2019年9月ACCA考试成绩查询时间10月14日

发布时间:2019-10-06

注意啦注意啦!在2019年9月考季参加ACCA考试的小伙伴们,51题库考试学习网提示:成绩将于2019年10月14日(星期一)公布!

9月ACCA考试成绩查询有如下三种方法:

方法一:电子邮件(e-mail)—您可在 MY ACCA 内选择通过 E-mail 接收考试成绩。

方法二:短信接收(SMS)—您可在 MY ACCA 内选择通过 SMS 接收考试成绩。

方法三:在线查看考试成绩—所有在 ACCA 全球网站上登记的考生都可在线查看自己的考试成绩。

操作如下:

1、登录 http://www.accaglobal.com/uk/en.html

2、进入右上角 MY ACCA,输入 ACCA 学员号及密码登录。

3、点击左侧导航栏 EXAM STATUS

& RESULTS 进行查询。

4、跳转页面后选择View your

status report,进入后就可以查看自己的所有科目的考试通过情况了。

期待自己的成绩吗?那就记准时间,届时都去查询吧!51题库考试学习网预祝所有参加今年9月ACCA考季小伙伴都能收获理想的成绩!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

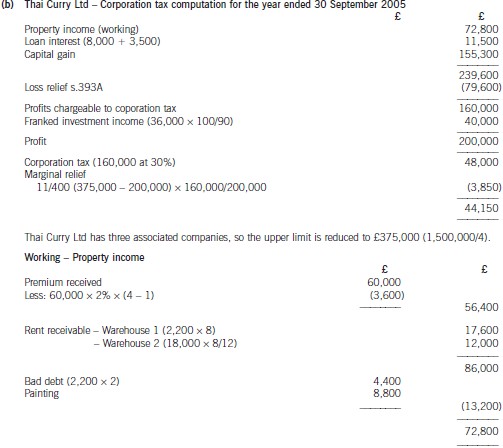

(b) Assuming that Thai Curry Ltd claims relief for its trading loss against total profits under s.393A ICTA 1988,calculate the company’s corporation tax liability for the year ended 30 September 2005. (10 marks)

(b) A sale of industrial equipment to Deakin Co in May 2005 resulted in a loss on disposal of $0·3 million that has

been separately disclosed on the face of the income statement. The equipment cost $1·2 million when it was

purchased in April 1996 and was being depreciated on a straight-line basis over 20 years. (6 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Keffler Co for the year ended

31 March 2006.

NOTE: The mark allocation is shown against each of the three issues.

(b) Sale of industrial equipment

(i) Matters

■ The industrial equipment was in use for nine years (from April 1996) and would have had a carrying value of

$660,000 at 31 March 2005 (11/20 × $1·2m – assuming nil residual value and a full year’s depreciation charge

in the year of acquisition and none in the year of disposal). Disposal proceeds were therefore only $360,000.

■ The $0·3m loss represents 15% of PBT (for the year to 31 March 2006) and is therefore material. The equipment

was material to the balance sheet at 31 March 2005 representing 2·6% of total assets ($0·66/$25·7 × 100).

■ Separate disclosure, of a material loss on disposal, on the face of the income statement is in accordance with

IAS 16 ‘Property, Plant and Equipment’. However, in accordance with IAS 1 ‘Presentation of Financial Statements’,

it should not be captioned in any way that might suggest that it is not part of normal operating activities (i.e. not

‘extraordinary’, ‘exceptional’, etc).

Tutorial note: However, note that if there is a prior period error to be accounted for (see later), there would be

no impact on the current period income statement requiring consideration of any disclosure.

■ The reason for the sale. For example, whether the equipment was:

– surplus to operating requirements (i.e. not being replaced); or

– being replaced with newer equipment (thereby contributing to the $8·1m increase (33·8 – 25·7) in total

assets).

■ The reason for the loss on sale. For example, whether:

– the sale was at an under-value (e.g. to a related party);

– the equipment had a bad maintenance history (or was otherwise impaired);

– the useful life of the equipment is less than 20 years;

– there is any deferred consideration not yet recorded;

– any non-cash disposal proceeds have been overlooked (e.g. if another asset was acquired in a part-exchange).

■ If the useful life was less than 20 years, tangible non-current assets may be materially overstated in respect of other

items of equipment that are still in use and being depreciated on the same basis.

■ If the sale was to a related party then additional disclosure should be required in a note to the financial statements

for the year to 31 March 2006 (IAS 24 ‘Related Party Disclosures’).

