宁夏考生:ACCA考试的科目和报考规定是什么呀?

发布时间:2020-01-10

当有些小伙伴正在如火如荼地备考ACCA考试的时候,千万不要忘了最重要的一个步骤,那就是考试报名。目前正处于ACCA考试常规报名阶段,51题库考试学习网提醒大家想要报考2020年ACCA考试的考生要抓紧时间报名了哦!51题库考试学习网帮助大家汇总了ACCA官网上发布的部分内容,来看看是不是你所需要的呢?

按照规定,学员在每个考季最多可报考4个科目(包括重考科目和新科目)并且每年报考不超过8门新科目,保证每门课程都有充足的学习时间。另外,学员必须按照以下3个阶段的顺序来报考ACCA科目。

知识模块的科目:F1-F3;

技能模块的科目:F4-F9(F4ENG/GLO 开启随时机考);

专业阶段的科目:P1, P2, P3 (and any two from P4, P5, P6 and P7)。

以上3个阶段内的考试科目可不分先后顺序报考,但如前一阶段有未通过的科目,将不能跳开此科目仅报后阶段科目。

ACCA每年会根据会计准则及事实的需要调整教学大纲,当年的考试会以最新的教学大纲作为考核内容,ACCA考官也会不定期的在ACCA官方网站上发表考官文章,帮助学生解析考试当中的一些难点和重点,ACCA教材也应随着考试大纲的不断变化,每年出最新版本,历年考题答案应随着教材变更后,调整最新答案。

学生在拿到最新教材后可以进行逐章逐节的学习,在掌握了每章节知识点后,将历年考题作为复习重点,充分的加以练习,达到熟练的程度,以保证考试的顺利通过。

与此同时,学生可以按照自身的需求,选择一些与教材紧密结合的辅导课程,由讲师为同学们总结考试重点及难点,深入分析、拓展思维,为学生节省时间,并且带领同学们一起做历年考题,学习考官文章,共同克服备课过程当中出现的各种困难增加学习效率及通过率。

除了认真备考熟练掌握知识点以外,ACCA对考试技巧,答题速度及考场的应试技巧也有很高的要求,很多同学复习阶段已经熟练的掌握知识点,但是考场应变能力差,考试时间没能合理分配,最终也很容易造成考试失败,正确的备考、应考方法也因此成为了考试顺利通过的关键,因此在备考经验不是很丰富的同学可以选择相关课程跟随老师一同学习。

以上信息就是关于ACCA的考试科目和报考规定的介绍,希望对正在努力备考的ACCAer们有所帮助。目前的ACCA证书含金量是相当高的,各位小伙伴不要觉得考试很难就放弃,付出的努力和得到的结果是成正比的,大家要坚持努力的复习学习,克服身边的一切诱惑!当你拿到证书的那一科你就明白所以的努力都是值得的。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

5 An organisation’s goals can only be achieved through the efforts of motivated individuals.

Required:

Explain what is meant by the following terms:

(a) Hygiene factors. (8 marks)

5 Overview

Understanding what motivates people is necessary at all levels of management. It is important that professional accountants

understand the relevance of individual motivation. Unless individuals are well managed and motivated they are unlikely to cooperate

to achieve the organisation’s objectives.

Part (a):

(a) Hygiene (or maintenance) factors lead to job dissatisfaction because of the need to avoid unpleasantness. They are so called

because they can in turn be avoided by the use of ‘hygienic’ methods, that is, they can be prevented. Attention to these

hygiene factors prevents dissatisfaction but does not on its own provide motivation.

Hygiene factors (or ‘dissatisfiers’) are concerned with those factors associated with, but not directly a part of, the job itself.

Herzberg suggested that these are mainly salary and the perceived differences with others’ salaries, job security, working

conditions, the level and quality of supervision, organisational policy and administration and the nature of interpersonal

relationships. Resolution of hygiene factors, however, is short term, longer term resolution requires motivator factors.

