2020年陕西省ACCA国际会计师考场规则,可以带计算器!

发布时间:2020-01-09

ACCA考场规则是什么呢?跟国内考试的规定有区别吗?这些问题是许多即将参加2020年3月份ACCA考试的同学们最关心的问题,害怕自己辛辛苦苦准备了几个月之久的考试就因为一个不小心触犯了相关的规定,那就得不偿失了。接下来,51题库考试学习网为大家盘点历年来ACCA考试的相关规定,希望大家引以为戒,小心不要触犯哟~

具体点来说,ACCA考试的考场规则主要分为两部分,一个就是进入考场前,另一个就是进入考场之后

ACCA考前规则:

1.考生须在开始考试之前30分钟到达ACCA考试地点,以免在出现突发情况。监考老师对考生进行核查考生本人身份证、ACCA注册号。

2.考生可选择开考前进行网上测试(见机考中心通知),也可选择开考前1小时到达考点,在机考中心进行测试,熟悉机考流程。(建议考生最好选择前者,后者可能出现在机考中心测试的人数太多而不能及时测试导致不熟悉机考流程的情况)

3.考生在考试开始前15分钟经过监考老师批准方可进入考场。逾时不得再进入考场。

4. 考生在到达考场并进行签到后,如因特殊原因需要离场,请主动联系监考人员,不得擅自离开,经过监考老师允许之后才可以离开。

5. 最好不要携带贵重物品前往考场,丢失了后果自负的。

注意:ACCA机考必须带那些东西

首先是自行在官网上打印的准考证其次就是身份证再是可以携带不带有记忆存储功能的计算器。(如考生有携带手机、包包等私人物品,请将其放至监考老师指定区域。)

进入考场后的规则

1.考生进入考场后必须把考试相关书籍材料等放到指定位置,并将手机等通讯设备关闭。考生只允许携带考试规定携带的东西进入考场,例如本人身份证、笔、单功能计算器进入考场,一经发现,按作弊处理。

2.考试开始前,监考人员会宣读考场纪律;考生需要在电脑上输入个人信息,监考人员会核对考生的身份;身份核对后,电脑上会显示出3页考试操作指南,考生仔细阅读,阅读完毕之后,举手向监控人员请示,得到监考人员的允许后才可点击考试科目,开始考试。

3.考试开始时,题目会直接在屏幕上显示,请直接在电脑上输入答案。不能点开电脑里的其他软件

4.考试结束后,需要打印2份考试成绩通知单,自己保留一份,机考中心保留一份。

5.机考中心会在考试结束后上传考试成绩,72小时内成绩会上传到考生的MYACCA成绩记录中。

6.考试费用一旦交付,如因考生自身原因缺考,作弃权处理,不须考虑退款事宜。因此建议各位考生要谨慎报名,毕竟考试费用也是一笔不小的费用。

7.ACCA机考中心保留因不可抗力因素(如网络问题,停电等)调整机考时间或取消考试的权力。出现了以上情况,及时向监考人员反映,他们会为你解决问题。

迟到及提早交卷规定:

在开考后1小时内到达的迟到考生可以入场,但不能补偿考试时间。简单的来说就是即便是晚到1小时,你的考试时间也不会往后延时1小时,交卷铃声响起你同样得交卷。而开考1小时以后到达的考生就算做放弃此次考试,不能入场。

这些考场规则有没有帮助到各位ACCAer们呀?相信大家看了之后或多或少对ACCA考场规则都有了一定的了解,51题库考试学习网提醒大家,认真阅读考场规则,如果和上面所述的规则有一定的出入,各地的相关考场规则以各地的为准,最后51题库考试学习网预祝大家考试顺利上岸~

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) For this part, assume today’s date is 1 May 2010.

Bill and Ben decided not to sell their company, and instead expanded the business themselves. Ben, however,

is now pursuing other interests, and is no longer involved with the day to day activities of Flower Limited. Bill

believes that the company would be better off without Ben as a voting shareholder, and wishes to buy Ben’s

shares. However, Bill does not have sufficient funds to buy the shares himself, and so is wondering if the

company could acquire the shares instead.

The proposed price for Ben’s shares would be £500,000. Both Bill and Ben pay income tax at the higher rate.

Required:

Write a letter to Ben:

(1) stating the income tax (IT) and/or capital gains tax (CGT) implications for Ben if Flower Limited were to

repurchase his 50% holding of ordinary shares, immediately in May 2010; and

(2) advising him of any available planning options that might improve this tax position. Clearly explain any

conditions which must be satisfied and quantify the tax savings which may result.

(13 marks)

Assume that the corporation tax rates for the financial year 2005 and the income tax rates and allowances

for the tax year 2005/06 apply throughout this question.

(b) [Ben’s address] [Firm’s address]

Dear Ben [Date]

A company purchase of own shares can be subject to capital gains treatment if certain conditions are satisfied. However, one

of these conditions is that the shares in question must have been held for a minimum period of five years. As at 1 May 2010,

your shares in Flower Limited have only been held for four years and ten months. As a result, the capital gains treatment will

not apply.

In the absence of capital gains treatment, the position on a company repurchase of its own shares is that the payment will

be treated as an income distribution (i.e. a dividend) in the hands of the recipient. The distribution element is calculated as

the proceeds received for the shares less the price paid for them. On the basis that the purchase price is £500,000, then the

element of distribution will be £499,500 (500,000 – 500). This would be taxed as follows:

(b) Discuss how the operating statement you have produced can assist managers in:

(i) controlling variable costs;

(ii) controlling fixed production overhead costs. (8 marks)

(b) Controlling variable costs

The first step in the process of controlling costs is to measure actual costs. The second step is to calculate variances that show

the difference between actual costs and budgeted or standard costs. These variances then need to be reported to those

managers who have responsibility for them. These managers can then decide whether action needs to be taken to bring actual

costs back into line with budgeted or standard costs. The operating statement therefore has a role to play in reporting

information to management in a way that assists in the decision-making process.

