备考ACCA的七大禁忌,请注意避开!

发布时间:2020-05-16

学习ACCA不是一件容易的事情,有时候会有很多因素会让自己陷入误区,使自己多走弯路,甚至于半途而废。小伙伴们在备考时一定要注意避开这几个雷区。

一、迷惑

没有为以后几天,几个月和以后几年作出计划可能是时间管理中最大的错误。解决困惑的最后办法就是设置目标并且不时对这些目标进行评估。这里有几个基本思想:

1、建立清楚的、可以达到的目标。

2、确立目标的优先权。

3、找出与目标有关的可以在较短时间内进行的工作。

4、确定完成较小目标的日期。

ACCA备考设立的目标一般都是中短期的目标,通常都是应该把它们分为更加实际的任务。每周都应该树立可以达到的具体的目标。同时每天睡觉前都要列出第二天的学习清单。

二、犹豫不决

犹豫不决让大家无法集中精力,无法放松,无法创造。它还可能成为其他问题的根源,如逃避责任。为了有效的管理时间,应该根据价值来投入时间,把时间投入到有较大意义的目标中去。

三、精力分散

精神和体力的超负荷精力分散是企图做超出需要的甚至超出可能的事情,过多的精力分散会引出无效的问题解决,无法集中精力,对最简单的工作也缺乏动机。企图在各方面都做工作就会使身体产生疲劳。ACCA有13个科目,考试战线比较长,是一个浩大的工程,这个工程需要一个总体的时间规划,这规划一定要尽量做细。把每一科的任务都分为几个阶段,把每一科的任务都细化到周。

四、拖延等到明天

拖延是时间的窃贼,是时间管理中的最重的罪恶。拖延的定义是把某一时间能够做好的事情拖到以后。虽然说计划赶不上变化,在具体的ACCA备考过程中会遇到很多情况,这些情况可能会延误你的复习进度。出现这种情况,一定要想方设法把进度追上。

五、逃避

小伙伴们可以找到很多逃避复习和学习的方法,大家会遇到一些和学习无关的事情,如同学过生日、院系组织的一些活动、同学组织去唱歌等,遇到这种情况,一定要学会克制,既然选择了考ACCA,有的时候就需要放弃很多类似的活动。

六、计划中断

不在计划中的打断是让人烦恼的事情之一。中断对复杂的工作伤害最大。大家在备考中都有过类似的经验,一道难题好不容易有点眉目了,被人打扰再也想不起来了。在寝室里温书,接了几个电话,一上午就完了。

七、完美主义

笔记作得工工整整脏了一点,修来改去甚至重抄一遍。殊不知,这样做并不能给自己带来更多的效益。

好了,今天的分享就到这里了,不知道这篇文章是否有给大家带来帮助呢?想知道更多关于ACCA的资讯还请继续关注51题库考试学习网哦!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(ii) vehicles. (3 marks)

(ii) Vehicles

■ Agreeing opening ledger balances of cost and accumulated depreciation (and impairment losses) to the non-current

asset register to confirm the comparative amounts.

■ Physically inspecting a sample of vehicles (selected from the asset register) to confirm existence and condition (for

evidence of impairment). If analytical procedures use management information on mileage records this should be

checked (e.g. against milometers) at the same time.

■ Agreeing additions to purchase invoices to confirm cost.

■ Reviewing the terms of all lease contracts entered into during the year to ensure that finance leases have been

capitalised.

■ Agreeing the depreciation rates applied to finance lease assets to those applied to similar purchased assets.

■ Reviewing repairs and maintenance accounts (included in materials expense) to ensure that there are no material

items of capital nature that have been expensed (i.e. a test for completeness).

(b) Explain the need for a first time group auditor to analyse the group structure. (5 marks)

(b) Need to analyse the group structure

A certain amount of analysis of the group structure will be undertaken before an auditor accepts the role of group auditor,

particularly if the auditor is not directly responsible for the whole group.

An analysis of the group structure is necessary to:

■ ensure that particular attention is given to the more unusual aspects of corporate structures (e.g. partnership

arrangements that may be a joint venture, components in tax havens, shell companies and horizontal groups);

■ arrange access to information relating to all ‘significant’ components (i.e. those representing 20% or more of group

assets, liabilities, cash flows, profit or revenue), on a timely basis;

■ identify the applicable financial reporting framework for each component and any local statutory reporting requirements;

■ plan work to deal with different accounting frameworks/policies applied throughout the group and differences between

International Auditing Standards (ISAs) and national standards;

■ integrate the group audit process effectively with local statutory audit requirements;

■ identify related parties and effectively audit the completeness of disclosures in the group accounts in accordance with

IAS 24 Related Party Disclosures.

