2021年6月acca考试时间是什么时候?有什么要求?

发布时间:2021-05-06

2021年6月acca的考试时间是什么时候?有什么具体要求?下面就给大家分享一下有关内容。

官方通知2021年第二次acca考试将于6月举行,具体考试时间如下:

2021年6月7日-11日

一.acca考试必备物品

1.考前必带证件:身份证、准考证;

2.考试必备文具:黑色圆珠笔、小尺、铅笔、橡皮(以上笔试需带)、计算器(单功能)、手表等,另外由于考试时间较长,考生还可以准备一瓶撕掉包装的矿泉水。

二.acca考试规则

1、请考生尽量提前1小时到达考场,留足准备时间。

2、考生在到达考场后需进行签到,不可擅自离开考场。

3、任何与考试相关的材料都需存放在指定位置,不可带入考试座位。如在考试期间发现任何与考试相关的材料,将被视为违纪行为。

4、可接受的证件类型包括有效期内的护照、驾照、身份证或生物指纹卡(Biometric Residence Permit),过期证件、学生证等非国家官方发布的证件不属于有效证件。

6、考试开考前请将手机及其他电子产品关闭,包括闹钟及任何提示音,并放在指定位置,请勿随身携带。考试期间如果发现随身携带有手机或其他电子设备,都将被视为违规。

7、考试中可以使用不具备编程功能、无线通讯功能和文字存储功能的科学计算器,有其他额外功能的计算器不允许使用,监考老师有权暂时收走不符合要求的计算器。计算器请提前准备好,现场没有备用计算器提供,考试期间也不可以互相借用。入场后请根据监考人员的指示,按照座位上的号码对号入座,并将身份证件和准考证放在桌角,以便监考人员的进行二次核对。

8、考生入座后请勿随意触碰键盘鼠标等考试物品,以免影响考试正常开始。

9、考试开始后,监考人员会给每位考生发放一张草稿纸,考试结束后会统一收回。如果草稿纸不够,应举手向监考人员申请。请勿在草稿纸以外的区域书写,比如在准考证或者其他纸张上打草稿。

(补充)迟到规定:

在开考后 1 小时内(上午 10:00 前,下午 14:30 前,晚上 19:00 前)到达的考生可以入场,但不能补偿考试时间。开考 1 小时以后到达的考生不能进入考场。

10、考试开始后不可提前离开考场。

以上就是今天分享的全部内容了,希望能够对大家有所帮助,如需了解更多acca的信息,请继续关注51题库考试学习网!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

2 Tyre, a public limited company, operates in the vehicle retailing sector. The company is currently preparing its financial

statements for the year ended 31 May 2006 and has asked for advice on how to deal with the following items:

(i) Tyre requires customers to pay a deposit of 20% of the purchase price when placing an order for a vehicle. If the

customer cancels the order, the deposit is not refundable and Tyre retains it. If the order cannot be fulfilled by

Tyre, the company repays the full amount of the deposit to the customer. The balance of the purchase price

becomes payable on the delivery of the vehicle when the title to the goods passes. Tyre proposes to recognise

the revenue from the deposits immediately and the balance of the purchase price when the goods are delivered

to the customer. The cost of sales for the vehicle is recognised when the balance of the purchase price is paid.

Additionally, Tyre had sold a fleet of cars to Hub and gave Hub a discount of 30% of the retail price on the

transaction. The discount given is normal for this type of transaction. Tyre has given Hub a buyback option which

entitles Hub to require Tyre to repurchase the vehicles after three years for 40% of the purchase price. The normal

economic life of the vehicles is five years and the buyback option is expected to be exercised. (8 marks)

Required:

Advise the directors of Tyre on how to treat the above items in the financial statements for the year ended

31 May 2006.

(The mark allocation is shown against each of the above items)

2 Advice on sundry accounting issues: year ended 31 May 2006

The following details the nature of the advice relevant to the accounting issues.

Revenue recognition

(i) Sale to customers

IAS18 ‘Revenue’ requires that revenue relating to the sale of goods is recognised when the significant risks and rewards are

transferred to the buyer. Also the company should not retain any continuing managerial involvement associated with

ownership or control of the goods. Additionally the revenue and costs must be capable of reliable measurement and it should

be probable that the economic benefits of the transaction will go to the company.

Although the deposit is non refundable on cancellation of the order by the customer, there is a valid expectation that the

deposit will be repaid where the company does not fulfil its contractual obligation in supplying the vehicle. The deposit should,

therefore, only be recognised in revenue when the vehicle has been delivered and accepted by the customer. It should be

treated as a liability up to this point. At this point also, the balance of the sale proceeds will be recognised. If the customer

does cancel the order, then the deposit would be recognised in revenue at the date of the cancellation of the order.

