湖北省考生:如何利用零散时间学习ACCA?

发布时间:2020-01-10

在我国职称会计师考试中,ACCA考试属于难度比较大的考试,由于严苛的报考条件,备考ACCA考试的朋友大多数都是工作比较忙碌的上班族,那么如何在繁忙的工作中合理安排备考时间对于考生来说就非常重要了。除去完整系统的备考时间外,生活中零散时间也是能够备考的,今天就来教大家如何高效利用零散时间学习ACCA考试,大家可以作为参考。

每天至少一道题

ACCA考试的类型有很多种,主要考察应试人员分析、解决财务工作的能力,同时对计算能力和语言能力也是极大的挑战。所以在平时的备考中是一定缺少不了习题的辅助的。建议大家每天至少要做一套ACCA真题训练,每道小问控制在8分钟左右,这就足够大家利用空闲时间进行做题。

生活空档看考点

在上班路上看新闻时间,午休后的看剧时间在备考期间大家都可以转换成“高会学习时间”,带上《轻松过关》辅导书,看里面的“考点精讲”,让你在短时间内了解学习内容。你可以选择将学过的知识点复习一遍,或者将要学习的知识点提前预习一遍,要知道只有多一份努力才能多一份胜算。

备考笔记随身带

很多考生在备考中有记笔记或者是记错题本的好习惯,将整理的内容随身携带,空闲时间可以随时拿出来进行学习也是不错的选择。选择自己整理的笔记可以加深学习的印象,在考试的过程中也能当成考试资料带入考场,寻找知识点也会更快。

用完整时间来学习,用零散时间来备考,两者结合高效备考!

以上就是为大家准备的备考方法,希望对大家有所帮助,预祝大家都能轻松过ACCA考试~加油~

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(ii) consignment inventory; and (3 marks)

(ii) Consignment inventory

■ Agree terms of sale to dealers to confirm the ‘principal – agent’ relationship between Pavia and dealers.

■ Inspect proforma invoices for vehicles sent on consignment to dealers to confirm number of vehicles with dealers

at the year end.

■ Obtain direct confirmation from dealers of vehicles unsold at the year end.

■ Physically inspect vehicles sold on consignment before the year end that are returned unsold by dealers after the

year end (if any) for evidence of impairment.

■ Perform. cutoff tests on sales to dealers/trade receivables/vehicle inventory.

■ If goods on consignment are treated as inventory agree their unit costs to be the same as for other vehicles in

inventory.

(c) Explain the capital gains tax (CGT) and income tax (IT) issues Paul and Sharon should consider in deciding

which form. of trust to set up for Gisella and Gavin. You are not required to consider inheritance tax (IHT) or

stamp duty land tax (SDLT) issues. (10 marks)

You should assume that the tax rates and allowances for the tax year 2005/06 apply throughout this question.

(c) As the trust is created in the settlors’ (Paul and Sharon’s) lifetime its creation will constitute a chargeable disposal for capital

gains tax. Also, as the settlors and trustees are connected persons, the disposal will be deemed to be at market value, resulting

in a chargeable gain of £80,000 (160,000 – 80,000). No taper relief will be available as the property is a non-business

asset, and has been held for less than three years, but annual exemptions of £17,000 (2 x £8,500) will be available.

However, in the case of a discretionary trust, gift hold over relief will be available. This is because the gift will constitute a

chargeable lifetime transfer and because there is an immediate charge to inheritance tax (even though no tax is payable due

to the nil rate band) relief is available if a specific accumulation and maintenance trust is used, as in this case the gift will

qualify as a potentially exempt transfer and so gift relief would only be available in respect of business assets. The use of a

basic discretionary trust will thus facilitate the deferral of an immediate capital gains tax charge of £25,200 (63,000 x 40%).

If/when the property is disposed of, however, the trustees will pay capital gains tax on the deferred gain at the trust income

tax rate of 40%, and have an annual exemption of only £4,250 (50% of the normal individual rate) available to them. The

40% rate of tax and lower annual exemption rate also apply to chargeable gains arising in a specific accumulation and

maintenance trust, as well as a basic discretionary trust.

