听说ACCA考试挺难,是真的吗?

发布时间:2019-07-21

很多同学一听到ACCA考试科目一共有14门在加上全英文的,就觉得考试很难。那么ACCA难考吗?ACCA全球通过率高吗?通过率是多少?报名ACCA需要准备什么材料?这些问题对于一个准备报考ACCA的小伙伴来说一定是在心里徘徊已久的问题了。为此小编特地整理了如下内容。

一、ACCA考试难度

ACCA是全英文考试,教材有非常厚,有几十本,考试科目也非常多,有13门。这些因素凑在一块,无疑不在加深ACCA的难度。不过,ACCA考试的难度是以英国大学学位考试的难度为标准。具体而言,第一(f1-f3)、第二部分(f4-f9)的难度分别相当于学士学位高年级课程的考试难度,第三部分的考试相当于硕士学位最后阶段的考试。

第一部分的每门考试只是测试本门课程所包含的知识,着重于为后两个部分中实务性的课程所要运用的理论和技能打下基础。

第二部分的考试除了本门课程的内容之外,还会考到第一部分的一些知识,着重培养学员的分析能力。

第三部分的考试要求学员综合运用学到的知识、技能和决断力。不仅会考到以前的课程内容,还会考到邻近科目的内容。

二、ACCA全球单科通过率

ACCA全球单科通过率基本在30-40%左右,中国学员通过率为50-60%。

ACCA作为国际注册会计师,逐渐受到了越来越多财务人士的认可。ACCA证书的含金量比较高,但是它的报考门槛却不高,凡具有国家教育局认可的大专以上学历即可报名参加考试。

三、在线注册报名考试的时候,需要准备哪些资料呢?

1.学历/ 学位证明(高校在校生需提交学校出具的在校证明函及第一年所有课程考试合格的成绩单)的原件、复印件和译文;外地申请者不要邮寄原件,请把您的申请材料复印件加盖公司或学校公章,或邮寄公证件既可。

2.身份证的原件、复印件和译文;或提供护照,不需提交翻译件。

3.两张张两寸照片;(黑白彩色均可)

4.注册报名费(银行汇票或信用卡支付),请确认信用卡可以从国外付款,否则会影响您的注册返回时间;如果不能确定建议您用汇票交纳注册费。(信用卡支付请在英文网站上注册时直接输入信用卡详细信息,英国总部收到您的书面注册材料后才会从您的信用卡上划帐)。

综上所述就是关于ACCA问题的解答,希望对于各位小伙伴有用,小编将持续为大家更新ACCA相关内容。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) International Standards on Auditing (ISAs); and (5 marks)

(b) International Standards on Auditing (ISAs)

The groundwork for an international set of auditing standards began in 1969 with a number of reports published by the

Accountants International Study Group that compared the situation in Canada, the UK, and US. The establishment of the

International Accounting Standards Committee (IASC), in 1973, generated calls for a similar body to be set up for auditing.

In the late 1970s the Council of International Federation of Accountants (IFAC) created the International Auditing Practices

Committee (IAPC) as a standing committee of the IFAC Council. (Subsequently the IFAC Board.)

Tutorial note: The IFAC Council was renamed the IFAC Board in May 2000.

The first ISA was issued in 1991. The codified core set released in 1994, which has remained the series to the present day,

has been increasingly accepted by national standard setters and auditors involved in global reporting and cross-border

financing transactions.

In July 2001, IFAC sought comment on the role of IASC3 and the future of ISAs. As a result of the review, in 2002, the IAPC

was renamed the International Auditing and Assurance Standards Board (IAASB). IAASB has made available, on its website,

the full text of ISAs since 2003.

Further, the growth of non-audit assurance services has led to the development of a new framework (‘The International

Framework for Assurance Engagements’) effective for assurance reports issued on or after 1 January 2005.

The hope that the take up of ISAs should follow the lead set by International Accounting Standards (IASs), following their

endorsement by IOSCO (the International Organization of Securities Commissions), has been expressed by many professional

bodies including ACCA and FEE (the Fédération des Experts Comptables Européens). FEE has been leading the debate on

the future of ISAs in Europe since 2001.

ISAs provide for the international harmonisation of national standards and the adoption of a global framework approach. As

a member of CCAB (the Consultative Committee of Accountancy Bodies) ACCA is committed to consulting its members on

the adoption of ISAs in the UK, and working with FEE, the European Commission (EC) and others.