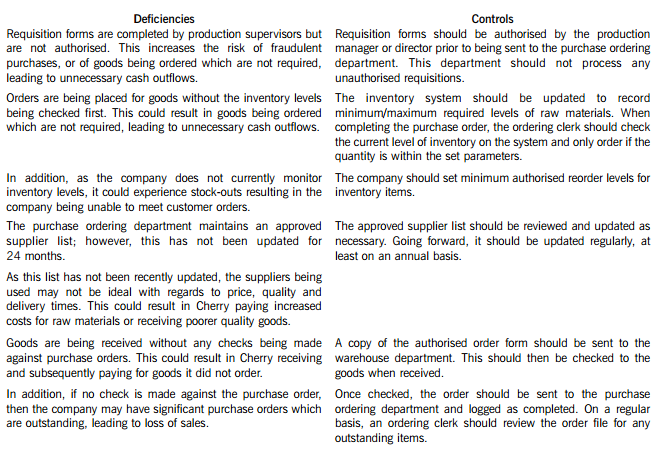

Cherry Blossom Co (Cherry) manufactures custom made furniture and its year end is 30 April. The company purchases its raw materials from a wide range of suppliers. Below is a description of Cherry’s purchasing system.

When production supervisors require raw materials, they complete a requisition form. and this is submitted to the purchase ordering department. Requisition forms do not require authorisation and no reference is made to the current inventory levels of the materials being requested. Staff in the purchase ordering department use the requisitions to raise sequentially numbered purchase orders based on the approved suppliers list, which was last updated 24 months ago. The purchasing director authorises the orders prior to these being sent to the suppliers.

When the goods are received, the warehouse department verifies the quantity to the suppliers despatch note and checks that the quality of the goods received are satisfactory. They complete a sequentially numbered goods received note (GRN) and send a copy of the GRN to the finance department.

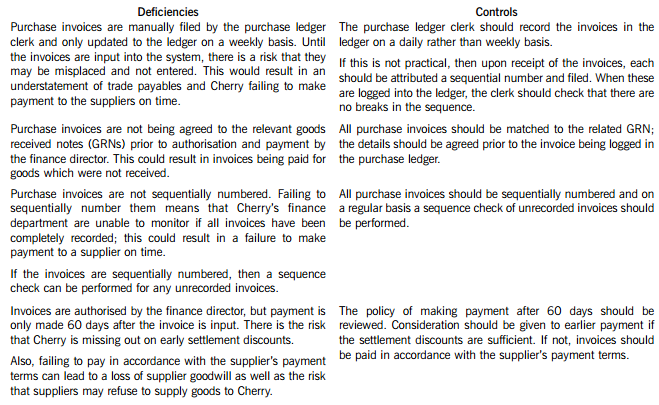

Purchase invoices are sent directly to the purchase ledger clerk, who stores them in a manual file until the end of each week. He then inputs them into the purchase ledger using batch controls and gives each invoice a unique number based on the supplier code. The invoices are reviewed and authorised for payment by the finance director, but the actual payment is only made 60 days after the invoice is input into the system.

Required:

In respect of the purchasing system of Cherry Blossom Co:

(i) Identify and explain FIVE deficiencies; and

(ii) Recommend a control to address each of these deficiencies.

Note: The total marks will be split equally between each part.

Cherry Blossom Co’s (Cherry) purchasing system deficiencies and controls

2 (a) Discuss the nature of the financial objectives that may be set in a not-for-profit organisation such as a charity

or a hospital. (8 marks)

2 (a) In the case of a not-for-profit (NFP) organisation, the limit on the services that can be provided is the amount of funds that

are available in a given period. A key financial objective for an NFP organisation such as a charity is therefore to raise as

much funds as possible. The fund-raising efforts of a charity may be directed towards the public or to grant-making bodies.