A chargeable disposal between connected persons will also arise for the purposes of capital gains tax if/when the property

vests in a beneficiary, i.e. one or more of the beneficiaries becomes absolutely entitled to all or part of the income or capital

of the trust. Gift hold over relief will again be available on all assets in the case of a discretionary trust, but only on business

assets in the case of an accumulation and maintenance trust, except where a beneficiary becomes entitled to both income

and capital at the same time.

The trust will have taxable property income in the form. of net rents from its creation and in future years is also likely to have

other investment income, probably in the form. of interest, to the extent that monies are retained in the trust. Whichever form

of trust is used, the trustees will pay tax at the standard trust rate of 40% on income other than dividend income (32·5%),

except to the extent of (1) the first £500 of taxable income, which is taxed at the rate that would otherwise apply to such

income (i.e. 22% for non-savings (rental) income, 20% for savings income (interest) and 10% for dividends) but, only to the

extent that it is not distributed; and (2) the legitimate trust management expenses, which are offsettable for the purposes of

the higher trust tax rates against the income with the lowest rate(s) of normal tax and so bear tax only at that rate. The higher

trust tax rate always applies to income that is distributed, other than to the extent that it has been treated as the settlor’s

income, and taxed at that settlor’s marginal tax rate.

As Paul and Sharon intend to create a trust for their unmarried minor (under 18) children, then even if the trust specifically

excludes them from any benefit under the trust, the trust income will be treated as theirs for income tax purposes to the extent

that it constitutes income paid for on behalf (including maintenance payments) of Gisella and Gavin; except where (1) the

total income arising does not exceed £100 gross per annum, and (2) income is held for the benefit of a child under an

accumulation and maintenance settlement, to the extent that it is not paid out.

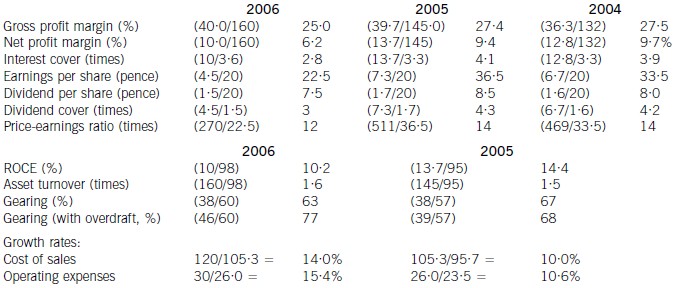

(ii) the recent financial performance of Merton plc from a shareholder perspective. Clearly identify any

issues that you consider should be brought to the attention of the ordinary shareholders. (15 marks)

(ii) Discussion of financial performance

It is clear that 2006 has been a difficult year for Merton plc. There are very few areas of interest to shareholders where

anything positive can be found to say.

Profitability

Return on capital employed has declined from 14·4% in 2005, which compared favourably with the sector average of

12%, to 10·2% in 2006. Since asset turnover has improved from 1·5 to 1·6 in the same period, the cause of the decline

is falling profitability. Gross profit margin has fallen each year from 27·5% in 2004 to 25% in 2006, equal to the sector

average, despite an overall increase in turnover during the period of 10% per year. Merton plc has been unable to keep

cost of sales increases (14% in 2006 and 10% in 2005) below the increases in turnover. Net profit margin has declined

over the same period from 9·7% to 6·2%, compared to the sector average of 8%, because of substantial increases in

operating expenses (15·4% in 2006 and 10·6% in 2005). There is a pressing need here for Merton plc to bring cost

of sales and operating costs under control in order to improve profitability.

Gearing and financial risk

Gearing as measured by debt/equity has fallen from 67% (2005) to 63% (2006) because of an increase in

shareholders’ funds through retained profits. Over the same period the overdraft has increased from £1m to £8m and

cash balances have fallen from £16m to £1m. This is a net movement of £22m. If the overdraft is included, gearing

has increased to 77% rather than falling to 63%.

None of these gearing levels compare favourably with the average gearing for the sector of 50%. If we consider the large

increase in the overdraft, financial risk has clearly increased during the period. This is also evidenced by the decline in

interest cover from 4·1 (2005) to 2·8 (2006) as operating profit has fallen and interest paid has increased. In each year

interest cover has been below the sector average of eight and the current level of 2·8 is dangerously low.

