ACCA证书含金量到底有多高?

发布时间:2019-07-20

2019年ACCA上半年考试已经结束,下半年考试正式计进入备考期,很多小伙在刚经历完上班年的考的,马上又要进入下半年新一轮的备考,这中间的疲惫相信很多正在备考或者已经考过的人都感同身受,很多考生会在这个阶段质疑说ACCA含金量真的有这么高吗?ACCA证书对求职就业、出国留学、未来发展有什么帮助吗?大这样努力考取这个证书真的是否有意义了?为此小编特地整理了如下内容。

一、ACCA的含金量

ACCA在通关部分科目后,可以申请英国OBU的学士学位和UOL的硕士学位,可以为自己的简历镀金,如果有想要出国留学或者工作都是有一定帮助的,获得学位后,还可以直接申请英联邦国家的硕博研究生。

ACCA在全球有180多个国家认可,被称为国际财会界的"通行证"。现拥有7,200家认可雇主,在中国有近千家签约就业企业,主要为四大会计师事务所、跨国银行、世界500强企业和国际国内大型知名企业。

据ACCA年度薪资调查报告显示,应届生通关ACCA后最低年薪基本不会低于15万。ACCA会员年薪达到30万至50万人民币之间比例高达52%,ACCA会员收入在50万至100万人民币之间比例高达21%,受访会员最高年薪超过200万人民币。

二、ACCA考试优势

ACCA考试周期短:

报名时间分为4个考季,3/6/9/12月,一年可以考4次。

ACCA报考条件低:

1、门槛不高,报考并无专业限制

2、大专学历即可报名

3、在校期间即可参加考试,毕业就拿证

4、无财会背景人士通过学习均可以通过

无论你是财会专业还是非财会专业,如果你想在财会行业有好的发展前景,就去考一个能够带你达到高起点、高薪资,真正有用的“万能通行证”。

三、ACCA就业前景

那考下ACCA之后,能去哪些企业~

1.四大会计师事务所

这个毫无疑问,ACCA这张素有“四大通行证”之称的证书,可谓是通往财会行业权威——四大的绝对加分项。但是,ACCAer可不止四大这一个选择哦~

2.国内会计师事务所

虽然,国际四大一直是财会人心中的圣地,但是近几年来,国内事务所的发展迅猛,收入和排名也随之发生了翻天覆地的变化。今年,身为本土八大的致同挤进前四!拿下ACCA,八大的面试官也会对你青睐有加。

3.投资银行

除了高盛、摩根大通、汇丰这些在国际上赫赫有名的国际银行外,国内的四大银行,也能给ACCA持证人们提供一个很好的施展平台。

4.金融机构

都说,金融、财会不分家,在ACCA的学习大军中,也不乏在金融领域打拼多年的从业者。因为金融工作中涉及到的财务报表、IPO估值等都需要用到财会的内容,所以ACCA可以说是对口证书。

5.500强外企

毫无疑问,ACCA这张起源于英国,适用国际会计准则的高端证书,绝对可以称得上是通往外企的“黄金文凭”。

综合以上就是对于上述ACCA问题的解答了,希望对于各位小伙伴有帮助,小编将持续更新相关内容。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

Explain the grounds upon which a person may be disqualified under the Company Directors Disqualification Act 1986.(10 marks)

The Company Directors Disqualification Act (CDDA) 1986 was introduced to control individuals who persistently abused the various privileges that accompany incorporation, most particularly the privilege of limited liability. The Act applies to more than just directors and the court may make an order preventing any person (without leave of the court) from being:

(i) a director of a company;

(ii) a liquidator or administrator of a company;

(iii) a receiver or manager of a company’s property; or

(iv) in any way, whether directly or indirectly, concerned with or taking part in the promotion, formation or management of a company.

The CDDA 1986 identifies three distinct categories of conduct, which may, and in some circumstances must, lead the court to disqualify certain persons from being involved in the management of companies.

(a) General misconduct in connection with companies

This first category involves the following:

(i) A conviction for an indictable offence in connection with the promotion, formation, management or liquidation of a company or with the receivership or management of a company’s property (s.2 of the CDDA 1986). The maximum period for disqualification under s.2 is five years where the order is made by a court of summary jurisdiction, and 15 years in any other case.