The appendix to IAS18, although not part of the standard, agrees that revenue is recognised when goods of this nature are

delivered to the buyer.

Sale of Fleet cars

The company has not transferred the significant risks and rewards of ownership as required by IAS18 as the buyback option

is expected to occur. The reason for this conclusion is that the company has retained the risk associated with the residual

value of the vehicles. Therefore, the transaction should not be treated as a sale. The vehicles should be treated as an operating

lease as essentially only 60% of the purchase price will be received by Tyre. Ownership of the assets are not expected to be

transferred to Hub, the lease term is arguably not for the major part of the assets’ life, and the present value of the minimum

lease payments will not be substantially equivalent to the fair value of the asset. Therefore it is an operating lease (IAS17).

No ‘outright sale profit’ will be recognised as the risks and rewards of ownership have been retained and no sale has occurred.

The vehicles will be shown in property, plant and equipment at their carrying amount. The lease income should be recognised

on a straight line basis over the lease term of three years unless some other basis is more representative. The vehicles will

be depreciated in accordance with IAS16, ‘Property, Plant and Equipment’. If there is any indication of impairment then the

company will apply IAS36 ‘Impairment of Assets’. As the discount given is normal for this type of transaction, it will not be

taken into account in estimating the fair value of the assets.

The buyback option will probably meet the definition of a financial liability and will be accounted for under IAS39 ‘Financial

Instruments: recognition and measurement’. The liability should be measured at ‘fair value’ and subsequently at amortisedcost unless designated at the outset as being at fair value through profit or loss.

(ii) the recent financial performance of Merton plc from a shareholder perspective. Clearly identify any

issues that you consider should be brought to the attention of the ordinary shareholders. (15 marks)

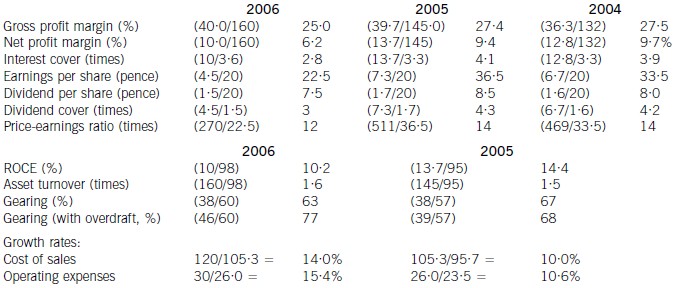

(ii) Discussion of financial performance

It is clear that 2006 has been a difficult year for Merton plc. There are very few areas of interest to shareholders where

anything positive can be found to say.

Profitability

Return on capital employed has declined from 14·4% in 2005, which compared favourably with the sector average of

12%, to 10·2% in 2006. Since asset turnover has improved from 1·5 to 1·6 in the same period, the cause of the decline

is falling profitability. Gross profit margin has fallen each year from 27·5% in 2004 to 25% in 2006, equal to the sector

average, despite an overall increase in turnover during the period of 10% per year. Merton plc has been unable to keep

cost of sales increases (14% in 2006 and 10% in 2005) below the increases in turnover. Net profit margin has declined

over the same period from 9·7% to 6·2%, compared to the sector average of 8%, because of substantial increases in

operating expenses (15·4% in 2006 and 10·6% in 2005). There is a pressing need here for Merton plc to bring cost

of sales and operating costs under control in order to improve profitability.

Gearing and financial risk

Gearing as measured by debt/equity has fallen from 67% (2005) to 63% (2006) because of an increase in

shareholders’ funds through retained profits. Over the same period the overdraft has increased from £1m to £8m and

cash balances have fallen from £16m to £1m. This is a net movement of £22m. If the overdraft is included, gearing

has increased to 77% rather than falling to 63%.

None of these gearing levels compare favourably with the average gearing for the sector of 50%. If we consider the large

increase in the overdraft, financial risk has clearly increased during the period. This is also evidenced by the decline in

interest cover from 4·1 (2005) to 2·8 (2006) as operating profit has fallen and interest paid has increased. In each year

interest cover has been below the sector average of eight and the current level of 2·8 is dangerously low.

Share price

As the return required by equity investors increases with increasing financial risk, continued increases in the overdraft

will exert downward pressure on the company’s share price and further reductions may be expected.

Investor ratios

Earnings per share, dividend per share and dividend cover have all declined from 2005 to 2006. The cut in the dividend

per share from 8·5 pence per share to 7·5 pence per share is especially worrying. Although in its announcement the

company claimed that dividend growth and share price growth was expected, it could have chosen to maintain the

dividend, if it felt that the current poor performance was only temporary. By cutting the dividend it could be signalling

that it expects the poor performance to continue. Shareholders have no guarantee as to the level of future dividends.

