哪些人报考ACCA可以申请免试,本篇文章来告诉你!

发布时间:2020-03-05

ACCA在国内称为"国际注册会计师",实际上是英国的注册会计师协会之一(英国有多家注册会计师协会),但它是英国具有特许头衔的4家注册会计师协会之一,也是当今知名的国际性会计师组织之一。考ACCA很多人都享有一定科目的免试,但是各专业免试政策不一样,那么,接下来一起看看具体内容吧!

ACCA对于中国学员的免试政策详情如下:

如何申请ACCA免试?

登录ACCA官网(https://www.accaglobal.com/gb/en.html),填写申请表向官方发邮件即可,已注册成功的学员,在获得相关可申请免试的证书(例如会计学位、CPA证书)后可向ACCA申请追加免试,申请流程:

1、填写免试申请表《Exemption

Application Form》。

2、将申请表、证书的原件和翻译件以电子版形式发送至students accaglobal.com。

3、请注意查收邮件或登录MYACCA学员账户查看最新免试信息。

4、1月15日前提交申请,6月考试生效;7月15日前提交申请,12月考试生效。

好的,以上就是今天51题库考试学习网为大家分享的全部内容,大家是否清楚了呢?希望本篇文章能够帮助到大家,如果大家还有什么疑问,欢迎大家前来咨询51题库考试学习网,我们会第一时间为大家答疑解惑。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(iii) Explain the potential corporation tax (CT) implications of Tay Limited transferring work to Trent Limited,

and suggest how these can be minimised or eliminated. (3 marks)

(iii) Trading losses may not be carried forward where, within a period of three years there is both a change in the ownership

of a company and a major change in the nature or conduct of its trade. The transfer of work from Tay Limited to Trent

Limited is likely to constitute a major change in the nature or conduct of the latter’s trade. As a consequence, any tax

losses at the date of acquisition will be forfeited. Assuming losses were incurred uniformly in 2005, the tax losses at the

date of acquisition were £380,000 (300,000 + 2/3 x 120,000)). This is worth £114,000 assuming a corporation tax

rate of 30%.

Thus, Tay Limited should not consider transferring any trade to Trent Limited until after the third anniversary of the date

of the change of ownership i.e. not before 1 September 2008. As the trades are similar, there should be little problem

in transferring work from that date onwards.

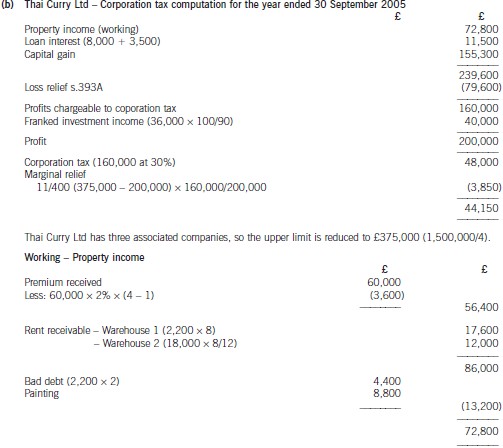

(b) Assuming that Thai Curry Ltd claims relief for its trading loss against total profits under s.393A ICTA 1988,calculate the company’s corporation tax liability for the year ended 30 September 2005. (10 marks)

(b) Explain the matters you should consider before accepting an engagement to conduct a due diligence review

of MCM. (10 marks)

(b) Matters to be considered (before accepting the engagement)

Tutorial note: Although candidates may approach this part from a rote-learned list of ‘matters to consider’ it is important

that answer points be tailored, in so far as the information given in the scenario permits, to the specifics of Plaza and MCM.

It is critical that answer points should not contradict the scenario (e.g. assuming that it is Plaza’s auditor who has been

asked to undertake the assignment).

■ Information about Duncan Seymour – What is the relationship of the chief finance officer to Plaza (e.g. is he on the

management board)? By what authority is he approaching Andando to undertake this assignment?

■ The purpose of the assignment must be clarified. Duncan’s approach to Andando is ‘to advise on a bid’. However,

Andando cannot make executive decisions for a client but only provide the facts of material interest. Plaza’s

management must decide whether or not to bid and, if so, how much to bid.

