大一在校大学生可不可以去考ACCA考试?

发布时间:2021-04-25

很多第一次备考ACCA考试的考生都会有个疑问,在校生可不可以备考ACCA考试,接下来就和51题库考试学习网一起去了解下具体情况吧!

ACCA有13门学科,每一年顶多考8门,快则2年取得,基本上3-5年取得,因此从大一逐渐开始学,假如顺利得话能在大叁、大四取得。可是假如您有考研计划,ACCA还没有考过,那么ACCA就需要先放一放提前准备研究生的复习了。读研究生期内再紧接着考ACCA。

大一新生及在校学生怎样学习ACCA?

ACCA考试的优点之一便是取决于它的学习形式非常灵便。实际上除开一小部分在校大学生可以进到院校设立的方位班学习培训ACCA之外,绝大多数在考ACCA的在校大学生全是通过培训学校来学习培训。

假如想做到一个理想化的情况,便是大学期内能通过基础环节的课程内容,从而获得有益于找个工作的分阶段考证,提议以下:

大一逐渐开始,满足申请注册取得材料,开展FIA/ACCA申请注册,并通过BT、MA、FA

大二上学期,学习培训3门课程内容(LW-TX)+得到语言证书申请OBU申请办理资质

大二下期,学习培训3门课程内容(FR-FM)

大叁上学期学习培训2门课程内容(SBR+SBL)前九门通过就可以申请办理得到高级商业会计证书,也可申请办理英国牛津布鲁克斯大学的运用会计专业(荣誉)理学士学士学位。

大叁下期学习培训2门(AFM+AFP),或是中止考试,提前准备国内考研、或出国留学雅思;

不考研的同学们,可大四上学期学习培训1门或未通过的学科,并开展本技术专业的毕业考试和毕业实习。大四下学年实习工作,开展本技术专业的论文和实习工作;

考研同学们依据考研结果决策是拿ACCA考证找个工作或是读研究生。

在学习时间层面,依据有工作经验的ACCA老师提议,每天花费2-3钟头或每星期花1至2天的时间专心致志备考ACCA课程内容,并相互配合平常练题及临考做考试真题,即可以做到比较好的学习效率。自然,实际学习时间也要依据报名学科总数及此学科难度系数决策,之上整体规划学科及过程可依据学员本身状况灵便调节。

以上就是51题库考试学习网给大家带来的全部内容,希望能够帮到大家!后续请大家持续关注51题库考试学习网,51题库考试学习网将会为大家持续更新最新、最热的考试资讯!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

Following a competitive tender, your audit firm Cal & Co has just gained a new audit client Tirrol Co. You are the manager in charge of planning the audit work. Tirrol Co’s year end is 30 June 2009 with a scheduled date to complete the audit of 15 August 2009. The date now is 3 June 2009.

Tirrol Co provides repair services to motor vehicles from 25 different locations. All inventory, sales and purchasing systems are computerised, with each location maintaining its own computer system. The software in each location is

the same because the programs were written specifically for Tirrol Co by a reputable software house. Data from each location is amalgamated on a monthly basis at Tirrol Co’s head office to produce management and financial accounts.

You are currently planning your audit approach for Tirrol Co. One option being considered is to re-write Cal & Co’s audit software to interrogate the computerised inventory systems in each location of Tirrol Co (except for head office)

as part of inventory valuation testing. However, you have also been informed that any computer testing will have to be on a live basis and you are aware that July is a major holiday period for your audit firm.

Required:

(a) (i) Explain the benefits of using audit software in the audit of Tirrol Co; (4 marks)

(ii) Explain the problems that may be encountered in the audit of Tirrol Co and for each problem, explain

how that problem could be overcome. (10 marks)

(b) Following a discussion with the management at Tirrol Co you now understand that the internal audit department are prepared to assist with the statutory audit. Specifically, the chief internal auditor is prepared to provide you with documentation on the computerised inventory systems at Tirrol Co. The documentation provides details of the software and shows diagrammatically how transactions are processed through the inventory system. This documentation can be used to significantly decrease the time needed to understand the computer systems and enable audit software to be written for this year’s audit.

Required:

Explain how you will evaluate the computer systems documentation produced by the internal audit

department in order to place reliance on it during your audit. (6 marks)