This view could be shared by the market, which might explain why the price-earnings ratio has fallen from 14 times to

12 times.

Financing strategy

Merton plc has experienced an increase in fixed assets over the last period of £10m and an increase in stocks and

debtors of £21m. These increases have been financed by a decline in cash (£15m), an increase in the overdraft (£7m)

and an increase in trade credit (£6m). The company is following an aggressive strategy of financing long-term

investment from short-term sources. This is very risky, since if the overdraft needed to be repaid, the company would

have great difficulty in raising the funds required.

A further financing issue relates to redemption of the existing debentures. The 10% debentures are due to be redeemed

in two years’ time and Merton plc will need to find £13m in order to do this. It does not appear that this sum can be

raised internally. While it is possible that refinancing with debt paying a lower rate of interest may be possible, the low

level of interest cover may cause concern to potential providers of debt finance, resulting in a higher rate of interest. The

Finance Director of Merton plc needs to consider the redemption problem now, as thought is currently being given to

raising a substantial amount of new equity finance. This financing choice may not be available again in the near future,

forcing the company to look to debt finance as a way of effecting redemption.

Overtrading

The evidence produced by the financial analysis above is that Merton plc is showing some symptoms of overtrading

(undercapitalisation). The board are suggesting a rights issue as a way of financing an expansion of business, but it is

possible that a rights issue will be needed to deal with the overtrading problem. This is a further financing issue requiring

consideration in addition to the redemption of debentures mentioned earlier.

Conclusion

Ordinary shareholders need to be aware of the following issues.

1. Profitability has fallen over the last year due to poor cost control

2. A substantial increase in the overdraft over the last year has caused gearing to increase

3. It is possible that the share price will continue to fall

4. The dividend cut may warn of continuing poor performance in the future

5. A total of £13m of debentures need redeeming in two year’s time

6. A large amount of new finance is needed for working capital and debenture redemption

Appendix: Analysis of key ratios and financial information

(b) You are the audit manager of Johnston Co, a private company. The draft consolidated financial statements for

the year ended 31 March 2006 show profit before taxation of $10·5 million (2005 – $9·4 million) and total

assets of $55·2 million (2005 – $50·7 million).

Your firm was appointed auditor of Tiltman Co when Johnston Co acquired all the shares of Tiltman Co in March

2006. Tiltman’s draft financial statements for the year ended 31 March 2006 show profit before taxation of

$0·7 million (2005 – $1·7 million) and total assets of $16·1 million (2005 – $16·6 million). The auditor’s

report on the financial statements for the year ended 31 March 2005 was unmodified.

You are currently reviewing two matters that have been left for your attention on the audit working paper files for

the year ended 31 March 2006:

(i) In December 2004 Tiltman installed a new computer system that properly quantified an overvaluation of

inventory amounting to $2·7 million. This is being written off over three years.

(ii) In May 2006, Tiltman’s head office was relocated to Johnston’s premises as part of a restructuring.

Provisions for the resulting redundancies and non-cancellable lease payments amounting to $2·3 million

have been made in the financial statements of Tiltman for the year ended 31 March 2006.

Required:

Identify and comment on the implications of these two matters for your auditor’s reports on the financial

statements of Johnston Co and Tiltman Co for the year ended 31 March 2006. (10 marks)

(b) Tiltman Co

Tiltman’s total assets at 31 March 2006 represent 29% (16·1/55·2 × 100) of Johnston’s total assets. The subsidiary is

therefore material to Johnston’s consolidated financial statements.

Tutorial note: Tiltman’s profit for the year is not relevant as the acquisition took place just before the year end and will

therefore have no impact on the consolidated income statement. Calculations of the effect on consolidated profit before

taxation are therefore inappropriate and will not be awarded marks.

(i) Inventory overvaluation

This should have been written off to the income statement in the year to 31 March 2005 and not spread over three

years (contrary to IAS 2 ‘Inventories’).

At 31 March 2006 inventory is overvalued by $0·9m. This represents all Tiltmans’s profit for the year and 5·6% of

total assets and is material. At 31 March 2005 inventory was materially overvalued by $1·8m ($1·7m reported profit

should have been a $0·1m loss).

Tutorial note: 1/3 of the overvaluation was written off in the prior period (i.e. year to 31 March 2005) instead of $2·7m.

That the prior period’s auditor’s report was unmodified means that the previous auditor concurred with an incorrect

accounting treatment (or otherwise gave an inappropriate audit opinion).

