请看!2020年-2021年的ACCA报考条件及科目介绍

发布时间:2020-04-03

特许公认会计师公会成立于1904年,是目前世界上的专业会计师团体,也是国际上海外学员多、学员规模发展快的专业会计师组织。ACCA在国内也被称为"国际注册会计师",ACCA资格被认为是"国际财会界的通行证",许多国家立法许可ACCA会员从事审计、投资顾问和破产执行工作。认可度如此高,ACCA的报考条件是不是也非常高呢?其实不然。凡满足以下条件之一者均可参加ACCA考试:

1、凡具有教育部承认的大专以上学历,即可报名成为ACCA的正式学员;

2、教育部认可的高等院校在校生,顺利完成大一的课程考试,即可报名成为ACCA的正式学员;

3、未符合1、2项报名资格的申请者,也可以先申请参加FIA基础财务资格考试。在完成基础商业会计、基础管理会计、基础财务会计3门课程,并完成ACCA基础职业模块,可获得ACCA商业会计师资格证书,获得资格证书后可豁免ACCA AB-FA三门课程的考试,直接进入技能课程的考试。

那么,ACCA考试需要考几科?

目前,ACCA官方共设置了15门考试科目,其中必须考过13门才能申请成为ACCA会员,十多个科目按难易程度可分为以下几个阶段,第一部分为基础阶段,主要分为知识课程和技能课程两个部分。

知识课程主要涉及财务会计和管理会计方面的核心知识,也为接下去进行技能阶段的详细学习搭建了一个平台。知识课程的三个科目同时也是FIA方式注册学员所学习的FAB、FMA、FFA三个科目。技能课程共有六门课程,广泛的涵盖了一名会计师所涉及的知识领域及必须掌握的技能。

第二部分为专业阶段,主要分为核心课程和选修课程。该阶段的课程相当于硕士阶段的课程

难度,是对第一部分课程的引申和发展。该阶段课程引入了作为未来的高级会计师所必须的更高级的职业技能和知识技能。

选修课程为从事高级管理咨询或顾问职业

的学员,设计了解决更高级和更复杂的问题的技能。

好了,看了上面的内容,相信小伙伴对ACCA的报考条件及课程有了一定的了解。如果还想了解更多信息,欢迎来51题库考试学习网留言。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

You are the audit supervisor of Maple & Co and are currently planning the audit of an existing client, Sycamore Science Co (Sycamore), whose year end was 30 April 2015. Sycamore is a pharmaceutical company, which manufactures and supplies a wide range of medical supplies. The draft financial statements show revenue of $35·6 million and profit before tax of $5·9 million.

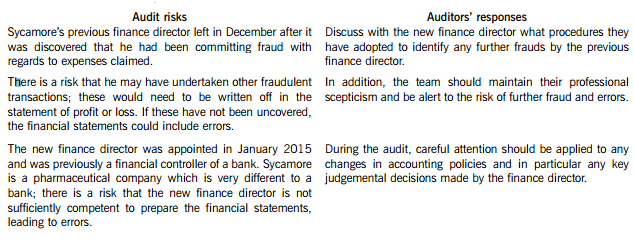

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

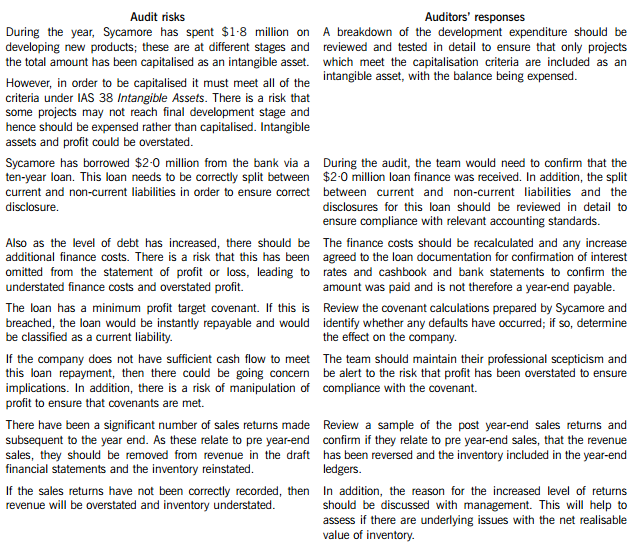

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

(a) Fraud responsibility

Maple & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error.

In order to fulfil this responsibility, Maple & Co is required to identify and assess the risks of material misstatement of the financial statements due to fraud.

They need to obtain sufficient appropriate audit evidence regarding the assessed risks of material misstatement due to fraud, through designing and implementing appropriate responses. In addition, Maple & Co must respond appropriately to fraud or suspected fraud identified during the audit.

When obtaining reasonable assurance, Maple & Co is responsible for maintaining professional scepticism throughout the audit, considering the potential for management override of controls and recognising the fact that audit procedures which are effective in detecting error may not be effective in detecting fraud.

