2020年黑龙江ACCA国际会计师考场规则,可以带计算器!

发布时间:2020-01-09

ACCA考场规则是什么呢?跟国内考试的规定有区别吗?这些问题是许多即将参加2020年3月份ACCA考试的同学们最关心的问题,害怕自己辛辛苦苦准备了几个月之久的考试就因为一个不小心触犯了相关的规定,那就得不偿失了。接下来,51题库考试学习网为大家盘点历年来ACCA考试的相关规定,希望大家引以为戒,小心不要触犯哟~

具体点来说,ACCA考试的考场规则主要分为两部分,一个就是进入考场前,另一个就是进入考场之后

ACCA考前规则:

1.考生须在开始考试之前30分钟到达ACCA考试地点,以免在出现突发情况。监考老师对考生进行核查考生本人身份证、ACCA注册号。

2.考生可选择开考前进行网上测试(见机考中心通知),也可选择开考前1小时到达考点,在机考中心进行测试,熟悉机考流程。(建议考生最好选择前者,后者可能出现在机考中心测试的人数太多而不能及时测试导致不熟悉机考流程的情况)

3.考生在考试开始前15分钟经过监考老师批准方可进入考场。逾时不得再进入考场。

4. 考生在到达考场并进行签到后,如因特殊原因需要离场,请主动联系监考人员,不得擅自离开,经过监考老师允许之后才可以离开。

5. 最好不要携带贵重物品前往考场,丢失了后果自负的。

注意:ACCA机考必须带那些东西

首先是自行在官网上打印的准考证其次就是身份证再是可以携带不带有记忆存储功能的计算器。(如考生有携带手机、包包等私人物品,请将其放至监考老师指定区域。)

进入考场后的规则

1.考生进入考场后必须把考试相关书籍材料等放到指定位置,并将手机等通讯设备关闭。考生只允许携带考试规定携带的东西进入考场,例如本人身份证、笔、单功能计算器进入考场,一经发现,按作弊处理。

2.考试开始前,监考人员会宣读考场纪律;考生需要在电脑上输入个人信息,监考人员会核对考生的身份;身份核对后,电脑上会显示出3页考试操作指南,考生仔细阅读,阅读完毕之后,举手向监控人员请示,得到监考人员的允许后才可点击考试科目,开始考试。

3.考试开始时,题目会直接在屏幕上显示,请直接在电脑上输入答案。不能点开电脑里的其他软件

4.考试结束后,需要打印2份考试成绩通知单,自己保留一份,机考中心保留一份。

5.机考中心会在考试结束后上传考试成绩,72小时内成绩会上传到考生的MYACCA成绩记录中。

6.考试费用一旦交付,如因考生自身原因缺考,作弃权处理,不须考虑退款事宜。因此建议各位考生要谨慎报名,毕竟考试费用也是一笔不小的费用。

7.ACCA机考中心保留因不可抗力因素(如网络问题,停电等)调整机考时间或取消考试的权力。出现了以上情况,及时向监考人员反映,他们会为你解决问题。

迟到及提早交卷规定:

在开考后1小时内到达的迟到考生可以入场,但不能补偿考试时间。简单的来说就是即便是晚到1小时,你的考试时间也不会往后延时1小时,交卷铃声响起你同样得交卷。而开考1小时以后到达的考生就算做放弃此次考试,不能入场。

这些考场规则有没有帮助到各位ACCAer们呀?相信大家看了之后或多或少对ACCA考场规则都有了一定的了解,51题库考试学习网提醒大家,认真阅读考场规则,如果和上面所述的规则有一定的出入,各地的相关考场规则以各地的为准,最后51题库考试学习网预祝大家考试顺利上岸~

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) Discuss the nature of the following issues in developing IFRSs for SMEs.