In response to the move in the profession, away from the ‘traditional audit risk’ model, to a business risk model, IAASB issued

ISA 315 ‘Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement,’ ISA 330 ‘The

Auditor’s Procedures in Response to Assessed Risks’ and ISA 500 (Revised) ‘Audit Evidence’. These standards (and

conforming amendments) are effective for audits of financial statements for periods beginning on or after 15 December 2004.

That is, they will be applicable to financial statements for periods beginning on or after 1 January 2005 that in the European

Economic Area (EEA) and elsewhere will be adopting International Financial Reporting Standards (IFRSs) for the first time.

The adoption of ISAs has been welcomed by professional bodies as providing a robust approach to risk, fraud and quality

control that is particularly important in the light of recent events (Enron/Worldcom/Parmalat). For example, ISA 315 provides

additional guidance on the assessment of risks of material misstatement at the financial statement level and at the assertion

level.

Tutorial note: Recent developments could validly be illustrated with reference to other standards. For example, ISA 240

(Revised) ‘The Auditor’s Responsibility to Consider Fraud in an Audit of Financial Statements’ that became effective from

1 January 2005 has raised auditor awareness of earnings management and the greater need for professional skepticism.

ISA 700 (Revised) ‘The Independent Auditor’s Report on a Complete Set of General Purpose Financial Statements’ is effective

for audits of financial statements for periods beginning on or after 15 December 2005. This proposed significant changes to

the auditor’s report to help promote consistency in reporting practices worldwide.

The International Organization of Securities Commissions (IOSCO) is in discussion with IAASB about the possible

endorsement of ISAs (similar to its endorsement of IASs).

Practicing professionals must keep themselves up to date on auditing standards if they are to provide quality audits. Failure

to do so could result in negligence claims and/or disciplinary action (e.g. by ACCA’s disciplinary committee). A survey by FEE

has demonstrated that the European accountancy bodies broadly comply with ISAs. However, an earlier survey4 of IFAC

member bodies showed that 14% had some significant differences (usually relating to reporting). IFAC needs to require its

member bodies to act rather than merely encourage implementation. A set of global ethical requirements will help improve

the implementation of ISAs as well as reduce the expectation gap in performing audits of financial statements.

(b) (i) Explain the matters you should consider, and the evidence you would expect to find in respect of the

carrying value of the cost of investment of Dylan Co in the financial statements of Rosie Co; and

(7 marks)

(b) (i) Cost of investment on acquisition of Dylan Co

Matters to consider

According to the schedule provided by the client, the cost of investment comprises three elements. One matter to

consider is whether the cost of investment is complete.

It appears that no legal or professional fees have been included in the cost of investment (unless included within the

heading ‘cash consideration’). Directly attributable costs should be included per IFRS 3 Business Combinations, and

there is a risk that these costs may be expensed in error, leading to understatement of the investment.

The cash consideration of $2·5 million is the least problematical component. The only matter to consider is whether the

cash has actually been paid. Given that Dylan Co was acquired in the last month of the financial year it is possible that

the amount had not been paid before the year end, in which case the amount should be recognised as a current liability

on the statement of financial position (balance sheet). However, this seems unlikely given that normally control of an

acquired company only passes to the acquirer on cash payment.

IFRS 3 states that the cost of investment should be recognised at fair value, which means that deferred consideration

should be discounted to present value at the date of acquisition. If the consideration payable on 31 January 2009 has

not been discounted, the cost of investment, and the corresponding liability, will be overstated. It is possible that the

impact of discounting the $1·5 million payable one year after acquisition would be immaterial to the financial

statements, in which case it would be acceptable to leave the consideration at face value within the cost of investment.

Contingent consideration should be accrued if it is probable to be paid. Here the amount is payable if revenue growth

targets are achieved over the next four years. The auditor must therefore assess the probability of the targets being

achieved, using forecasts and projections of Maxwell Co’s revenue. Such information is inherently subjective, and could

have been manipulated, if prepared by the vendor of Maxwell Co, in order to secure the deal and maximise

consideration. Here it will be crucial to be sceptical when reviewing the forecasts, and the assumptions underlying the

data. The management of Rosie Co should have reached their own opinion on the probability of paying the contingent

consideration, but they may have relied heavily on information provided at the time of the acquisition.