■ The scope of the due diligence review. It seems likely that Plaza will be interested in acquiring all of MCM’s business

as its areas of operation coincide with Plaza’s. However it must be confirmed that Plaza is not merely interested in

acquiring only the National or International business of MCM.

■ Andando’s competence and experience – Andando should not accept the engagement unless the firm has experience in

undertaking due diligence assignments. Even then, the firm must have sufficient knowledge of the territories in which

the businesses operate to evaluate whether all facts of material interest to Plaza have been identified.

Tutorial note: Candidates should be querying their competence and experience in the fields of retailing and training

as though they were dealing with highly regulated or specialist industries such as banking or insurance.

■ Whether Andando has sufficient resources (e.g. representative/associated offices), if any, in Europe and Asia to

investigate MCM’s International business.

■ Any factors which might impair Andando’s objectivity in reporting to Plaza the facts uncovered by the due diligence

review. For example, if Duncan is closely connected with a partner in Andando or if Andando is the auditor of Frontiers.

Tutorial note: Candidates will not be awarded marks for going into ‘autopilot’ on independence issues. For example,

this is a one-off assignment so size of fee is not relevant. Andando holding shares in MCM is not possible (since whollyowned).

■ Plaza’s rationale for wishing to acquire MCM. Presumably it is significant that MCM operates in the same territories as

Plaza. Plaza may be wanting to provide extensive training programs in management, communications and marketing

to its workforce.

■ The relationship, if any, between Plaza and MCM in any of the territories. Plaza may be a major client of MCM. That

is, Plaza is currently out-sourcing training to MCM. Acquiring MCM would bring training in-house.

Tutorial note: Ascertaining what a purchaser hopes to gain from an acquisition before the assignment is accepted is

important. The facts to be uncovered for a merger from which synergy is expected will be different from those relevant

to acquiring an investment opportunity.

■ Time available – Andando must have sufficient time to find all facts that would be of material interest to Plaza before

disclosing their findings.

■ The acceptability of any limitations – whether there will be restrictions on Andando’s access to information held by MCM

(e.g. if there will not be access to board minutes) and personnel.

■ The degree of secrecy required – this may go beyond the normal duties of confidentiality not to disclose information to

outsiders (e.g. if unannounced staff redundancies could arise).

■ Why Plaza’s current auditors have not been asked to conduct the due diligence review – especially as they are

responsible for (and therefore capable of undertaking) the group audit covering the relevant countries.

■ Andando should be allowed to communicate with Plaza’s current auditor:

– to inform. them of the nature of the work they have been asked to undertake; and

– to enquire if there is any reason why they should not accept this assignment.

■ In taking on Plaza as a new client Andando may have a later opportunity to offer external audit and other services to

Plaza (e.g. internal audit).

(b) Explain what effect the acquisition of Di Rollo Co will have on the planning of your audit of the consolidated

financial statements of Murray Co for the year ending 31 March 2008. (10 marks)

(b) Effect of acquisition on planning the audit of Murray’s consolidated financial statements for the year ending 31 March

2008

Group structure

The new group structure must be ascertained to identify all entities that should be consolidated into the Murray group’s

financial statements for the year ending 31 March 2008.

Materiality assessment

Preliminary materiality for the group will be much higher, in monetary terms, than in the prior year. For example, if a % of

total assets is a determinant of the preliminary materiality, it may be increased by 10% (as the fair value of assets acquired,

including goodwill, is $2,373,000 compared with $21·5m in Murray’s consolidated financial statements for the year ended

31 March 2007).

The materiality of each subsidiary should be re-assessed, in terms of the enlarged group as at the planning stage. For

example, any subsidiary that was just material for the year ended 31 March 2007 may no longer be material to the group.

This assessment will identify, for example:

– those entities requiring an audit visit; and

– those entities for which substantive analytical procedures may suffice.

As Di Rollo’s assets are material to the group Ross should plan to inspect the South American operations. The visit may

include a meeting with Di Rollo’s previous auditors to discuss any problems that might affect the balances at acquisition and

a review of the prior year audit working papers, with their permission.

Di Rollo was acquired two months into the financial year therefore its post-acquisition results should be expected to be

material to the consolidated income statement.