To ensure that the whole engagement team is aware of the risks and responsibilities for fraud and error, ISAs require that a discussion is held within the team. For members not present at the meeting, Sycamore’s audit engagement partner should determine which matters are to be communicated to them.

(b) Audit risks and auditors’ responses

(c) (i) Review engagements

Review engagements are often undertaken as an alternative to an audit, and involve a practitioner reviewing financial data, such as six-monthly figures. This would involve the practitioner undertaking procedures to state whether anything has come to their attention which causes the practitioner to believe that the financial data is not in accordance with the financial reporting framework.

A review engagement differs to an external audit in that the procedures undertaken are not nearly as comprehensive as those in an audit, with procedures such as analytical review and enquiry used extensively. In addition, the practitioner does not need to comply with ISAs as these only relate to external audits.

(ii) Levels of assurance

The level of assurance provided by audit and review engagements is as follows:

External audit – A high but not absolute level of assurance is provided, this is known as reasonable assurance. This provides comfort that the financial statements present fairly in all material respects (or are true and fair) and are free of material misstatements.

Review engagements – where an opinion is being provided, the practitioner gathers sufficient evidence to be satisfied that the subject matter is plausible; in this case negative assurance is given whereby the practitioner confirms that nothing has come to their attention which indicates that the subject matter contains material misstatements.

(b) Explain in the context of Flavours Fine Foods, what is meant by:

(i) responsibility; (4 marks)

(b) (i) RESPONSIBILITY is the liability of a person to be called to account for their actions and results, and is therefore an obligation to take some action to discharge that responsibility. Unlike authority, responsibility cannot be delegated. There is however some discussion on the extent to which this statement is true: the idea that responsibility cannot be delegated is too simplistic. Any task contains an element of responsibility. It is the idea of accountability and the direction of responsibility that is the relevant concept and is the problem at Flavours Fine Foods; ultimate responsibility resides with the owners. It is self evident that it is impossible to exercise authority without responsibility because this could lead to problems of control and therefore undesirable outcomes for the organisation. However, the superior (the owner) is always ultimately responsible for the actions of his or her subordinates. The key element here is the recognition of discretion by virtue of the person’s position. This underlines the doctrine of absolute responsibility; the superior is always ultimately accountable.

3 Susan Paullaos was recently appointed as a non-executive member of the internal audit committee of Gluck and

Goodman, a public listed company producing complex engineering products. Barney Chester, the executive finance

director who chairs the committee, has always viewed the purpose of internal audit as primarily financial in nature

and as long as financial controls are seen to be fully in place, he is less concerned with other aspects of internal

control. When Susan asked about operational controls in the production facility Barney said that these were not the

concern of the internal audit committee. This, he said, was because as long as the accounting systems and financial

controls were fully functional, all other systems may be assumed to be working correctly.

Susan, however, was concerned with the operational and quality controls in the production facility. She spoke to

production director Aaron Hardanger, and asked if he would be prepared to produce regular reports for the internal

audit committee on levels of specification compliance and other control issues. Mr Hardanger said that the internal

audit committee had always trusted him because his reputation as a manager was very good. He said that he had

never been asked to provide compliance evidence to the internal audit committee and saw no reason as to why he

should start doing so now.

At board level, the non-executive chairman, George Allejandra, said that he only instituted the internal audit committee

in the first place in order to be seen to be in compliance with the stock market’s requirement that Gluck and Goodman

should have one. He believed that internal audit committees didn’t add materially to the company. They were, he

believed, one of those ‘outrageous demands’ that regulatory authorities made without considering the consequences

in smaller companies nor the individual needs of different companies. He also complained about the need to have an

internal auditor. He said that Gluck and Goodman used to have a full time internal auditor but when he left a year

ago, he wasn’t replaced. The audit committee didn’t feel it needed an internal auditor because Barney Chester believed

that only financial control information was important and he could get that information from his management

accountant.

Susan asked Mr Allejandra if he recognised that the company was exposing itself to increased market risks by failing

to have an effective audit committee. Mr Allejandra said he didn’t know what a market risk was.

Required:

(a) Internal control and audit are considered to be important parts of sound corporate governance.

(i) Describe FIVE general objectives of internal control. (5 marks)

3 (a) (i) FIVE general objectives of internal control

An internal control system comprises the whole network of systems established in an organisation to provide reasonable

assurance that organisational objectives will be achieved.

Specifically, the general objectives of internal control are as follows:

To ensure the orderly and efficient conduct of business in respect of systems being in place and fully implemented.

Controls mean that business processes and transactions take place without disruption with less risk or disturbance and

this, in turn, adds value and creates shareholder value.

To safeguard the assets of the business. Assets include tangibles and intangibles, and controls are necessary to ensure

they are optimally utilised and protected from misuse, fraud, misappropriation or theft.

To prevent and detect fraud. Controls are necessary to show up any operational or financial disagreements that might

be the result of theft or fraud. This might include off-balance sheet financing or the use of unauthorised accounting

policies, inventory controls, use of company property and similar.