In addition, a charity may have income from investments made from surplus funds from previous periods. In any period,

however, a charity is likely to know from previous experience the amount and timing of the funds available for use. The same

is true for an NFP organisation funded by the government, such as a hospital, since such an organisation will operate under

budget constraints or cash limits. Whether funded by the government or not, NFP organisations will therefore have the

financial objective of keeping spending within budget, and budgets will play an important role in controlling spending and in

specifying the level of services or programmes it is planned to provide.

Since the amount of funding available is limited, NFP organisations will seek to generate the maximum benefit from available

funds. They will obtain resources for use by the organisation as economically as possible: they will employ these resources

efficiently, minimising waste and cutting back on any activities that do not assist in achieving the organisation’s non-financial

objectives; and they will ensure that their operations are directed as effectively as possible towards meeting their objectives.

The goals of economy, efficiency and effectiveness are collectively referred to as value for money (VFM). Economy is

concerned with minimising the input costs for a given level of output. Efficiency is concerned with maximising the outputs

obtained from a given level of input resources, i.e. with the process of transforming economic resources into desires services.

Effectiveness is concerned with the extent to which non-financial organisational goals are achieved.

Measuring the achievement of the financial objective of VFM is difficult because the non-financial goals of NFP organisations

are not quantifiable and so not directly measurable. However, current performance can be compared to historic performance

to ascertain the extent to which positive change has occurred. The availability of the healthcare provided by a hospital, for

example, can be measured by the time that patients have to wait for treatment or for an operation, and waiting times can be

compared year on year to determine the extent to which improvements have been achieved or publicised targets have been

met.

Lacking a profit motive, NFP organisations will have financial objectives that relate to the effective use of resources, such as

achieving a target return on capital employed. In an organisation funded by the government from finance raised through

taxation or public sector borrowing, this financial objective will be centrally imposed.

(b) (i) Explain, by reference to Coral’s residence, ordinary residence and domicile position, how the rental

income arising in respect of the property in the country of Kalania will be taxed in the UK in the tax year

2007/08. State the strategy that Coral should adopt in order to minimise the total income tax suffered

on the rental income. (7 marks)

(b) (i) UK tax on the rental income

Coral is UK resident in 2007/08 because she is present in the UK for more than 182 days. Accordingly, she will be

subject to UK income tax on her Kalanian rental income.

Coral is ordinarily resident in the UK in 2007/08 as she is habitually resident in the UK.

Coral will have acquired a domicile of origin in Kalania from her father. She has not acquired a domicile of choice in the

UK as she has not severed her ties with Kalania and does not intend to make her permanent home in the UK.

Accordingly, the rental income will be taxed in the UK on the remittance basis.

Any rental income remitted to the UK will fall into the basic rate band and will be subject to income tax at 22% on the

gross amount (before deduction of Kalanian tax). Unilateral double tax relief will be available in respect of the 8% tax

suffered in Kalania such that the effective rate of tax suffered by Coral in the UK on the grossed up amount of income

remitted will be 14%.

In order to minimise the total income tax suffered on the rental income Coral should ensure that it is not brought into or

used in the UK such that it will not be subject to income tax in the UK.

Coral should retain evidence, for example bank statements, to show that the rental income has not been removed from

Kalania. Coral can use the money whilst she is on holiday in Kalania with no UK tax implications.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-04-15

- 2020-02-28

- 2020-01-10

- 2020-03-04

- 2020-02-29

- 2020-01-10

- 2020-01-03

- 2020-01-08

- 2020-03-14

- 2020-01-09

- 2020-01-09

- 2020-01-10

- 2020-02-06

- 2021-05-06

- 2020-01-08

- 2020-01-10

- 2020-01-08

- 2020-01-10

- 2019-07-21

- 2020-02-28

- 2020-04-03

- 2020-01-09

- 2020-03-05

- 2020-08-13

- 2020-01-09

- 2020-01-09

- 2020-03-14

- 2019-03-30

- 2019-12-29

- 2020-04-16