(i) The purpose of the standards and the type of entity to whom they should apply. (7 marks)

(b) There are several issues which need to be addressed when developing IFRSs for SMEs:

(i) The purpose of the standards and type of entity

The principal aim of the development of an accounting framework for SMEs is to provide a framework which generates

relevant, reliable and useful information. The standards should provide high quality and understandable accounting

standards suitable for SMEs globally. Additionally they should meet the needs set out in (a) above. For example reduce

the financial reporting burden for SMEs. It is unlikely that one of the objectives would be to provide information for

management or meet the needs of the tax authorities as these bodies will have specific requirements which would be

difficult to meet in an accounting standard. However, it is likely that the standards for SMEs will be a modified version

of the full IFRSs and not an independently developed set of standards in order that they are based on the same

conceptual framework and will allow easier transition to full IFRS if the SME grows or decides to become a publicly listed

entity.

It is important to define the type of entity for which the standards are intended. Companies who have issued shares to

the public would be expected to use full IFRS. The question arises as to whether SME standards should apply to all

unlisted entities or just those listed entities below a certain size threshold. The difficulty with size criteria is that it would

have to apply worldwide and it would be very difficult to specify such criteria. Additionally some unlisted companies, for

example public utilities, have a reporting obligation that is equivalent to that of a listed company and should follow full

IFRS.

The main characteristic which distinguishes SMEs from other entities is the degree of public accountability. Thus the

definition of what constitutes an SME could revolve around those entities that do not have public accountability.

Indicators of public accountability will have to be developed. For example, a listed company or companies holding assets

in a fiduciary capacity (bank), or a public utility, or an entity with economic significance in its country. Thus all entities

that do not have public accountability may be considered as potential users of IFRSs for SMEs.

Size may not be the best way to determine what is an SME. SMEs could be defined by reference to ownership and themanagement of the entity. SMEs are not necessarily just smaller versions of public companies.

Moonstar Co is a property development company which is planning to undertake a $200 million commercial property development. Moonstar Co has had some difficulties over the last few years, with some developments not generating the expected returns and the company has at times struggled to pay its finance costs. As a result Moonstar Co’s credit rating has been lowered, affecting the terms it can obtain for bank finance. Although Moonstar Co is listed on its local stock exchange, 75% of the share capital is held by members of the family who founded the company. The family members who are shareholders do not wish to subscribe for a rights issue and are unwilling to dilute their control over the company by authorising a new issue of equity shares. Moonstar Co’s board is therefore considering other methods of financing the development, which the directors believe will generate higher returns than other recent investments, as the country where Moonstar Co is based appears to be emerging from recession.

Securitisation proposals

One of the non-executive directors of Moonstar Co has proposed that it should raise funds by means of a securitisation process, transferring the rights to the rental income from the commercial property development to a special purpose vehicle. Her proposals assume that the leases will generate an income of 11% per annum to Moonstar Co over a ten-year period. She proposes that Moonstar Co should use 90% of the value of the investment for a collateralised loan obligation which should be structured as follows:

– 60% of the collateral value to support a tranche of A-rated floating rate loan notes offering investors LIBOR plus 150 basis points

– 15% of the collateral value to support a tranche of B-rated fixed rate loan notes offering investors 12%

– 15% of the collateral value to support a tranche of C-rated fixed rate loan notes offering investors 13%

– 10% of the collateral value to support a tranche as subordinated certificates, with the return being the excess of receipts over payments from the securitisation process

The non-executive director believes that there will be sufficient demand for all tranches of the loan notes from investors. Investors will expect that the income stream from the development to be low risk, as they will expect the property market to improve with the recession coming to an end and enough potential lessees to be attracted by the new development.

The non-executive director predicts that there would be annual costs of $200,000 in administering the loan. She acknowledges that there would be interest rate risks associated with the proposal, and proposes a fixed for variable interest rate swap on the A-rated floating rate notes, exchanging LIBOR for 9·5%.

However the finance director believes that the prediction of the income from the development that the non-executive director has made is over-optimistic. He believes that it is most likely that the total value of the rental income will be 5% lower than the non-executive director has forecast. He believes that there is some risk that the returns could be so low as to jeopardise the income for the C-rated fixed rate loan note holders.

Islamic finance

Moonstar Co’s chief executive has wondered whether Sukuk finance would be a better way of funding the development than the securitisation.

