature. The fair value assessment is likely to involve significant judgments, e.g. regarding market conditions, the timing of

cash flows, or the future intentions of the entity. In addition, there may be a deliberate attempt by management to manipulate

the fair value to achieve a desired aim within the financial statements, in other words to attempt some kind of window

dressing.

Many fair value estimation models are complicated, e.g. discounted cash flow techniques, or the actuarial calculations used

to determine the value of a pension fund. Any complicated calculations are relatively high risk, as difficult valuation techniques

are simply more likely to contain errors than simple valuation techniques. However, there will be some items shown at fair

value which have a low inherent risk, because the measurement of fair value may be relatively straightforward, e.g. assets

that are regularly bought and sold on open markets that provide readily available and reliable information on the market prices

at which actual exchanges occur.

In addition to the complexities discussed above, some fair value measurement techniques will contain significant

assumptions, e.g. the most appropriate discount factor to use, or judgments over the future use of an asset. Management

may not always have sufficient experience and knowledge in making these judgments.

Thus the auditor should approach some balances recognised at fair value as having a relatively high inherent risk, as their

subjective and complex nature means that the balance is prone to contain an error. However, the auditor should not just

assume that all fair value items contain high inherent risk – each balance recognised at fair value should be assessed for its

individual level of risk.

Control risk

The risk that the entity’s internal monitoring system fails to prevent and detect valuation errors needs to be assessed as part

of overall audit risk assessment. One problem is that the fair value assessment is likely to be performed once a year, outside

the normal accounting and management systems, especially where the valuation is performed by an external specialist.

Therefore, as a non-routine event, the assessment of fair value is likely not to have the same level of monitoring or controls

as a day-to-day business transaction.

However, due to the material impact of fair values on the statement of financial position, and in some circumstances on profit,

management may have made great effort to ensure that the assessment is highly monitored and controlled. It therefore could

be the case that there is extremely low control risk associated with the recognition of fair values.

Detection risk

The auditor should minimise detection risk via thorough planning and execution of audit procedures. The audit team may

lack experience in dealing with the fair value in question, and so would be unlikely to detect errors in the valuation techniques

used. Over-reliance on an external specialist could also lead to errors not being found.

Conclusion

It is true that the increasing recognition of items measured at fair value will in many cases cause the auditor to assess the

audit risk associated with the balance as high. However, it should not be assumed that every fair value item will be likely to

contain a material misstatement. The auditor must be careful to identify and respond to the level of risk for fair value items

on an individual basis to ensure that sufficient and appropriate evidence is gathered, thus reducing the audit risk to an

acceptable level.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2021-03-11

- 2021-03-12

- 2021-05-11

- 2021-03-11

- 2021-04-16

- 2021-05-08

- 2021-05-24

- 2021-03-11

- 2021-03-11

- 2021-03-11

- 2021-03-11

- 2021-01-01

- 2021-05-29

- 2021-04-17

- 2021-03-11

- 2021-03-12

- 2021-03-12

- 2021-03-12

- 2021-04-16

- 2021-06-10

- 2021-03-12

- 2021-01-21

- 2021-01-01

- 2021-03-10

- 2021-03-12

- 2021-06-27

- 2021-06-02

- 2021-01-12

- 2021-04-15

- 2021-03-11