辽宁省考生:2020年ACCA国际会计师几月份考试?

发布时间:2020-01-09

你是否因为自己错过2019年12月份的ACCA考试的报名时间而懊恼呢?自己呕心沥血准备几个月的考试就因为没有及时报名而前功尽弃了?那么,51题库考试学习网想告诉大家:好消息来啦!2020年ACCA国家会计师考试报名时间新鲜出炉啦~最近的一次考试就在两个月之后哟,有参加的同学可以开始备考啦!具体的时间如下所示:

首先是报名的时间节点,目前2020年3月份ACCA考试提前报名的时间已于2019年11月11日结束了,而常规报名时间仍在继续,持续时间到2020年1月27日,没有报名的同学赶紧去报名呀~不要到时候又遇到错过时间的尴尬局面:

以上是2020年ACCA四个考季的报名时间,有想报名的同学要随时关注时间哟~

了解完了报名时间,那么考试的具体时间又是什么时候呢?别担心,51题库考试学习网会为大家奉上2020年一整年的ACCA考试时间:

以上就是2020年ACCA考试的报名时间和考试时间的具体情况,51题库考试学习网提醒大家,在备考的同时千万不要忘记这些重要的时间节点哟~错过任何一个对大家来说都是一大损失。建议大家将自己考试的时间记录在一个明显且自己能够天天看到的位置,以免忘记。最后,大家还是需要根据自己实际的学习情况来报考,祝大家考试顺利通过~

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

6 Alasdair, aged 42, is single. He is considering investing in property, as he has heard that this represents a good

investment. In order to raise the funds to buy the property, he wants to extract cash from his personal company, Beezer

Limited, whose year end is 31 December.

Beezer Limited was formed on 1 May 1998 with £1,000 of capital issued as 1,000 £1 ordinary shares, and traded

until 1 January 2005 when Alasdair sold the trade and related assets. The company’s only asset is cash of

£120,000. Alasdair wants to extract this cash from the company with the minimum amount of tax payable. He is

considering either, paying himself a dividend of £120,000, on 31 March 2006, after which the company would have

no assets and be wound up or, leaving the cash in the company and then liquidating the company. Costs of liquidation

of £5,000 would then be incurred.

Since Beezer Limited ceased trading, Alasdair has been taken on as a partner at a marketing firm, Gallus & Co. He

estimates his profit share for the year of assessment 2005/06 will be £30,000. He has not made any capital disposals

in the current tax year.

Alasdair wishes to reinvest the cash extracted from Beezer Limited in property but is not sure whether he should invest

directly in residential or commercial property, or do so via some form. of collective investment. He is aware that Gallus

& Co are looking to rent a new warehouse which could be bought for £200,000. Alasdair thinks that he may be able

to buy the warehouse himself and lease it to his firm, but only if he can borrow the additional money to buy the

property.

Alasdair has a 25% shareholding in another company, Glaikit Limited, whose year end is 31 March. The remaining

shares in this company are held by his friend, Gill. Alasdair is considering borrowing £15,000 from Glaikit Limited

on 1 January 2006. He does not intend to pay any interest on the loan, which is likely to be written off some time

in 2007. Alasdair does not have any connection with Glaikit Limited other than his shareholding.

Required:

(a) Advise Alasdair whether or not a dividend payment will result in a higher after-tax cash sum than the

liquidation of Beezer Limited. Assume that either the dividend would be paid on 31 March 2006 or the

liquidation would take place on 31 March 2006. (9 marks)

Assume that Beezer Limited has always paid corporation tax at or above the small companies rate of 19%

and that the tax rates and allowances for 2004/05 apply throughout this part.

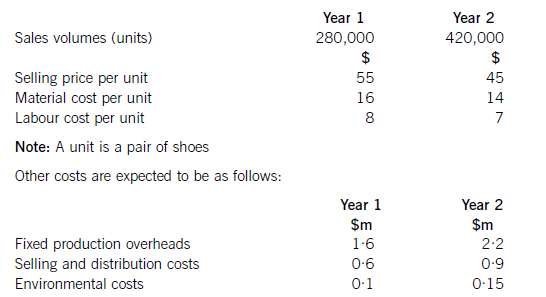

Shoe Co, a shoe manufacturer, has developed a new product called the ‘Smart Shoe’ for children, which has a built-in tracking device. The shoes are expected to have a life cycle of two years, at which point Shoe Co hopes to introduce a new type of Smart Shoe with even more advanced technology. Shoe Co plans to use life cycle costing to work out the total production cost of the Smart Shoe and the total estimated profit for the two-year period.