Share price

As the return required by equity investors increases with increasing financial risk, continued increases in the overdraft

will exert downward pressure on the company’s share price and further reductions may be expected.

Investor ratios

Earnings per share, dividend per share and dividend cover have all declined from 2005 to 2006. The cut in the dividend

per share from 8·5 pence per share to 7·5 pence per share is especially worrying. Although in its announcement the

company claimed that dividend growth and share price growth was expected, it could have chosen to maintain the

dividend, if it felt that the current poor performance was only temporary. By cutting the dividend it could be signalling

that it expects the poor performance to continue. Shareholders have no guarantee as to the level of future dividends.

This view could be shared by the market, which might explain why the price-earnings ratio has fallen from 14 times to

12 times.

Financing strategy

Merton plc has experienced an increase in fixed assets over the last period of £10m and an increase in stocks and

debtors of £21m. These increases have been financed by a decline in cash (£15m), an increase in the overdraft (£7m)

and an increase in trade credit (£6m). The company is following an aggressive strategy of financing long-term

investment from short-term sources. This is very risky, since if the overdraft needed to be repaid, the company would

have great difficulty in raising the funds required.

A further financing issue relates to redemption of the existing debentures. The 10% debentures are due to be redeemed

in two years’ time and Merton plc will need to find £13m in order to do this. It does not appear that this sum can be

raised internally. While it is possible that refinancing with debt paying a lower rate of interest may be possible, the low

level of interest cover may cause concern to potential providers of debt finance, resulting in a higher rate of interest. The

Finance Director of Merton plc needs to consider the redemption problem now, as thought is currently being given to

raising a substantial amount of new equity finance. This financing choice may not be available again in the near future,

forcing the company to look to debt finance as a way of effecting redemption.

Overtrading

The evidence produced by the financial analysis above is that Merton plc is showing some symptoms of overtrading

(undercapitalisation). The board are suggesting a rights issue as a way of financing an expansion of business, but it is

possible that a rights issue will be needed to deal with the overtrading problem. This is a further financing issue requiring

consideration in addition to the redemption of debentures mentioned earlier.

Conclusion

Ordinary shareholders need to be aware of the following issues.

1. Profitability has fallen over the last year due to poor cost control

2. A substantial increase in the overdraft over the last year has caused gearing to increase

3. It is possible that the share price will continue to fall

4. The dividend cut may warn of continuing poor performance in the future

5. A total of £13m of debentures need redeeming in two year’s time

6. A large amount of new finance is needed for working capital and debenture redemption

Appendix: Analysis of key ratios and financial information

(b) Explain what effect the acquisition of Di Rollo Co will have on the planning of your audit of the consolidated

financial statements of Murray Co for the year ending 31 March 2008. (10 marks)

(b) Effect of acquisition on planning the audit of Murray’s consolidated financial statements for the year ending 31 March

2008

Group structure

The new group structure must be ascertained to identify all entities that should be consolidated into the Murray group’s

financial statements for the year ending 31 March 2008.

Materiality assessment

Preliminary materiality for the group will be much higher, in monetary terms, than in the prior year. For example, if a % of

total assets is a determinant of the preliminary materiality, it may be increased by 10% (as the fair value of assets acquired,

including goodwill, is $2,373,000 compared with $21·5m in Murray’s consolidated financial statements for the year ended

31 March 2007).

The materiality of each subsidiary should be re-assessed, in terms of the enlarged group as at the planning stage. For

example, any subsidiary that was just material for the year ended 31 March 2007 may no longer be material to the group.

This assessment will identify, for example:

– those entities requiring an audit visit; and

– those entities for which substantive analytical procedures may suffice.

As Di Rollo’s assets are material to the group Ross should plan to inspect the South American operations. The visit may

include a meeting with Di Rollo’s previous auditors to discuss any problems that might affect the balances at acquisition and

a review of the prior year audit working papers, with their permission.

Di Rollo was acquired two months into the financial year therefore its post-acquisition results should be expected to be

material to the consolidated income statement.