As the matter is material a prior period adjustment is required (IAS 8 ‘Accounting Policies, Changes in Accounting

Estimates and Errors’). $1·8m should be written off against opening reserves (i.e. restated as at 1 April 2005).

(ii) Restructuring provision

$2·3m expense has been charged to Tiltman’s profit and loss in arriving at a draft profit of $0·7m. This is very material.

(The provision represents 14·3% of Tiltman’s total assets and is material to the balance sheet date also.)

The provision for redundancies and onerous contracts should not have been made for the year ended 31 March 2006

unless there was a constructive obligation at the balance sheet date (IAS 37 ‘Provisions, Contingent Liabilities and

Contingent Assets’). So, unless the main features of the restructuring plan had been announced to those affected (i.e.

redundancy notifications issued to employees), the provision should be reversed. However, it should then be disclosed

as a non-adjusting post balance sheet event (IAS 10 ‘Events After the Balance Sheet Date’).

Given the short time (less than one month) between acquisition and the balance sheet it is very possible that a

constructive obligation does not arise at the balance sheet date. The relocation in May was only part of a restructuring

(and could be the first evidence that Johnston’s management has started to implement a restructuring plan).

There is a risk that goodwill on consolidation of Tiltman may be overstated in Johnston’s consolidated financial

statements. To avoid the $2·3 expense having a significant effect on post-acquisition profit (which may be negligible

due to the short time between acquisition and year end), Johnston may have recognised it as a liability in the

determination of goodwill on acquisition.

However, the execution of Tiltman’s restructuring plan, though made for the year ended 31 March 2006, was conditional

upon its acquisition by Johnston. It does not therefore represent, immediately before the business combination, a

present obligation of Johnston. Nor is it a contingent liability of Johnston immediately before the combination. Therefore

Johnston cannot recognise a liability for Tiltman’s restructuring plans as part of allocating the cost of the combination

(IFRS 3 ‘Business Combinations’).

Tiltman’s auditor’s report

The following adjustments are required to the financial statements:

■ restructuring provision, $2·3m, eliminated;

■ adequate disclosure of relocation as a non-adjusting post balance sheet event;

■ current period inventory written down by $0·9m;

■ prior period inventory (and reserves) written down by $1·8m.

Profit for the year to 31 March 2006 should be $3·9m ($0·7 + $0·9 + $2·3).

If all these adjustments are made the auditor’s report should be unmodified. Otherwise, the auditor’s report should be

qualified ‘except for’ on grounds of disagreement. If none of the adjustments are made, the qualification should still be

‘except for’ as the matters are not pervasive.

Johnston’s auditor’s report

If Tiltman’s auditor’s report is unmodified (because the required adjustments are made) the auditor’s report of Johnston

should be similarly unmodified. As Tiltman is wholly-owned by Johnston there should be no problem getting the

adjustments made.

If no adjustments were made in Tiltman’s financial statements, adjustments could be made on consolidation, if

necessary, to avoid modification of the auditor’s report on Johnston’s financial statements.

The effect of these adjustments on Tiltman’s net assets is an increase of $1·4m. Goodwill arising on consolidation (if

any) would be reduced by $1·4m. The reduction in consolidated total assets required ($0·9m + $1·4m) is therefore

the same as the reduction in consolidated total liabilities (i.e. $2·3m). $2·3m is material (4·2% consolidated total

assets). If Tiltman’s financial statements are not adjusted and no adjustments are made on consolidation, the

consolidated financial position (balance sheet) should be qualified ‘except for’. The results of operations (i.e. profit for

the period) should be unqualified (if permitted in the jurisdiction in which Johnston reports).

Adjustment in respect of the inventory valuation may not be required as Johnston should have consolidated inventory

at fair value on acquisition. In this case, consolidated total liabilities should be reduced by $2·3m and goodwill arising

on consolidation (if any) reduced by $2·3m.

Tutorial note: The effect of any possible goodwill impairment has been ignored as the subsidiary has only just been

acquired and the balance sheet date is very close to the date of acquisition.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-04-16

- 2020-01-09

- 2020-01-10

- 2020-01-09

- 2020-01-10

- 2020-10-08

- 2020-01-10

- 2021-04-23

- 2020-03-14

- 2020-01-10

- 2020-01-08

- 2020-01-09

- 2020-03-08

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-09

- 2020-03-05

- 2020-03-12

- 2020-03-15

- 2020-04-29

- 2020-03-11

- 2020-01-09

- 2020-01-10

- 2020-05-09

- 2020-01-10

- 2020-02-28

- 2020-01-10

- 2020-03-08