Shoe Co has spent $5·6m developing the Smart Shoe. The time spent on this development meant that the company missed out on the opportunity of earning an estimated $800,000 contribution from the sale of another product.

The company has applied for and been granted a ten-year patent for the technology, although it must be renewed each year at a cost of $200,000. The costs of the patent application were $500,000, which included $20,000 for the salary costs of Shoe Co’s lawyer, who is a permanent employee of the company and was responsible for preparing the application.

The following information is also available for the next two years:

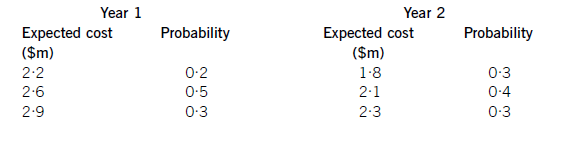

Shoe Co is still negotiating with marketing companies with regard to its advertising campaign, so is uncertain as to what the total marketing costs will be each year. However, the following information is available as regards the probabilities of the range of costs which are likely to be incurred:

Required:

Applying the principles of life cycle costing, calculate the total expected profit for Shoe Co for the two-year period.

(10 marks)

Totalsalesrevenue=(280,000x$55)+(420,000x$45)=$15·4m+18·9m=$34·3m.NoteTheexpectedprofithasbeencalculatedusinglifecyclecostingnotrelevantcosting.Hence,the$20,000salarycostincludedinpatentcostsshouldbeincludedinthelifecyclecost.Similarly,theopportunitycostof$800,000isnotincludedusinglifecyclecostingwhereasifrelevantcostingwasbeingusedtodecideonaparticularcourseofaction,theopportunitycostwouldbeincluded.Working1Expectedmarketingcostinyear1:(0·2x$2·2m)+(0·5x$2·6m)+(0·3x$2·9m)=$2·61mExpectedmarketingcostyear2:(0·3x$1·8m)+(0·4x$2·1m)+(0·3x$2·3m)=$2·07mTotalexpectedmarketingcost=$4·68m

(b) The tax relief available in respect of the anticipated trading losses, together with supporting calculations and

a recommended structure for the business. (16 marks)

Aral Ltd owned by Banda

The losses would have to be carried forward and deducted from the trading profits of the year ending 30 June 2010.

Aral Ltd cannot offset the loss in the current period or carry it back as it has no other income or gains.

Aral Ltd owned by Flores Ltd

The two companies will form. a group relief group if Flores Ltd owns at least 75% of the ordinary share capital of Aral

Ltd. The trading losses could be surrendered to Flores Ltd in the year ending 30 June 2008 and the year ending

30 June 2009. The total tax saved would be £11,079 ((£38,696 + £19,616) x 19%)

Recommended structure

The Aral business should be established in a company owned by Flores Ltd.

This will maximise the relief available in respect of the trading losses and enable relief to be obtained in the period in

which the losses are incurred.

Tutorial note

The whole of the loss for the period ending 30 June 2008 can be surrendered to Flores Ltd as it is less than that

company’s profit for the corresponding period, i.e. £60,000 (£120,000 x 6/12).

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-08

- 2021-01-13

- 2021-01-13

- 2021-01-13

- 2020-02-27

- 2020-08-13

- 2020-01-10

- 2020-08-13

- 2020-02-28

- 2021-04-10

- 2020-01-08

- 2021-02-25

- 2021-10-23

- 2021-04-04

- 2019-12-28

- 2020-01-09

- 2020-09-03

- 2020-02-27

- 2020-01-10

- 2020-01-29

- 2020-01-03

- 2020-01-08

- 2020-01-09

- 2020-02-01

- 2020-01-10

- 2020-09-03

- 2020-01-09

- 2020-02-27

- 2020-01-10

- 2021-06-19