ACCA 考试的内容有哪些?

发布时间:2021-03-12

ACCA 考试的内容有哪些?

最佳答案

考试内容:

F1会计师与企业 Accountant in Business (AB)

F2管理会计 Management Accounting (MA)

F3 财务会计 Financial Accounting (FA)

F4公司法与商法 Corporate and Business Law (CL)

F5业绩管理 Performance Management (PM)

F6税务 Taxation (TX)

F7/财务报告 Financial Reporting (FR)

F8/审计与认证业务Audit and Assurance (AA)

F9/财务管理 Financial Management (FM)

核心课程(共3门)

P1Professional Accounting 专业会计

P2 Corporate Reporting 公司报表

P3 Business Analysis 企业财务分析

选修课程(任选其中2门)

P4 Advanced Financial Management 高级财务管理

P5 Advanced Performance Management 高级业绩管理

P6 Advanced Taxation 高级税法

P7 Advanced Audit and Assurance 高级审计和认证

前三门是选择 后面的都是大题(大题有文字论述和计算题)

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

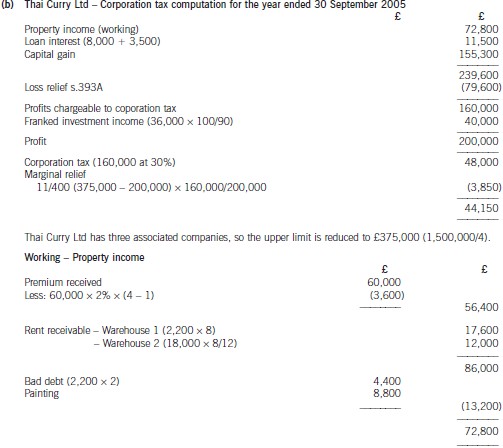

(b) Assuming that Thai Curry Ltd claims relief for its trading loss against total profits under s.393A ICTA 1988,calculate the company’s corporation tax liability for the year ended 30 September 2005. (10 marks)

21 Which of the following items must be disclosed in a company’s published financial statements?

1 Authorised share capital

2 Movements in reserves

3 Finance costs

4 Movements in non-current assets

A 1, 2 and 3 only

B 1, 2 and 4 only

C 2, 3 and 4 only

D All four items

(c) In August 2004 it was discovered that the inventory at 31 December 2003 had been overstated by $100,000.

(4 marks)

Required:

Advise the directors on the correct treatment of these matters, stating the relevant accounting standard which

justifies your answer in each case.

NOTE: The mark allocation is shown against each of the three matters.

(c) The opening inventory should be included in the current year’s income statement at the corrected figure, and the opening

balance of retained profit reduced by $100,000. The $100,000 reduction will appear in the statement of changes in equity.

(IAS8 Accounting policies, changes in accounting estimates and errors)

(ii) If a partner, who is an actuary, provides valuation services to an audit client, can we continue with the audit?

(3 marks)

Required:

For each of the three questions, explain the threats to objectivity that may arise and the safeguards that

should be available to manage them to an acceptable level.

NOTE: The mark allocation is shown against each of the three questions above.

(ii) Actuarial services to an audit client

IFAC’s ‘Code of Ethics for Professional Accountants’ does not deal specifically with actuarial valuation services but with

valuation services in general.

A valuation comprises:

■ making assumptions about the future;

■ applying certain methodologies and techniques;

■ computing a value (or range of values) for an asset, a liability or for a business as a whole.

A self-review threat may be created when a firm or network firm2 performs a valuation for a financial statement audit

client that is to be incorporated into the client’s financial statements.

As an actuarial valuation service is likely to involve the valuation of matters material to the financial statements (e.g. the

present value of obligations) and the valuation involves a significant degree of subjectivity (e.g. length of service), the

self-review threat created cannot be reduced to an acceptable level of the application of any safeguard. Accordingly:

■ such valuation services should not be provided; or

■ the firm should withdraw from the financial statement audit engagement.

If the net liability was not material to the financial statements the self-review threat may be reduced to an acceptable

level by the application of safeguards such as:

■ involving an additional professional accountant who was not a member of the audit team to review the work done

by the actuary;

■ confirming with the audit client their understanding of the underlying assumptions of the valuation and the

methodology to be used and obtaining approval for their use;

■ obtaining the audit client‘s acknowledgement of responsibility for the results of the work performed by the firm; and

■ making arrangements so that the partner providing the actuarial services does not participate in the audit

engagement.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2021-06-03

- 2021-03-10

- 2021-04-24

- 2021-06-28

- 2021-01-01

- 2021-12-31

- 2021-03-12

- 2021-06-23

- 2021-04-22

- 2021-04-24

- 2021-03-10

- 2021-03-10

- 2021-03-11

- 2021-03-11

- 2021-05-29

- 2021-03-12

- 2021-04-21

- 2021-04-15

- 2021-03-12

- 2021-05-13

- 2021-04-15

- 2021-12-16

- 2021-03-11

- 2021-05-08

- 2021-03-12

- 2021-05-22

- 2021-03-12

- 2021-03-12

- 2021-05-12

- 2021-03-11