Audit evidence

– Agreement of the monetary value and payment dates of the consideration per the client schedule to legal

documentation signed by vendor and acquirer.

– Agreement of $2·5 million paid to Rosie Co’s bank statement and cash book prior to year end. If payment occurs

after year end confirm that a current liability is recognised on the individual company and consolidated statement

of financial position (balance sheet).

– Board minutes approving the payment.

– Recomputation of discounting calculations applied to deferred and contingent consideration.

– Agreement that the discount rate used is pre-tax, and reflects current market assessment of the time value of money

(e.g. by comparison to Rosie Co’s weighted average cost of capital).

– Revenue and profit projections for the period until January 2012, checked for arithmetic accuracy.

– A review of assumptions used in the projections, and agreement that the assumptions are comparable with the

auditor’s understanding of Dylan Co’s business.

Tutorial note: As the scenario states that Chien & Co has audited Dylan Co for several years, it is reasonable to rely on

their cumulative knowledge and understanding of the business in auditing the revenue projections.

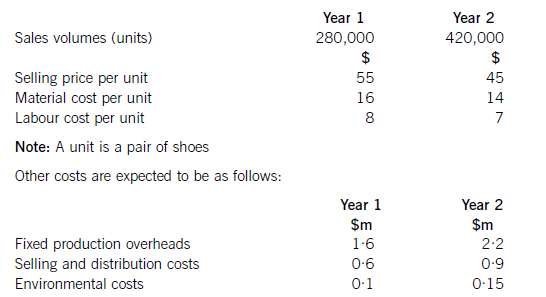

Shoe Co, a shoe manufacturer, has developed a new product called the ‘Smart Shoe’ for children, which has a built-in tracking device. The shoes are expected to have a life cycle of two years, at which point Shoe Co hopes to introduce a new type of Smart Shoe with even more advanced technology. Shoe Co plans to use life cycle costing to work out the total production cost of the Smart Shoe and the total estimated profit for the two-year period.

Shoe Co has spent $5·6m developing the Smart Shoe. The time spent on this development meant that the company missed out on the opportunity of earning an estimated $800,000 contribution from the sale of another product.

The company has applied for and been granted a ten-year patent for the technology, although it must be renewed each year at a cost of $200,000. The costs of the patent application were $500,000, which included $20,000 for the salary costs of Shoe Co’s lawyer, who is a permanent employee of the company and was responsible for preparing the application.

The following information is also available for the next two years:

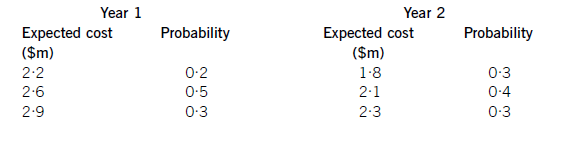

Shoe Co is still negotiating with marketing companies with regard to its advertising campaign, so is uncertain as to what the total marketing costs will be each year. However, the following information is available as regards the probabilities of the range of costs which are likely to be incurred:

Required:

Applying the principles of life cycle costing, calculate the total expected profit for Shoe Co for the two-year period.

(10 marks)

Totalsalesrevenue=(280,000x$55)+(420,000x$45)=$15·4m+18·9m=$34·3m.NoteTheexpectedprofithasbeencalculatedusinglifecyclecostingnotrelevantcosting.Hence,the$20,000salarycostincludedinpatentcostsshouldbeincludedinthelifecyclecost.Similarly,theopportunitycostof$800,000isnotincludedusinglifecyclecostingwhereasifrelevantcostingwasbeingusedtodecideonaparticularcourseofaction,theopportunitycostwouldbeincluded.Working1Expectedmarketingcostinyear1:(0·2x$2·2m)+(0·5x$2·6m)+(0·3x$2·9m)=$2·61mExpectedmarketingcostyear2:(0·3x$1·8m)+(0·4x$2·1m)+(0·3x$2·3m)=$2·07mTotalexpectedmarketingcost=$4·68m

(b) Using relevant evaluation criteria, assess how achievable and compatible these three strategic goals are over

the next five years. (20 marks)