(ii) Persistent breaches of companies legislation in relation to provisions which require any return, account or other document to be filed with, or notice of any matter to be given to, the registrar (s.3 of the CDDA 1986). Section 3 provides that a person is conclusively proved to be persistently in default where it is shown that, in the five years ending with the date of the application, he has been adjudged guilty of three or more defaults (s.3(2) of the CDDA 1986). This is without prejudice to proof of persistent default in any other manner. The maximum period of disqualification under this section is five years.

(iii) Fraud in connection with winding up (s.4 of the CDDA 1986). A court may make a disqualification order if, in the course of the winding up of a company, it appears that a person:

(1) has been guilty of an offence for which he is liable under s.993 of the CA 2006, that is, that he has knowingly been a party to the carrying on of the business of the company either with the intention of defrauding the company’s creditors or any other person or for any other fraudulent purpose; or

(2) has otherwise been guilty, while an officer or liquidator of the company or receiver or manager of the property of the company, of any fraud in relation to the company or of any breach of his duty as such officer, liquidator, receiver or manager (s.4(1)(b) of the CDDA 1986).

The maximum period of disqualification under this category is 15 years.(b) Disqualification for unfitness

The second category covers:

(i) disqualification of directors of companies which have become insolvent, who are found by the court to be unfit to be directors (s.6 of the CDDA 1986). Under s. 6, the minimum period of disqualification is two years, up to a maximum of 15 years;

(ii) disqualification after investigation of a company under Pt XIV of the CA 1985 (it should be noted that this part of the previous Act still sets out the procedures for company investigations) (s.8 of the CDDA 1986). Once again, the maximum period of disqualification is 15 years.

Schedule 1 to the CDDA 1986 sets out certain particulars to which the court is to have regard in deciding whether a person’s conduct as a director makes them unfit to be concerned in the management of a company. In addition, the courts have given indications as to what sort of behaviour will render a person liable to be considered unfit to act as a company director. Thus, in Re Lo-Line Electric Motors Ltd (1988), it was stated that:

‘Ordinary commercial misjudgment is in itself not sufficient to justify disqualification. In the normal case, the conduct complained of must display a lack of commercial probity, although . . . in an extreme case of gross negligence or total incompetence, disqualification could be appropriate.’

(c) Other cases for disqualification

This third category relates to:

(i) participation in fraudulent or wrongful trading under s.213 of the Insolvency Act (IA)1986 (s.10 of the CDDA 1986);

(ii) undischarged bankrupts acting as directors (s.11 of the CDDA 1986); and

(iii) failure to pay under a county court administration order (s.12 of the CDDA 1986).

For the purposes of most of the CDDA 1986, the court has discretion to make a disqualification order. Where, however, a person has been found to be an unfit director of an insolvent company, the court has a duty to make a disqualification order (s.6 of the CDDA 1986). Anyone who acts in contravention of a disqualification order is liable:

(i) to imprisonment for up to two years and/or a fine, on conviction on indictment; or

(ii) to imprisonment for up to six months and/or a fine not exceeding the statutory maximum, on conviction summarily (s.13 of the CDDA 1986).

James died on 22 January 2015. He had made the following gifts during his lifetime:

(1) On 9 October 2007, a cash gift of £35,000 to a trust. No lifetime inheritance tax was payable in respect of this gift.

(2) On 14 May 2013, a cash gift of £420,000 to his daughter.

(3) On 2 August 2013, a gift of a property valued at £260,000 to a trust. No lifetime inheritance tax was payable in respect of this gift because it was covered by the nil rate band. By the time of James’ death on 22 January 2015, the property had increased in value to £310,000.

On 22 January 2015, James’ estate was valued at £870,000. Under the terms of his will, James left his entire estate to his children.

The nil rate band of James’ wife was fully utilised when she died ten years ago.

The nil rate band for the tax year 2007–08 is £300,000, and for the tax year 2013–14 it is £325,000.

Required:

(a) Calculate the inheritance tax which will be payable as a result of James’ death, and state who will be responsible for paying the tax. (6 marks)

(b) Explain why it might have been beneficial for inheritance tax purposes if James had left a portion of his estate to his grandchildren rather than to his children. (2 marks)

(c) Explain why it might be advantageous for inheritance tax purposes for a person to make lifetime gifts even when such gifts are made within seven years of death.