Goodwill acquired

The assets and liabilities of Di Rollo at 31 March 2008 will be combined on a line-by-line basis into the consolidated financial

statements of Murray and goodwill arising on acquisition recognised.

Audit work on the fair value of the Di Rollo brand name at acquisition, $600,000, may include a review of a brand valuation

specialist’s working papers and an assessment of the reasonableness of assumptions made.

Significant items of plant are likely to have been independently valued prior to the acquisition. It may be appropriate to plan

to place reliance on the work of expert valuers. The fair value adjustment on plant and equipment is very high (441% of

carrying amount at the date of acquisition). This may suggest that Di Rollo’s depreciation policies are over-prudent (e.g. if

accelerated depreciation allowed for tax purposes is accounted for under local GAAP).

As the amount of goodwill is very material (approximately 50% of the cash consideration) it may be overstated if Murray has

failed to recognise any assets acquired in the purchase of Di Rollo in accordance with IFRS 3 Business Combinations. For

example, Murray may have acquired intangible assets such as customer lists or franchises that should be recognised

separately from goodwill and amortised (rather than tested for impairment).

Subsequent impairment

The audit plan should draw attention to the need to consider whether the Di Rollo brand name and goodwill arising have

suffered impairment as a result of the allegations against Di Rollo’s former chief executive.

Liabilities

Proceedings in the legal claim made by Di Rollo’s former chief executive will need to be reviewed. If the case is not resolved

at 31 March 2008, a contingent liability may require disclosure in the consolidated financial statements, depending on the

materiality of amounts involved. Legal opinion on the likelihood of Di Rollo successfully defending the claim may be sought.

Provision should be made for any actual liabilities, such as legal fees.

Group (related party) transactions and balances

A list of all the companies in the group (including any associates) should be included in group audit instructions to ensure

that intra-group transactions and balances (and any unrealised profits and losses on transactions with associates) are

identified for elimination on consolidation. Any transfer pricing policies (e.g. for clothes manufactured by Di Rollo for Murray

and sales of Di Rollo’s accessories to Murray’s retail stores) must be ascertained and any provisions for unrealised profit

eliminated on consolidation.

It should be confirmed at the planning stage that inter-company transactions are identified as such in the accounting systems

of all companies and that inter-company balances are regularly reconciled. (Problems are likely to arise if new inter-company

balances are not identified/reconciled. In particular, exchange differences are to be expected.)

Other auditors

If Ross plans to use the work of other auditors in South America (rather than send its own staff to undertake the audit of Di

Rollo), group instructions will need to be sent containing:

– proforma statements;

– a list of group and associated companies;

– a statement of group accounting policies (see below);

– the timetable for the preparation of the group accounts (see below);

– a request for copies of management letters;

– an audit work summary questionnaire or checklist;

– contact details (of senior members of Ross’s audit team).

Accounting policies

Di Rollo may have material accounting policies which do not comply with the rest of the Murray group. As auditor to Di Rollo,

Ross will be able to recalculate the effect of any non-compliance with a group accounting policy (that Murray’s management

would be adjusting on consolidation).

Timetable

The timetable for the preparation of Murray’s consolidated financial statements should be agreed with management as soon

as possible. Key dates should be planned for:

– agreement of inter-company balances and transactions;

– submission of proforma statements;

– completion of the consolidation package;

– tax review of group accounts;

– completion of audit fieldwork by other auditors;

– subsequent events review;

– final clearance on accounts of subsidiaries;

– Ross’s final clearance of consolidated financial statements.

Tutorial note: The order of dates is illustrative rather than prescriptive.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-11

- 2019-07-19

- 2020-04-20

- 2020-05-12

- 2019-12-29

- 2020-01-09

- 2020-03-07

- 2020-02-04

- 2020-01-09

- 2020-02-18

- 2020-05-20

- 2020-04-22

- 2020-02-21

- 2020-01-09

- 2020-02-19

- 2020-04-04

- 2020-01-09

- 2020-04-17

- 2019-07-19

- 2019-07-19

- 2020-01-10

- 2020-03-21

- 2020-05-13

- 2020-01-09

- 2020-01-04

- 2020-05-03

- 2020-05-12

- 2020-01-09

- 2020-05-10

- 2020-05-15