To ensure the completeness and accuracy of accounting records. Ensuring that all accounting transactions are fully and

accurately recorded, that assets and liabilities are correctly identified and valued, and that all costs and revenues can be

fully accounted for.

To ensure the timely preparation of financial information which applies to statutory reporting (of year end accounts, for

example) and also management accounts, if appropriate, for the facilitation of effective management decision-making.

[Tutorial note: candidates may address these general objectives using different wordings based on analyses of different

study manuals. Allow latitude]

4 Assume today’s date is 15 May 2005.

In March 1999, Bob was made redundant from his job as a furniture salesman. He decided to travel round the world,

and did so, returning to the UK in May 2001. Bob then decided to set up his own business selling furniture. He

started trading on 1 October 2001. After some initial success, the business made losses as Bob tried to win more

customers. However, he was eventually successful, and the business subsequently made profits.

The results for Bob’s business were as follows:

Period Schedule D Case I

Trading Profits/(losses)

£

1 October 2001 – 30 April 2002 13,500

1 May 2002 – 30 April 2003 (18,000)

1 May 2003 – 30 April 2004 28,000

Bob required funds to help start his business, so he raised money in three ways:

(1) Bob is a keen cricket fan, and in the 1990s, he collected many books on cricket players. To raise money, Bob

started selling books from his collection. These had risen considerably in value and sold for between £150 and

£300 per book. None of the books forms part of a set. Bob created an internet website to advertise the books.

Bob has not declared this income, as he believes that the proceeds from selling the books are non-taxable.

(2) He disposed of two paintings and an antique silver coffee set at auction on 1 December 2004, realising

chargeable gains totalling £23,720.

(3) Bob took a part time job in a furniture store on 1 January 2003. His annual salary has remained at £12,600

per year since he started this employment.

Bob has 5,000 shares in Willis Ltd, an unquoted trading company based in the UK. He subscribed for these shares

in August 2000, paying £3 per share. On 1 December 2004, Bob received a letter informing him that the company

had gone into receivership. As a result, his shares were almost worthless. The receivers dealing with the company

estimated that on the liquidation of the company, he would receive no more than 10p per share for his shareholding.

He has not yet received any money.

Required:

(a) Write a letter to Bob advising him on whether or not he is correct in believing that his book sales are nontaxable.

Your advice should include reference to the badges of trade and their application to this case.

(9 marks)

(a) Evidence of trading

[Client address]

[Own address]

[Date]

Dear Bob,

I note that you have been selling some books in order to raise some extra income. While you believe that the sums are not

taxable, I believe that there may be a risk of the book sales being treated as a trade, and therefore taxable under Schedule D

Case I. We need to refer to guidance in the form. of a set of principles known as the ‘badges of trade’. These help determine

whether or not a trade exists, and need to be looked at in their entirety. The badges are as follows.

1. The subject matter

Some assets can be enjoyed by themselves as an investment, while others (such as large amounts of aircraft linen) are

clearly not. It is likely that such assets are acquired as trading stock, and are therefore a sign of trading. Sporting books

can be an investment, and so this test is not conclusive.

2. Frequency of transactions

Where transactions are frequent (not one-offs), this suggests trading. You have sold several books, which might suggest

trading, although you have only done this for a short period - between one and two years.

3. Length of ownership

Where items are bought and sold soon afterwards, this indicates trading. You bought your books in the 1990s, and the

length of time between acquisition and sale would not suggest trading.

4. Supplementary work and marketing

You are actively marketing the books on your internet website, which is an indication of trading.

5. Profit motive

A motive to make profit suggests trading activity. You sold the books to raise funds for your property business, and not

to make a profit as such, which suggests that your motive was to raise cash, and not make profits.

6. The way in which the asset sold was acquired.

Selling assets which were acquired unintentionally (such as a gift) is not usually seen as trading. You acquired the books

for your collection over a period of time, and while these were intentional acquisitions, the reasons for doing so were for

your personal pleasure.

By applying all of these tests, it should be possible to argue that you were not trading, merely selling some assets in

order to generate short-term cash for your business.

The asset disposals will be taxed under the capital gain tax rules, but as the books are chattels and do not form. part of

a set, they will be exempt from capital gains tax.

Yours sincerely

A N. Accountant

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-02-26

- 2020-04-16

- 2020-02-22

- 2021-04-25

- 2021-01-16

- 2020-02-27

- 2020-08-15

- 2020-02-23

- 2021-01-13

- 2020-01-09

- 2020-02-20

- 2020-07-04

- 2021-01-13

- 2020-09-03

- 2020-01-09

- 2020-01-10

- 2020-03-22

- 2020-01-10

- 2019-03-08

- 2021-04-08

- 2020-01-29

- 2021-04-02

- 2020-09-03

- 2020-01-10

- 2020-01-10

- 2020-01-09

- 2019-12-28

- 2020-02-19

- 2020-03-25

- 2019-12-29