Notes:

1. Your answer should include a calculation of James’ inheritance tax saving from making the gift of property to the trust on 2 August 2013 rather than retaining the property until his death.

2. You are not expected to consider lifetime exemptions in this part of the question. (2 marks)

(a) James – Inheritance tax arising on death

Lifetime transfers within seven years of death

The personal representatives of James’ estate will be responsible for paying the inheritance tax of £348,000.

Working – Available nil rate band

(b) Skipping a generation avoids a further charge to inheritance tax when the children die. Gifts will then only be taxed once before being inherited by the grandchildren, rather than twice.

(c) (1) Even if the donor does not survive for seven years, taper relief will reduce the amount of IHT payable after three years.

(2) The value of potentially exempt transfers and chargeable lifetime transfers are fixed at the time they are made.

(3) James therefore saved inheritance tax of £20,000 ((310,000 – 260,000) at 40%) by making the lifetime gift of property.

(b) What advantages and disadvantages might result from outsourcing Global Imaging’s HR function?

(8 marks)

(b) It is important to note that there is nothing in the nature of the activities carried out by HR staff and departments that prevents

outsourcing being looked at as a serious option. Indeed, amongst larger companies the outsourcing of some parts of the HR

function is already well under way, with one source estimating that HR outsourcing is growing by 27% each year. Paul,

therefore, needs to look at the HR activities identified above and assess the advantages and disadvantages of outsourcing a

particular HR activity. Outsourcing certain parts of the recruitment process has long been accepted, with professional

recruitment agencies and ‘head-hunters’ being heavily involved in the advertising and short listing of candidates for senior

management positions. Some HR specialists argue that outsourcing much of the routine personnel work, including

maintaining employees’ records, frees the HR specialist to make a real contribution to the strategic planning process. One

study argues that ‘HR should become a partner with senior and line managers in strategy execution’.

If Paul is able to outsource the routine HR activities this will free him to contribute to the development of the growth strategy

and the critical people needs that strategy will require. In many ways the HR specialist is in a unique position to assess current

skills and capabilities of existing staff and the extent to which these can be ‘leveraged’ to achieve the desired strategy. In

Hamel and Prahalad’s terms this strategy is likely to ‘stretch’ the people resources of the company and require the recruitment

of additional staff with the relevant capabilities. Paul needs to show how long it will take to develop the necessary staff

resources as this will significantly influence the time needed to achieve the growth strategy.

Outsourcing passes on to the provider the heavy investment needed if the company sets up its own internal HR services with

much of this investment now going into web-based systems. The benefits are reduced costs and improved service quality.

The downside is a perceived loss of control and a reduced ability to differentiate the HR function from that of competitors.

Issues of employee confidentiality are also relevant in the decision to outsource.

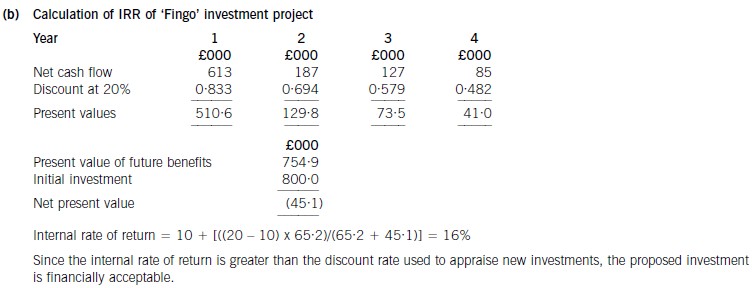

(b) Calculate the internal rate of return of the proposed investment and comment on your findings. (5 marks)

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-08

- 2020-01-08

- 2021-02-25

- 2020-02-29

- 2020-02-29

- 2019-07-20

- 2020-01-08

- 2020-01-08

- 2020-01-08

- 2019-07-20

- 2019-07-20

- 2019-07-20

- 2019-07-20

- 2020-01-08

- 2020-01-08

- 2019-07-20

- 2020-02-29

- 2019-07-20

- 2020-01-08

- 2020-02-29

- 2020-02-29

- 2019-07-20

- 2020-01-08

- 2020-09-04

- 2020-02-29

- 2020-01-02

- 2019-07-20

- 2021-08-12

- 2020-01-08

- 2019-07-20