(a)(i)BenefitsofusingauditsoftwareStandardsystemsatclientThesamecomputerisedsystemsandprogramsasusedinall25branchesofTirrolCo.Thismeansthatthesameauditsoftwarecanbeusedineachlocationprovidingsignificanttimesavingscomparedtothesituationwhereclientsystemsaredifferentineachlocation.UseactualcomputerfilesnotcopiesorprintoutsUseofauditsoftwaremeansthattheTirrolCo’sactualinventoryfilescanbetestedratherthanhavingtorelyonprintoutsorscreenimages.Thelattercouldbeincorrect,byaccidentorbydeliberatemistake.Theauditfirmwillhavemoreconfidencethatthe‘real’fileshavebeentested.TestmoreitemsUseofsoftwarewillmeanthatmoreinventoryrecordscanbetested–itispossiblethatallproductlinescouldbetestedforobsolescenceratherthanasampleusingmanualtechniques.Theauditorwillthereforegainmoreevidenceandhavegreaterconfidencethatinventoryisvaluedcorrectly.CostTherelativecostofusingauditsoftwaredecreasesthemoreyearsthatsoftwareisused.Anycostoverrunsthisyearcouldbeoffsetagainsttheauditfeesinfutureyearswhentheactualexpensewillbeless.(ii)ProblemsontheauditofTirrolTimescale–sixweekreportingdeadline–auditplanningTheauditreportisduetobesignedsixweeksaftertheyearend.Thismeansthattherewillbeconsiderablepressureontheauditortocompleteauditworkwithoutcompromisingstandardsbyrushingprocedures.Thisproblemcanbeovercomebycarefulplanningoftheaudit,useofexperiencedstaffandensuringotherstaffsuchassecondpartnerreviewsarebookedwellinadvance.Timescale–sixweekreportingdeadline–softwareissuesTheauditreportisduetobesignedaboutsixweeksaftertheyearend.Thismeansthatthereislittletimetowriteandtestauditsoftware,letaloneusethesoftwareandevaluatetheresultsoftesting.Thisproblemcanbealleviatedbycarefulplanning.AccesstoTirrolCo’ssoftwareanddatafilesmustbeobtainedassoonaspossibleandworkcommencedontailoringCal&Co’ssoftwarefollowingthis.Specialistcomputerauditstaffshouldbebookedassoonaspossibletoperform.thiswork.FirstyearauditcostsTherelativecostsofanauditinthefirstyearataclienttendtobegreaterduetotheadditionalworkofascertainingclientsystems.ThismeansthatCal&Comayhavealimitedbudgettodocumentsystemsincludingcomputersystems.Thisproblemcanbealleviatedtosomeextentagainbygoodauditplanning.Themanagermustalsomonitortheauditprocesscarefully,ensuringthatanyadditionalworkcausedbytheclientnotprovidingaccesstosystemsinformationincludingcomputersystemsisidentifiedandaddedtothetotalbillingcostoftheaudit.StaffholidaysMostoftheauditworkwillbecarriedoutinJuly,whichisalsothemonthwhenmanyofCal&Costafftaketheirannualholiday.Thismeansthattherewillbeashortageofauditstaff,particularlyasauditworkforTirrolCoisbeingbookedwithlittlenotice.Theproblemcanbealleviatedbybookingstaffassoonaspossibleandthenidentifyinganyshortages.Wherenecessary,staffmaybeborrowedfromotherofficesorevendifferentcountriesonasecondmentbasiswhereshortagesareacute.Non-standardsystemsTirrolCo’scomputersoftwareisnon-standard,havingbeenwrittenspecificallyfortheorganisation.Thismeansthatmoretimewillbenecessarytounderstandthesystemthanifstandardsystemswereused.Thisproblemcanbealleviatedeitherbyobtainingdocumentationfromtheclientorbyapproachingthesoftwarehouse(withTirrolCo’spermission)toseeiftheycanassistwithprovisionofinformationondatastructuresfortheinventorysystems.ProvisionofthisinformationwilldecreasethetimetakentotailorauditsoftwareforuseinTirrolCo.IssuesoflivetestingCal&Cohasbeeninformedthatinventorysystemsmustbetestedonalivebasis.Thisincreasestheriskofaccidentalamendmentordeletionofclientdatasystemscomparedtotestingcopyfiles.Tolimitthepossibilityofdamagetoclientsystems,Cal&CocanconsiderperforminginventorytestingondayswhenTirrolCoisnotoperatinge.g.weekends.Attheworst,backupsofdatafilestakenfromthepreviousdaycanbere-installedwhenCal&Co’stestingiscomplete.ComputersystemsTheclienthas25locations,witheachlocationmaintainingitsowncomputersystem.Itispossiblethatcomputersystemsarenotcommonacrosstheclientduetoamendmentsmadeatthebranchlevel.Thisproblemcanbeovercometosomeextentbyaskingstaffateachbranchwhethersystemshavebeenamendedandfocusingauditworkonmaterialbranches.UsefulnessofauditsoftwareTheuseofauditsoftwareatTirrolCodoesappeartohavesignificantproblemsthisyear.Thismeansthateveniftheauditsoftwareisready,theremaystillbesomeriskofincorrectconclusionsbeingderivedduetolackoftesting,etc.Thisproblemcanbealleviatedbyseriouslyconsideringthepossibilityofusingamanualauditthisyear.Themanagermayneedtoinvestigatewhetheramanualauditisfeasibleandifsowhetheritcouldbecompletedwithinthenecessarytimescalewithminimalauditrisk.(b)RelianceoninternalauditdocumentationTherearetwoissuestoconsider;theabilityofinternalaudittoproducethedocumentationandtheactualaccuracyofthedocumentationitself.Theabilityoftheinternalauditdepartmenttoproducethedocumentationcanbedeterminedby:–Ensuringthatthedepartmenthasstaffwhohaveappropriatequalifications.Provisionofarelevantqualificatione.g.membershipofacomputerrelatedinstitutewouldbeappropriate.–Ensuringthatthisandsimilardocumentationisproducedusingarecognisedplanandthatthedocumentationistestedpriortouse.Theuseofdifferentstaffintheinternalauditdepartmenttoproduceandtestdocumentationwillincreaseconfidenceinitsaccuracy.–Ensuringthatthedocumentationisactuallyusedduringinternalauditworkandthatproblemswithdocumentationarenotedandinvestigatedaspartofthatwork.Beinggivenaccesstointernalauditreportsontheinventorysoftwarewillprovideappropriateevidence.Regardingtheactualdocumentation:–Reviewingthedocumentationtoensurethatitappearslogicalandthattermsandsymbolsareusedconsistentlythroughout.Thiswillprovideevidencethattheflowcharts,etcshouldbeaccurate.–Comparingthedocumentationagainstthe‘live’inventorysystemtoensureitcorrectlyreflectstheinventorysystem.Thiscomparisonwillincludetracingindividualtransactionsthroughtheinventorysystems.–UsingpartofthedocumentationtoamendCal&Co’sauditsoftware,andthenensuringthatthesoftwareprocessesinventorysystemdataaccurately.However,thisstagemaybelimitedduetotheneedtouselivefilesatTirrolCo.