Moonstar Co’s chairman has pointed out that a major bank in the country where Moonstar Co is located has begun to offer a range of Islamic financial products. The chairman has suggested that a Mudaraba contract would be the most appropriate method of providing the funds required for the investment.

Required:

(a) Calculate the amounts in $ which each of the tranches can expect to receive from the securitisation arrangement proposed by the non-executive director and discuss how the variability in rental income affects the returns from the securitisation. (11 marks)

(b) Discuss the benefits and risks for Moonstar Co associated with the securitisation arrangement that the non-executive director has proposed. (6 marks)

(c) (i) Discuss the suitability of Sukuk finance to fund the investment, including an assessment of its appeal to potential investors. (4 marks)

(ii) Discuss whether a Mudaraba contract would be an appropriate method of financing the investment and discuss why the bank may have concerns about providing finance by this method. (4 marks)

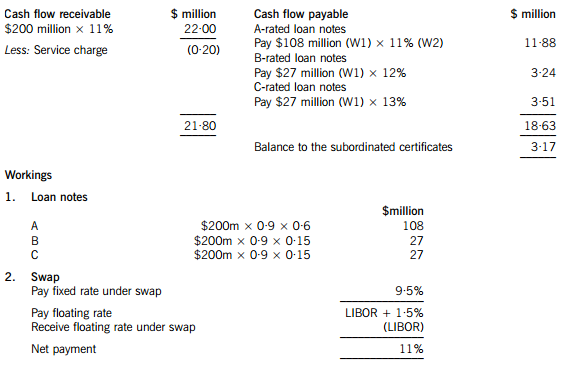

(a) An annual cash flow account compares the estimated cash flows receivable from the property against the liabilities within the securitisation process. The swap introduces leverage into the arrangement.

The holders of the certificates are expected to receive $3·17million on $18 million, giving them a return of 17·6%. If the cash flows are 5% lower than the non-executive director has predicted, annual revenue received will fall to $20·90 million, reducing the balance available for the subordinated certificates to $2·07 million, giving a return of 11·5% on the subordinated certificates, which is below the returns offered on the B and C-rated loan notes. The point at which the holders of the certificates will receive nothing and below which the holders of the C-rated loan notes will not receive their full income will be an annual income of $18·83 million (a return of 9·4%), which is 14·4% less than the income that the non-executive director has forecast.

(b) Benefits

The finance costs of the securitisation may be lower than the finance costs of ordinary loan capital. The cash flows from the commercial property development may be regarded as lower risk than Moonstar Co’s other revenue streams. This will impact upon the rates that Moonstar Co is able to offer borrowers.

The securitisation matches the assets of the future cash flows to the liabilities to loan note holders. The non-executive director is assuming a steady stream of lease income over the next 10 years, with the development probably being close to being fully occupied over that period.

The securitisation means that Moonstar Co is no longer concerned with the risk that the level of earnings from the properties will be insufficient to pay the finance costs. Risks have effectively been transferred to the loan note holders.

Risks

Not all of the tranches may appeal to investors. The risk-return relationship on the subordinated certificates does not look very appealing, with the return quite likely to be below what is received on the C-rated loan notes. Even the C-rated loan note holders may question the relationship between the risk and return if there is continued uncertainty in the property sector.

If Moonstar Co seeks funding from other sources for other developments, transferring out a lower risk income stream means that the residual risks associated with the rest of Moonstar Co’s portfolio will be higher. This may affect the availability and terms of other borrowing.

It appears that the size of the securitisation should be large enough for the costs to be bearable. However Moonstar Co may face unforeseen costs, possibly unexpected management or legal expenses.

(c) (i) Sukuk finance could be appropriate for the securitisation of the leasing portfolio. An asset-backed Sukuk would be the same kind of arrangement as the securitisation, where assets are transferred to a special purpose vehicle and the returns and repayments are directly financed by the income from the assets. The Sukuk holders would bear the risks and returns of the relationship.

The other type of Sukuk would be more like a sale and leaseback of the development. Here the Sukuk holders would be guaranteed a rental, so it would seem less appropriate for Moonstar Co if there is significant uncertainty about the returns from the development.

