2020年甘肃省7月ACCA考试成绩查询时间

发布时间:2020-08-12

考试结束后,大家最关心的莫过于考试成绩,那么2020年甘肃省7月ACCA考试成绩查询时间大家清楚吗?下面51题库考试学习网就带领大家一起来了解看看,关于2020年甘肃省ACCA考试成绩查询相关内容,感兴趣的小伙伴赶紧来围观吧。

根据官网消息,2020年7月ACCA考试成绩预计将于8月1日公布。

2020ACCA成绩查询方式与流程

ACCA成绩查询方式

1.电子邮件(e-mail)---您可在MYACCA内选择通过e-mail接收考试成绩。

2.短信通知---ACCA可采用短信通知考试成绩,但由于跨国服务较为复杂,可能不能接收短信。

3.网站查看考试成绩—在ACCA官网注册过的所有学生都能登录官网查看自己的成绩。

官网成绩查询的步骤:

1、登录

点击myACCA,输入学员账ID和密码,

2、点击exam entry,

查看自己的考试报名结果。

3、下载

确认好考试报名的信息后,一定要确认自己的身份信息,考试科目以及考试地点。点击“Download”j进行准考证的下载。

ACCA成绩查询结果显示:

到ACCA全球官方网站http://www.accaglobal.com/;点击Myacca登陆,点左面框架里的“EXAMS”进入页面,中间有一段:

EXAM STATUS REPORT Your status report

provides details of the ACCA exams you have already passed and those you have

still to complete

EXAM STATUS REPORT Your status report

provides details of the ACCA exams you have already passed and those you have

still to complete

View your status report————这个是超级链接,点进去就是你全部的考试分数记录了。

2020年ACCA成绩合格标准:

ACCA考试是百分制,50分为及格线。这意味着考生需要单科考试分数至少需要达到50分才算通过了考试。

成绩有效期:

ACCA 应用课程(F阶段)成绩有效期为无限期,战略课程(P阶段)成绩有效期为7年

ACCA考试期限跟CPA一样实行轮废制,即需要在一定的时间里面考完规定的科目,否则成绩将会无效。

时间计算:

根据以前的规则,学员必须在首次报名注册后10年内通过所有考试,否则将注销其学员资格。而后ACCA对时限做出了重要调整即:F段成绩永久有效,P段要在7年内考完。根据新规则,专业阶段考试的时限将为7年。因此,国际财会基础资格(Foundations in Accountancy,简称FIA)的考试以及ACCA资格考试的基础阶段F1-F9考试将不再有通过时限。

“7年政策”意味着从你通过P阶段的第一门科目开始,7年内需完成P阶段所要求的所有ACCA考试科目。否则,从第8年开始,你第1年所考过的P阶段科目成绩将会被视为过期作废,须重新考试。

另外,需要说明的是——此政策实行滚动式废除,也就是说不会在第8年时把你之前7年所有考过的P阶段科目成绩都废除,只会废除你第1年考过的P阶段科目成绩,第9年会废除你前2年所通过的P阶段科目成绩,以此类推。

以上是关于甘肃省2020年7月ACCA考试成绩查询相关内容,小伙伴们都了解了吗?如果大家对于ACCA考试还有别的问题,可以多多关注51题库考试学习网,我们将继续为大家答疑解惑!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(c) Discuss how the manipulation of financial statements by company accountants is inconsistent with their

responsibilities as members of the accounting profession setting out the distinguishing features of a

profession and the privileges that society gives to a profession. (Your answer should include reference to the

above scenario.) (7 marks)

Note: requirement (c) includes 2 marks for the quality of the discussion.

(c) Accounting and ethical implications of sale of inventory

Manipulation of financial statements often does not involve breaking laws but the purpose of financial statements is to present

a fair representation of the company’s position, and if the financial statements are misrepresented on purpose then this could

be deemed unethical. The financial statements in this case are being manipulated to show a certain outcome so that Hall

may be shown to be in a better financial position if the company is sold. The retained earnings of Hall will be increased by

$4 million, and the cash received would improve liquidity. Additionally this type of transaction was going to be carried out

again in the interim accounts if Hall was not sold. Accountants have the responsibility to issue financial statements that do

not mislead the public as the public assumes that such professionals are acting in an ethical capacity, thus giving the financial

statements credibility.

A profession is distinguished by having a:

(i) specialised body of knowledge

(ii) commitment to the social good

(iii) ability to regulate itself

(iv) high social status

Accountants should seek to promote or preserve the public interest. If the idea of a profession is to have any significance,

then it must make a bargain with society in which they promise conscientiously to serve the public interest. In return, society

allocates certain privileges. These might include one or more of the following:

– the right to engage in self-regulation

– the exclusive right to perform. particular functions

– special status

There is more to being an accountant than is captured by the definition of the professional. It can be argued that accountants

should have the presentation of truth, in a fair and accurate manner, as a goal.