(b) The three strategic goals are to become the leading premium ice cream brand in the UK; to increase sales to £25 million;

and to achieve a significant entry into the supermarket sector. On the basis of performance to date these goals will certainly

be stretching. All three strategies will involve significant growth in the company. Johnson and Scholes list three success criteria

against which the strategies can be assessed, namely suitability, acceptability and feasibility. Suitability is a test of whether a

strategy addresses the situation in which a company is operating. In Johnson and Scholes’ terms it is the firm’s ‘strategic

position’, an understanding of which comes from the analysis done in the answer to the question above. Acceptability is

concerned with the likely performance outcomes of the strategy and in particular whether the return and risk are in line with

the expectations of the stakeholders. Feasibility is the extent to which the strategy can be made to work and is determined

by the strategic capability of the company reflecting the resources available to implement the strategy. It is interesting to see

that the three growth related goals are compatible in that becoming the leading premium brand will involve increased market

penetration, product development and market development. If achieved it will increase sales and necessitate a successful

entry into the supermarket sector. Time will be an important influence on the success or otherwise of these growth goals –

five years seems to be a reasonable length of time to achieve these ambitious targets.

Suitability – Churchill is currently a small but significant player at the premium end of the market. This segment is becoming

more significant and is attractive because of the high prices and high margins attainable. This is leading to more intense

competition with global companies. One immediate question that springs to mind is what precisely does ‘leading brand’

mean? The most obvious test is that of market share and unless Churchill achieve the access to the supermarkets looked for

in the third strategic goal, seems difficult to achieve. If ‘leading brand’ implies brand recognition this again looks very

ambitious. On the positive side this segment of the ice cream market is showing significant growth and Churchill’s success

in gaining sponsorship rights to major sporting events is a step in the right direction. The combination of high price and high

quality should position the company where it wants to be. Achieving sales of £25 million represents a quantum shift in

performance in a company that has to date only achieved modest levels of sales growth.

Acceptability – as a family owned business the balance between risk and return is an important one. The family to date has

been ‘happy’ with a modest rate of growth and modest return in terms of profits. The other significant stakeholder group is

the professional managers headed up by Richard Smith. They seem much more growth orientated and may be happier with

the risks that the growth strategy entails. The family members seem more interested in the manufacturing side than the

retailing side of the business and their bad previous experiences with growing the business through international market

development may mean they are risk averse and less willing to invest the necessary resources.

Feasibility – again this is linked to how ‘leading brand’ is defined. If as seems likely the brand becomes more widely known

through increasing the number of company owned ice cream stores then a significant investment in retail outlets will be

necessary. Increasing the number of franchised outlets will reduce the financial resources required but may be at the expense

of the brand’s reputation. Certainly there would seem to be a need for increased levels of advertising and promotion –

particularly to gain access to the ice cream cabinets in the supermarket chains. This is likely to mean an increase in the

number of sales and marketing staff. Equally important will be the ability to develop and launch new products in a luxury

market shaped by impulse buying and customers looking to indulge themselves.

Overall, becoming the leading brand of premium ice cream may well be the key to achieving the desired presence in the

supermarket ice cream cabinets, which in turn is a pre-requisite for increasing company sales to £25 million. So the three

strategic goals may be regarded as consistent and compatible with one another. However each strategic goal will have to be

broken down into its key elements. For example in achieving sales of £25 million what proportion of sales will come from its

own ice cream stores and what proportion from other outlets including the supermarkets? Sales to date of Churchill ice cream

are dominated by impulse purchases but in achieving sales of £25 million penetrating the take home market will be essential.

Finally, what proportion of these take home sales will be under the supermarkets own label brands? Over reliance on own

label sales will seriously weaken Churchill’s desire to become the leading national brand of premium ice cream. It looks to

be an ambitious but attainable strategy but will require a significant planning effort to develop the necessary resources andcapabilities vital to successful implementation of the strategy.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-03

- 2020-01-10

- 2020-01-09

- 2020-03-04

- 2020-01-10

- 2020-01-09

- 2020-03-11

- 2020-03-12

- 2020-01-09

- 2021-04-23

- 2020-01-09

- 2020-01-01

- 2020-01-10

- 2020-04-14

- 2019-07-21

- 2020-04-15

- 2020-01-10

- 2020-03-26

- 2020-08-01

- 2020-01-10

- 2020-03-08

- 2020-01-10

- 2020-01-09

- 2020-02-28

- 2020-03-03

- 2020-01-10

- 2020-03-12

- 2020-01-10

- 2020-03-17

- 2020-01-10