The main issue with the asset-backed Sukuk finance is whether it would be as appealing as certainly the A-tranche of the securitisation arrangement which the non-executive director has proposed. The safer income that the securitisation offers A-tranche investors may be more appealing to investors than a marginally better return from the Sukuk. There will also be costs involved in establishing and gaining approval for the Sukuk, although these costs may be less than for the securitisation arrangement described above.

(ii) A Mudaraba contract would involve the bank providing capital for Moonstar Co to invest in the development. Moonstar Co would manage the investment which the capital funded. Profits from the investment would be shared with the bank, but losses would be solely borne by the bank. A Mudaraba contract is essentially an equity partnership, so Moonstar Co might not face the threat to its credit rating which it would if it obtained ordinary loan finance for the development. A Mudaraba contract would also represent a diversification of sources of finance. It would not require the commitment to pay interest that loan finance would involve.

Moonstar Co would maintain control over the running of the project. A Mudaraba contract would offer a method of obtaining equity funding without the dilution of control which an issue of shares to external shareholders would bring. This is likely to make it appealing to Moonstar Co’s directors, given their desire to maintain a dominant influence over the business.

The bank would be concerned about the uncertainties regarding the rental income from the development. Although the lack of involvement by the bank might appeal to Moonstar Co's directors, the bank might not find it so attractive. The bank might be concerned about information asymmetry – that Moonstar Co’s management might be reluctant to supply the bank with the information it needs to judge how well its investment is performing.

(b) Both divisions have recognised the need for a strategic alliance to help them achieve a successful entry into

European markets.

Critically evaluate the advantages and disadvantages of the divisions using strategic alliances to develop their

respective businesses in Europe. (15 marks)

(b) Johnson, Scholes and Whittington define a strategic alliance as ‘where two or more organisations share resources and

activities to pursue a strategy’. There are a number of types of alliance ranging from a formal joint venture through to networks

where there is collaboration but no formal agreement. The type of strategic alliance will be affected by how quickly market

conditions are changing – swift rates of change may require flexible less formal types of alliance and determine whether

specific dedicated resources are required or whether the partners can use existing resources. Johnson, Scholes and

Whittington argue that for an alliance to be successful there needs to be a clear strategic purpose and senior management

support; compatibility between the partners at all levels – this may be complicated if it is a cross-border alliance; time spent

defining and meeting performance expectations including clear goals, governance and organisational arrangements; and

finally trust both in terms of respective competences and trustworthiness.

6D–ENGAA

Paper 3.5

6D–ENGAA

Paper 3.5

The advantages that may be gained by a successful strategic alliance include creating a joint operation that has a ‘critical

mass’ that may lead to lower costs or an improved offer to the customer. It may also allow each partner to specialise in areas

where they have a particular advantage or competence. Interestingly, alliances are often entered into where a company is

seeking to enter new geographical markets, as is the case with both divisions. The partner brings local knowledge and

expertise in distribution, marketing and customer support. A good strategic alliance will also enable the partners to learn from

one another and develop competences that may be used in other markets. Often firms looking to develop an e-business will

use an alliance with a partner with experience in website development. Once its e-business is up and running a firm may

eventually decide to bring the website design skills in-house and acquire the partner.

Disadvantages of alliances range from over-dependence on the partner, not developing own core competences and a tendency

for them not to have a defined end date. Clearly there is a real danger of the partner eventually becoming a competitor.

In assessing the suitability for each division in using a strategic alliance to enter European markets one clearly has to analyse

the very different positions of the divisions in terms of what they can offer a potential partner. The earlier analysis suggests

that the Shirtmaster division may have the greater difficulty in attracting a partner. One may seriously question the feasibility

of using the Shirtmaster brand in Europe and the competences the division has in terms of manufacturing and selling to large

numbers of small independent UK clothing retailers would seem inappropriate to potential European partners. Ironically, if

the management consultant recommends that the Shirtmaster division sources some or all of its shirts from low cost

manufacturers in Europe this may provide a reason for setting up an alliance with such a manufacturer.