Tutorial note: Since there are no specific pointers to a related party transaction (RPT), this point is not expanded

on.

■ Whether the sale was identified in the prior year audit’s post balance sheet event review. If so:

– the disclosure made in the prior year’s financial statements (IAS 10 ‘Events After the Balance Sheet Date’);

– whether an impairment loss was recognised at 31 March 2005.

■ If not, and the equipment was impaired at 31 March 2005, a prior period error should be accounted for (IAS 8

‘Accounting Policies, Changes in Accounting Estimates and Errors’). An impairment loss of $0·3m would have

been material to prior year profit (12·5%).

Tutorial note: Unless this was a RPT or the impairment arose after 31 March 2005 a prior period adjustment

should be made.

■ Failure to account for a prior period error (if any) would result in modification of the audit opinion ‘except for’ noncompliance

with IAS 8 (in the current year) and IAS 36 (in the prior period).

(ii) Audit evidence

■ Carrying amount ($0·66m as above) agreed to the non-current asset register balances at 31 March 2005 and

recalculation of the loss on disposal.

■ Cost and accumulated depreciation removed from the asset register in the year to 31 March 2006.

■ Receipt of proceeds per cash book agreed to bank statement.

■ Sales invoice transferring title to Deakin.

■ A review of maintenance expenses and records (e.g. to confirm reason for loss on sale).

■ Post balance sheet event review on prior year audit working papers file.

■ Management representation confirming that Deakin is not a related party (provided that there is no evidence to

suggest otherwise).

(d) What criteria would you use to assess whether Universal is an ‘excellent’ company? (5 marks)

(d) One of the most widely used models to identify excellence is that of Peters and Waterman developed in their research into

excellent American companies. Interestingly, they agreed with Leavitt in that the companies identified as excellent, whether

they were manufacturers or service businesses, could be seen as offering an excellent service to their customers. This required

them to understand what their customers really valued and then put in place the resources, competences and decision making

processes that delivered the desired attributes. Excellence was positively associated with innovation. Using their checklist of

excellent attributes, Universal could see to be excellent in the following ways:

A bias for action – there is evidence to suggest that both Matthew and Simon are action orientated. They showed an admirable

willingness to experiment and develop a service that added significant value to the customer experience.

Hands-on, value driven – again, the commitment to deliver a quality service – one that they are totally familiar with and able

to deliver themselves – suggests that this value is communicated and shared with staff. The use of self employed installers

and sales people make this commitment particularly important.

Close to the customer – all the evidence points to a real and deep understanding of customer needs. The opportunity for the

business stems from the poor customer service provided by their small competitors. Systems are designed to achieve the ‘no

surprises’ service, which leads to significant levels of customer recommendation and advocacy.

Autonomy and entrepreneurship – there is evidence of a strong belief that individuals and teams should be encouraged to

compete with one another, but not in ways that compromise the quality of the service delivered.

Simple form. – lean staff – Universal is a small functionally managed firm. There is no evidence of creating a large

headquarters, since managers are closely involved with the day-to-day management of their function.

Productivity through people – people are key to the service provided and there is recognition that teams are crucial to the

firm’s growth and success.

Simultaneous loose-tight properties – more difficult to identify in a small company, but there is clearly commitment to shared

values and giving people the freedom to achieve results within this value framework.

These measures of excellence again show the importance of ‘hard’ and ‘soft’ factors in achieving outstanding performance.

An alternative interpretation is to see these attributes as critical success factors, which if achieved, are clearly linked to key

performance indicators. Universal’s growth shows the link between strategy and the qualities needed to achieve this growth.

The ubiquitous balanced scorecard could also be used to measure four key criteria of company performance and

benchmarking the company against the major installers could also provide evidence of excellence. The recent gaining of a

government award for Universal’s contribution to inner city job creation is also a useful indicator of all round excellence.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2021-04-07

- 2020-09-05

- 2020-09-05

- 2020-01-10

- 2020-08-12

- 2020-01-10

- 2020-08-12

- 2020-09-05

- 2020-08-12

- 2020-12-24

- 2020-09-05

- 2020-01-10

- 2019-03-20

- 2020-09-05

- 2020-09-05

- 2020-03-20

- 2020-09-04

- 2021-01-08

- 2021-04-08

- 2021-04-04

- 2020-09-05

- 2020-04-01

- 2021-01-06

- 2020-09-05

- 2019-01-05

- 2019-01-05

- 2020-09-05

- 2021-04-07

- 2020-10-19

- 2019-01-05