Any doubts about the group structure will need to be clarified against publicly available information as soon as possible to

ensure an effective audit of the relevant components (i.e. subsidiaries, associates and joint ventures). The auditor can then

plan the level of assurance required on each component well in advance of the year end.

Having established thoroughly the group structure from the outset the auditor will then need only to update the structure for

changes year-on-year.

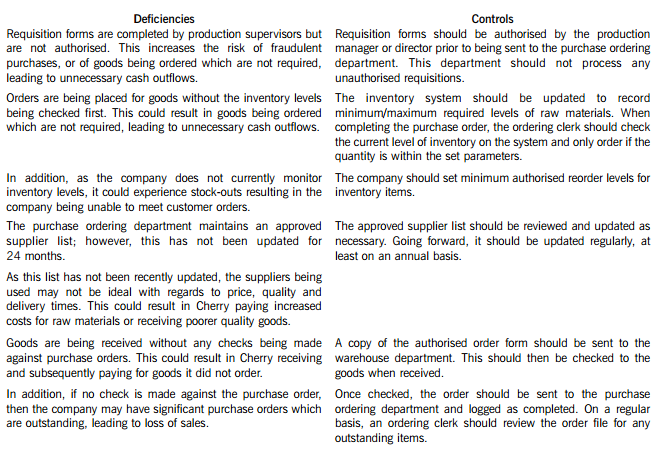

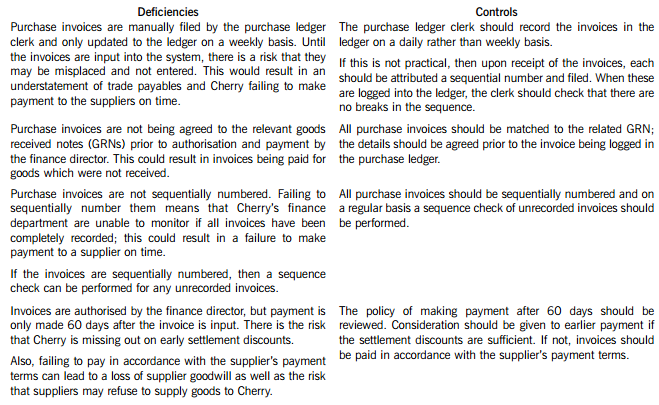

Cherry Blossom Co (Cherry) manufactures custom made furniture and its year end is 30 April. The company purchases its raw materials from a wide range of suppliers. Below is a description of Cherry’s purchasing system.

When production supervisors require raw materials, they complete a requisition form. and this is submitted to the purchase ordering department. Requisition forms do not require authorisation and no reference is made to the current inventory levels of the materials being requested. Staff in the purchase ordering department use the requisitions to raise sequentially numbered purchase orders based on the approved suppliers list, which was last updated 24 months ago. The purchasing director authorises the orders prior to these being sent to the suppliers.

When the goods are received, the warehouse department verifies the quantity to the suppliers despatch note and checks that the quality of the goods received are satisfactory. They complete a sequentially numbered goods received note (GRN) and send a copy of the GRN to the finance department.

Purchase invoices are sent directly to the purchase ledger clerk, who stores them in a manual file until the end of each week. He then inputs them into the purchase ledger using batch controls and gives each invoice a unique number based on the supplier code. The invoices are reviewed and authorised for payment by the finance director, but the actual payment is only made 60 days after the invoice is input into the system.

Required:

In respect of the purchasing system of Cherry Blossom Co:

(i) Identify and explain FIVE deficiencies; and

(ii) Recommend a control to address each of these deficiencies.

Note: The total marks will be split equally between each part.

Cherry Blossom Co’s (Cherry) purchasing system deficiencies and controls

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-29

- 2020-02-28

- 2020-01-14

- 2020-04-09

- 2020-01-10

- 2020-02-15

- 2021-06-19

- 2020-01-10

- 2020-03-08

- 2020-04-14

- 2020-01-10

- 2020-01-09

- 2020-05-08

- 2020-01-10

- 2020-04-29

- 2020-01-10

- 2020-04-18

- 2020-03-08

- 2020-01-10

- 2020-04-11

- 2020-01-10

- 2020-01-10

- 2020-04-14

- 2020-01-10

- 2020-02-20

- 2020-01-27

- 2020-01-09

- 2020-02-02

- 2020-05-15

- 2020-04-29