The prospects of developing a strategic alliance in the Corporate Clothing division are much more favourable. The division

has developed a value added service for its corporate customers, indeed its relationship with its customers can be seen as a

relatively informal network or alliance and there seems every chance this could be replicated with large corporate customers

in Europe. Equally, there may be European workwear companies looking to grow and develop who would welcome sharingthe Corporate Clothing division’s expertise.

(c) What changes to Churchill’s existing marketing mix will be needed to achieve the three strategic goals?

(15 marks)

(c) Each of the strategic goals will have a profound impact on the marketing mix as it currently exists. As each goal affects the

market position of Churchill developing an appropriate marketing mix will be the key to successful implementation of the

overall growth strategy. The product, the brand and the reputation it creates are at the heart of the company’s marketing

strategy. Their focus on the premium segment of the market seems a sensible one and one which allows a small family-owned

business to survive and grow slowly. Evidence suggests this is a luxury indulgence market reflecting changing consumer tastes

and lifestyles. Managing the product range will be a major marketing activity. While the core products may develop an almost

timeless quality there will be a need to respond to the product innovations introduced by its much larger competitors. The

company’s emphasis on the quality of its products resulting from the quality of its ingredients is at the heart of its competitive

advantage. Growing the product range will also bring the danger of under performing products and a consequent need to

divest such products. Packaging is likely to be a key part of the products’ appeal and will be an area where constant innovation

is important.

Pricing raises a number of issues. Why is Churchill’s core product priced at £1 less than its immediate competition? What is

the basis on which Churchill prices this product? Each of the methods of pricing has its advantages and disadvantages. Using

cost plus may create an illusion of security in that all costs are covered, but at the same time raises issues as to whether

relevant costs have been included and allocated. Should the company price in anticipation of cost reductions as volume

increases? Should the basis for pricing be what your competitors are charging? As a luxury product one would assume that

its demand is relatively price inelastic: a significant increase in price e.g. £1 would lead to only a small reduction in quantity

demanded. Certainly, profit margins would be enhanced to help provide the financial resources the company needs if it is to

grow. One interesting issue on pricing is the extent to which it is pursuing a price skimming or price penetration policy –

evidence from the scenario suggests more of a price skimming policy in line with the luxury nature of the product.

Place is an equally important issue – the vertical integration strategy of the company has led to company-owned shops being

the main way customers can buy the product. At the same time, this distribution strategy has led to Churchill’s sales being

largely confined to one region in the UK – although it is the most populous. If Churchill has a desire to grow, does it do this

through expanding the number of company owned and franchised outlets or look for other channels of distribution in

particular the increasingly dominant supermarket chains? Each distribution strategy will have significant implications for other

elements in the marketing mix and for the resources and capabilities required in the company.

Finally, promotion is an interesting issue for the company. The relatively recent appointment of a sales and marketing director

perhaps reflects a need to balance the previous dominance of the manufacturing side of the business. Certainly there is

evidence to suggest that John Churchill is not convinced of the need to advertise. There are some real concerns about how

the brand is developed and promoted. Certainly sponsorship is now seen as a key part of the firm’s promotional strategy. The

company has a good reputation but customer access to the product is fairly limited. Overall there is scope for the company

to critically review its marketing mix and implement a very different mix if it wants to grow.

The four Ps above are very much the ‘hard’ elements in the marketing mix and Churchill in its desire to grow will need toensure that the ‘softer’ elements of people, physical evidence and processes are aligned to its ambitious strategy.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-02-26

- 2020-03-27

- 2020-02-06

- 2020-02-06

- 2020-01-09

- 2020-04-05

- 2020-03-08

- 2020-05-12

- 2020-04-23

- 2020-02-06

- 2020-05-09

- 2020-01-09

- 2020-01-14

- 2020-01-09

- 2020-03-14

- 2020-03-15

- 2021-05-23

- 2020-03-07

- 2020-04-05

- 2020-05-15

- 2020-04-07

- 2020-01-11

- 2020-03-05

- 2020-04-07

- 2019-12-27

- 2020-02-20

- 2020-01-09

- 2020-04-17

- 2020-01-09

- 2020-05-13