Goodwill acquired

The assets and liabilities of Di Rollo at 31 March 2008 will be combined on a line-by-line basis into the consolidated financial

statements of Murray and goodwill arising on acquisition recognised.

Audit work on the fair value of the Di Rollo brand name at acquisition, $600,000, may include a review of a brand valuation

specialist’s working papers and an assessment of the reasonableness of assumptions made.

Significant items of plant are likely to have been independently valued prior to the acquisition. It may be appropriate to plan

to place reliance on the work of expert valuers. The fair value adjustment on plant and equipment is very high (441% of

carrying amount at the date of acquisition). This may suggest that Di Rollo’s depreciation policies are over-prudent (e.g. if

accelerated depreciation allowed for tax purposes is accounted for under local GAAP).

As the amount of goodwill is very material (approximately 50% of the cash consideration) it may be overstated if Murray has

failed to recognise any assets acquired in the purchase of Di Rollo in accordance with IFRS 3 Business Combinations. For

example, Murray may have acquired intangible assets such as customer lists or franchises that should be recognised

separately from goodwill and amortised (rather than tested for impairment).

Subsequent impairment

The audit plan should draw attention to the need to consider whether the Di Rollo brand name and goodwill arising have

suffered impairment as a result of the allegations against Di Rollo’s former chief executive.

Liabilities

Proceedings in the legal claim made by Di Rollo’s former chief executive will need to be reviewed. If the case is not resolved

at 31 March 2008, a contingent liability may require disclosure in the consolidated financial statements, depending on the

materiality of amounts involved. Legal opinion on the likelihood of Di Rollo successfully defending the claim may be sought.

Provision should be made for any actual liabilities, such as legal fees.

Group (related party) transactions and balances

A list of all the companies in the group (including any associates) should be included in group audit instructions to ensure

that intra-group transactions and balances (and any unrealised profits and losses on transactions with associates) are

identified for elimination on consolidation. Any transfer pricing policies (e.g. for clothes manufactured by Di Rollo for Murray

and sales of Di Rollo’s accessories to Murray’s retail stores) must be ascertained and any provisions for unrealised profit

eliminated on consolidation.

It should be confirmed at the planning stage that inter-company transactions are identified as such in the accounting systems

of all companies and that inter-company balances are regularly reconciled. (Problems are likely to arise if new inter-company

balances are not identified/reconciled. In particular, exchange differences are to be expected.)

Other auditors

If Ross plans to use the work of other auditors in South America (rather than send its own staff to undertake the audit of Di

Rollo), group instructions will need to be sent containing:

– proforma statements;

– a list of group and associated companies;

– a statement of group accounting policies (see below);

– the timetable for the preparation of the group accounts (see below);

– a request for copies of management letters;

– an audit work summary questionnaire or checklist;

– contact details (of senior members of Ross’s audit team).

Accounting policies

Di Rollo may have material accounting policies which do not comply with the rest of the Murray group. As auditor to Di Rollo,

Ross will be able to recalculate the effect of any non-compliance with a group accounting policy (that Murray’s management

would be adjusting on consolidation).

Timetable

The timetable for the preparation of Murray’s consolidated financial statements should be agreed with management as soon

as possible. Key dates should be planned for:

– agreement of inter-company balances and transactions;

– submission of proforma statements;

– completion of the consolidation package;

– tax review of group accounts;

– completion of audit fieldwork by other auditors;

– subsequent events review;

– final clearance on accounts of subsidiaries;

– Ross’s final clearance of consolidated financial statements.

Tutorial note: The order of dates is illustrative rather than prescriptive.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-03-08

- 2020-01-01

- 2020-01-10

- 2020-01-14

- 2020-04-20

- 2020-03-25

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-05-21

- 2020-01-10

- 2020-02-20

- 2020-05-13

- 2020-02-20

- 2020-01-10

- 2020-04-11

- 2020-01-09

- 2020-01-10

- 2020-04-21

- 2020-01-10

- 2020-03-11

- 2020-01-10

- 2020-01-10

- 2020-05-06

- 2020-01-10

- 2020-05-17

- 2020-01-10

- 2021-04-17

- 2020-01-10

- 2020-05-03