The operating statement quantifies the effect of the volume difference between budgeted and actual sales so that the actual

cost of the actual output can be compared with the standard (or budgeted) cost of the actual output. The statement clearly

differentiates between adverse and favourable variances so that managers can identify areas where there is a significant

difference between actual results and planned performance. This supports management by exception, since managers can

focus their efforts on these significant areas in order to obtain the most impact in terms of getting actual operations back in

line with planned activity.

In control terms, variable costs can be affected in the short term and so an operating statement for the last month showing

variable cost variances will highlight those areas where management action may be effective. In the short term, for example,

managers may be able to improve labour efficiency through training, or through reducing or eliminating staff actions which

do not assist the production process. In this way the adverse direct labour efficiency variance of £252, which is 7·3% of the

standard direct labour cost of the actual output, could be reduced.

Controlling fixed production overhead costs

In the short term, it is unlikely that fixed production overhead costs can be controlled. An operating statement from last month

showing fixed production overhead variances may not therefore assist in controlling fixed costs. Managers will not be able to

take any action to correct the adverse fixed production overhead expenditure variance, for example, which may in fact simply

show the need for improvement in the area of budget planning. Investigation of the component parts of fixed production

overhead will show, however, whether any of these are controllable. In general, this is not the case2.

Absorption costing gives rise to a fixed production overhead volume variance, which shows the effect of actual production

being different from planned production. Since fixed production overheads are a sunk cost, the volume variance shows little

more than that the standard hours for actual production were different from budgeted standard hours3. Similarly, the fixed

production overhead efficiency variance offers little more in information terms than the direct labour efficiency variance. While

fixed production overhead variances assist in reconciling budgeted profit with actual profit, therefore, their reporting in an

operating statement is unlikely to assist in controlling fixed costs.

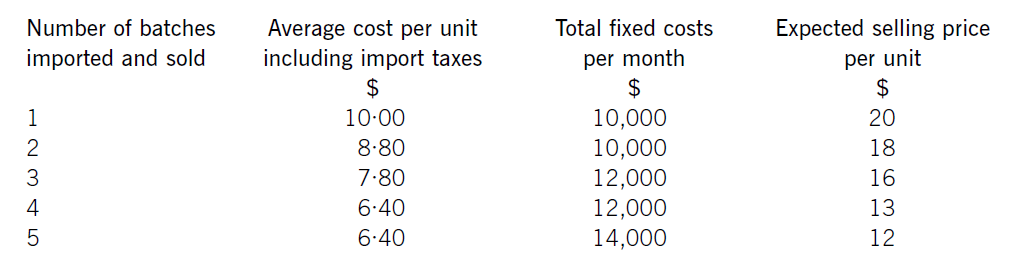

Jewel Co is setting up an online business importing and selling jewellery headphones. The cost of each set of headphones varies depending on the number purchased, although they can only be purchased in batches of 1,000 units. It also has to pay import taxes which vary according to the quantity purchased.

Jewel Co has already carried out some market research and identified that sales quantities are expected to vary depending on the price charged. Consequently, the following data has been established for the first month:

Required:

(a) Calculate how many batches Jewel Co should import and sell. (6 marks)

(b) Explain why Jewel Co could not use the algebraic method to establish the optimum price for its product.

(4 marks)

(b)Thealgebraicmodelrequiresseveralassumptionstobetrue.First,theremustbeaconsistentrelationshipbetweenprice(P)anddemand(Q),sothatademandequationcanbeestablished,usuallyintheform.P=a–bQ.Here,althoughthereisaclearrelationshipbetweenthetwo,itisnotaperfectlylinearrelationshipandsomorecomplicatedtechniquesarerequiredtocalculatethedemandequation.ItalsocannotbeassumedthatalinearrelationshipwillholdforallvaluesofPandQotherthanthefivegiven.Similarly,theremustbeaclearrelationshipbetweendemandandmarginalcost,usuallysatisfiedbyconstantvariablecostperunitandconstantfixedcosts.Thechangingvariablecostsperunitagaincomplicatetheissue,butitisthechangesinfixedcostswhichmakethealgebraicmethodlessusefulinJewel’scase.Thealgebraicmodelisonlysuitableforcompaniesoperatinginamonopolyanditisnotclearherewhetherthisisthecase,butitseemsunlikely,soany‘optimum’pricemightbecomeirrelevantifJewel’scompetitorschargesignificantlylowerprices.Othermoregeneralfactorsnotconsideredbythealgebraicmodelarepoliticalfactorswhichmightaffectimports,socialfactorswhichmayaffectcustomertastesandeconomicfactorswhichmayaffectexchangeratesorcustomerspendingpower.Thereliabilityoftheestimatesthemselves–forsalesprices,variablecostsandfixedcosts–couldalsobecalledintoquestion.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-09

- 2020-01-09

- 2020-02-21

- 2020-01-01

- 2020-03-17

- 2020-01-09

- 2020-04-02

- 2020-03-18

- 2020-01-09

- 2020-01-09

- 2020-05-10

- 2020-04-29

- 2020-01-09

- 2020-04-05

- 2019-07-19

- 2020-01-09

- 2020-05-15

- 2020-02-04

- 2020-05-14

- 2020-01-09

- 2020-03-26

- 2020-03-22

- 2020-01-01

- 2020-05-05

- 2020-05-07

- 2020-01-09

- 2020-01-09

- 2020-04-08

- 2020-02-12

- 2020-05-20