(b) Peter, one of Linden Limited’s non-executive directors, having lived and worked in the UK for most of his adult

life, sold his home near London on 22 March 2006 and, together with his wife (a French citizen), moved to live

in a villa which she owns in the south of France. Peter is now demanding that the tax deducted from his director’s

fees, for the board meetings held on 18 April and 16 May 2006, be refunded, on the grounds that, as he is no

longer resident in the UK, he is no longer liable to UK income tax. All of the company’s board meetings are held

at its offices in Cambridge.

Despite Peter’s assurance that none of the other companies of which he is a director has disputed his change of

tax status, Damian is uncertain whether he should make the refunds requested. However, as Peter is a friend of

the company’s founder, Linden Limited’s managing director is urging him to do so, stating that if the tax does

have to be paid, then Linden Limited could always bear the cost.

Required:

Advise Damian whether Peter is correct in his assertion regarding his tax position and in the case that there

is a UK tax liability the implications of the managing director’s suggestion. You are not required to consider

national insurance (NIC) issues. (4 marks)

(b) Peter will have been resident and ordinarily resident in the UK. When such individuals leave the UK for a purpose other than

to take up full time employment abroad, they normally continue to still be so regarded unless their absence spans a complete

tax year. But, where someone intends to live permanently abroad or to do so for a period of at least three tax years, they may

be treated as non-resident and non-ordinarily resident from the day after the date of their departure, if they can provide

evidence to HMRC of that intention. Selling a residence in the UK and setting up home abroad will normally constitute such

evidence. However to retain non-resident status the intention must actually be fulfilled, and visits to the UK must not exceed

182 days in any tax year or average more than 90 days per year over a period of four tax years. Given that Peter would appear

to have several company directorships in the UK, it is possible that he might fail to satisfy the 90 day average ‘substantial

visits’ rule.

Even if Peter is classed as non-resident, any remuneration earned in the UK will still be liable to UK income tax, and subject

to PAYE, unless it is for duties incidental to an overseas employment, which is unlikely to be the case for fees paid to a nonexecutive

director for attending board meetings. Thus, income tax should still be deducted from the fees under PAYE. Where

PAYE should have been deducted from a director’s emoluments and it has not been, but the tax is nevertheless accounted

for by the company to HMRC, then to the extent that the tax is not reimbursed by the director, he will be treated as receiving

a benefit equivalent to the amount of tax.

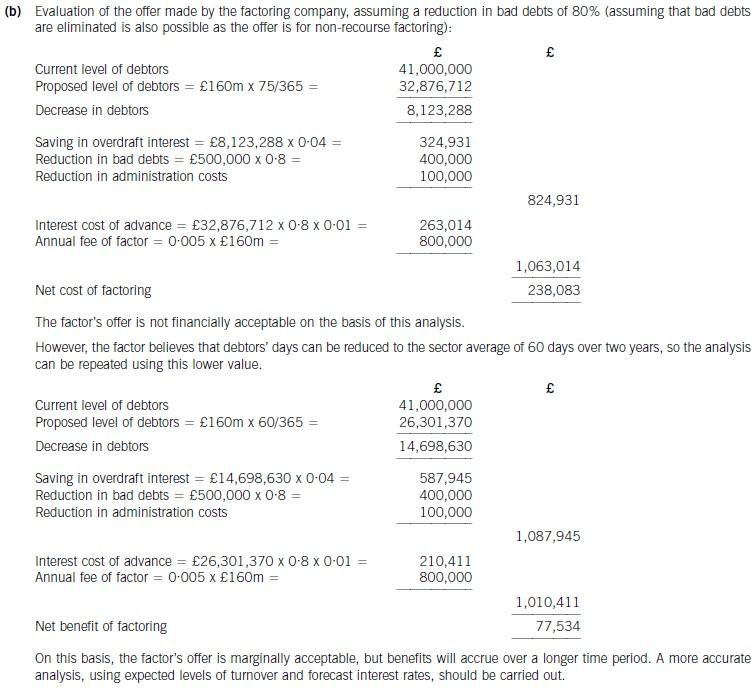

(b) Determine whether the factoring company’s offer can be recommended on financial grounds. Assume a

working year of 365 days and base your analysis on financial information for 2006. (8 marks)

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2019-01-05

- 2021-01-08

- 2020-01-10

- 2020-08-12

- 2020-04-16

- 2020-01-01

- 2020-10-18

- 2019-01-05

- 2020-09-05

- 2020-09-05

- 2021-01-08

- 2021-04-04

- 2021-01-06

- 2021-04-07

- 2020-01-10

- 2020-01-14

- 2020-08-12

- 2019-10-06

- 2019-03-20

- 2019-01-05

- 2020-08-17

- 2020-08-12

- 2020-01-01

- 2020-09-05

- 2020-01-10

- 2020-10-18

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2019-03-20