12 At 1 July 2004 a company had prepaid insurance of $8,200. On 1 January 2005 the company paid $38,000 for

insurance for the year to 30 September 2005.

What figures should appear for insurance in the company’s financial statements for the year ended 30 June

2005?

Income statement Balance sheet

A $27,200 Prepayment $19,000

B $39,300 Prepayment $9,500

C $36,700 Prepayment $9,500

D $55,700 Prepayment $9,500

(ii) the strategy of the business regarding its treasury policies. (3 marks)

(Marks will be awarded in part (b) for the identification and discussion of relevant points and for the style. of the

report.)

(ii) Strategy of the business regarding its treasury policies

Treasury policies are reviewed regularly by the Board. It is group policy to account for all financial instruments as cash

flow hedges. As a result, changes in the fair values of financial instruments are deferred in reserves to the extent the

hedge is effective and released to profit or loss in the time periods in which the hedged item impacts profit or loss.

The Group contracts fixed rate currency swaps and issues floating to fixed rate interest rate swaps to meet the objective

of protecting borrowing costs. The cash flow effects of the interest rate swaps match the cash flows on the underlying

instruments so that there is no net cash flow effect from movements in market interest rates. If the interest rate swaps

had not been transacted there could have been an increase in the annual net interest payable to the Group. The strategy

of the group is to minimise the exposure to interest rate fluctuations.

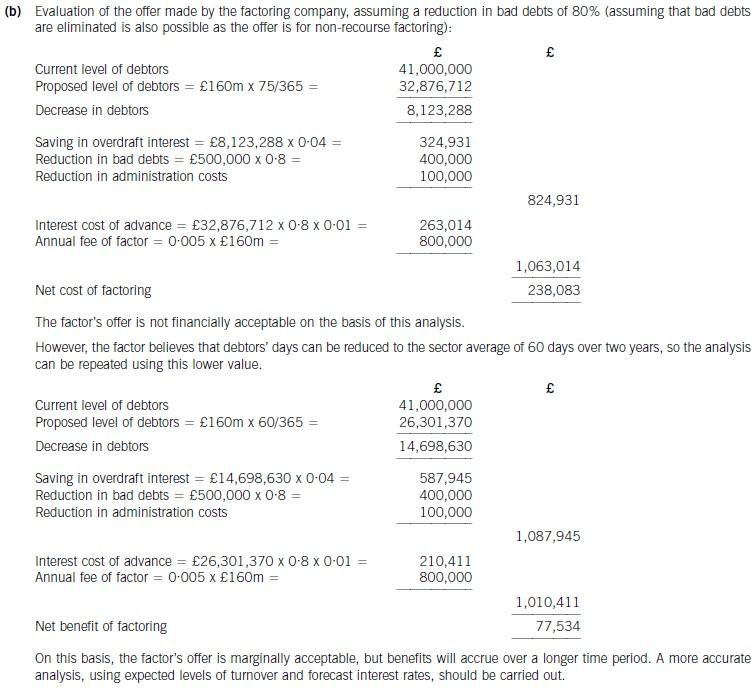

(b) Determine whether the factoring company’s offer can be recommended on financial grounds. Assume a

working year of 365 days and base your analysis on financial information for 2006. (8 marks)

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-10

- 2020-09-03

- 2020-09-03

- 2020-02-27

- 2020-01-10

- 2020-02-27

- 2020-01-09

- 2021-05-22

- 2020-01-10

- 2020-01-10

- 2020-02-26

- 2020-01-29

- 2020-01-30

- 2021-04-24

- 2020-01-10

- 2020-01-10

- 2020-01-08

- 2020-01-09

- 2020-02-27

- 2020-09-03

- 2020-01-08

- 2020-01-10

- 2020-08-12

- 2020-01-05

- 2020-01-09

- 2021-01-21

- 2020-01-09

- 2020-02-23

- 2020-04-10

- 2020-03-22