解答!为什么有人舍弃国内的注会,而选择报考国际注册会计师呢

发布时间:2020-04-15

在中国,有着中国的会计师资格CIPA,在国外有着ACCA这样的国际注册会计师。其实,各国家都有着自己的会计师认证考试,但为什么还是有人舍弃国内的注会,而选择报考国际注册会计师呢?51题库考试学习网在这里为大家进行详细解答!

1、ACCA工作领域更广泛

ACCA考试是按现代企业财务人员需要具备的技能和技术的要求而设计的,其课程所涵盖的不仅仅包含会计、审计方面的专业知识,也同时涵盖人力资源、公司管理、战略决策、法务、税务、业绩衡量、财务管理、职业道德等方面的知识体系。将为学习的学员提供完整的国际商业知识结构,无论ACCA的学员是否直接从事财务工作,或是从事管理,销售,人力资源,金融工程等工作,无论从事何种行业,均将受益于ACCA的完善知识结构!

2、薪资待遇丰厚

ACCA学员到企业工作平均年薪能在15~30万之间。一些猎头公司在帮助企业找人的时候都明确表示首先要ACCA学员,然后看相关工作经验,如果有外资公司、四大会计师事务所工作经验的更受青睐。如果有会计师事务所培训的背景,容易拿到高薪,一般都能做到财务经理以上这样的职位。

3、英语水平是门槛

尽管ACCA学员有很好的就业前景,但不是说每个人都适合考ACCA。ACCA实行的是宽进严出的政策。英语水平是考ACCA的首道门槛。虽然没有硬性规定英语要在6级以上,但是建议达到英语四级这个水平。因为考试、答题是全英文的。ACCA共分为三个阶段13门课程,每次考试最多只能报考四门,所以,按最理想化的方式计算,通过所有的考试,最短也要花上将近三年的时间。

4、晋升空间充足

虽然在中国,ACCA是没有签字权,但是被看好是因为ACCA是晋升的途径。在会计师事务所工作分工明确,多数是希望有中注协资格的,因为这样有利于吸引客户。但作为自己晋升这方面,ACCA还是被很多海外回来的人认可。同时,事务所有持有国际证书的人,也有利于服务客户,例如海外上市的时候,因为海外上市报表必须按国际会计准则来编制,国内会计师无法胜任。

今日分享时间到此结束啦,如果大家觉得意犹未尽,还想了解更多内容的话,敬请关注51题库考试学习网。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) Explain the matters you should consider before accepting an engagement to conduct a due diligence review

of MCM. (10 marks)

(b) Matters to be considered (before accepting the engagement)

Tutorial note: Although candidates may approach this part from a rote-learned list of ‘matters to consider’ it is important

that answer points be tailored, in so far as the information given in the scenario permits, to the specifics of Plaza and MCM.

It is critical that answer points should not contradict the scenario (e.g. assuming that it is Plaza’s auditor who has been

asked to undertake the assignment).

■ Information about Duncan Seymour – What is the relationship of the chief finance officer to Plaza (e.g. is he on the

management board)? By what authority is he approaching Andando to undertake this assignment?

■ The purpose of the assignment must be clarified. Duncan’s approach to Andando is ‘to advise on a bid’. However,

Andando cannot make executive decisions for a client but only provide the facts of material interest. Plaza’s

management must decide whether or not to bid and, if so, how much to bid.

■ The scope of the due diligence review. It seems likely that Plaza will be interested in acquiring all of MCM’s business

as its areas of operation coincide with Plaza’s. However it must be confirmed that Plaza is not merely interested in

acquiring only the National or International business of MCM.

■ Andando’s competence and experience – Andando should not accept the engagement unless the firm has experience in

undertaking due diligence assignments. Even then, the firm must have sufficient knowledge of the territories in which

the businesses operate to evaluate whether all facts of material interest to Plaza have been identified.

Tutorial note: Candidates should be querying their competence and experience in the fields of retailing and training

as though they were dealing with highly regulated or specialist industries such as banking or insurance.

■ Whether Andando has sufficient resources (e.g. representative/associated offices), if any, in Europe and Asia to

investigate MCM’s International business.

■ Any factors which might impair Andando’s objectivity in reporting to Plaza the facts uncovered by the due diligence

review. For example, if Duncan is closely connected with a partner in Andando or if Andando is the auditor of Frontiers.

Tutorial note: Candidates will not be awarded marks for going into ‘autopilot’ on independence issues. For example,

this is a one-off assignment so size of fee is not relevant. Andando holding shares in MCM is not possible (since whollyowned).

■ Plaza’s rationale for wishing to acquire MCM. Presumably it is significant that MCM operates in the same territories as

Plaza. Plaza may be wanting to provide extensive training programs in management, communications and marketing

to its workforce.

■ The relationship, if any, between Plaza and MCM in any of the territories. Plaza may be a major client of MCM. That

is, Plaza is currently out-sourcing training to MCM. Acquiring MCM would bring training in-house.

Tutorial note: Ascertaining what a purchaser hopes to gain from an acquisition before the assignment is accepted is

important. The facts to be uncovered for a merger from which synergy is expected will be different from those relevant

to acquiring an investment opportunity.

■ Time available – Andando must have sufficient time to find all facts that would be of material interest to Plaza before

disclosing their findings.

■ The acceptability of any limitations – whether there will be restrictions on Andando’s access to information held by MCM

(e.g. if there will not be access to board minutes) and personnel.

■ The degree of secrecy required – this may go beyond the normal duties of confidentiality not to disclose information to

outsiders (e.g. if unannounced staff redundancies could arise).

■ Why Plaza’s current auditors have not been asked to conduct the due diligence review – especially as they are

responsible for (and therefore capable of undertaking) the group audit covering the relevant countries.

■ Andando should be allowed to communicate with Plaza’s current auditor:

– to inform. them of the nature of the work they have been asked to undertake; and

– to enquire if there is any reason why they should not accept this assignment.

■ In taking on Plaza as a new client Andando may have a later opportunity to offer external audit and other services to

Plaza (e.g. internal audit).

(ii) Discuss TWO problems that may be faced in implementing quality control procedures in a small firm of

Chartered Certified Accountants, and recommend how these problems may be overcome. (4 marks)

(ii) Consultation – it may not be possible to hold extensive consultations on specialist issues within a small firm, due to a

lack of specialist professionals. There may be a lack of suitably experienced peers to discuss issues arising on client

engagements. Arrangements with other practices for consultation may be necessary.

Training/Continuing Professional Development (CPD) – resources may not be available, and it is expensive to establish

an in-house training function. External training consortia can be used to provide training/CPD for qualified staff, and

training on non-exam related issues for non-qualified staff.

Review procedures – it may not be possible to hold an independent review of an engagement within the firm due to the

small number of senior and experienced auditors. In this case an external review service may be purchased.

Lack of specialist experience – where special skills are needed within an engagement; the skills may be bought in, for

example, by seconding staff from another practice. Alternatively if work is too specialised for the firm, the work could be

sub-contracted to another practice.

Working papers – the firm may lack resources to establish an in-house set of audit manuals or standard working papers.

In this case documentation can be provided by external firms or professional bodies.

Moonstar Co is a property development company which is planning to undertake a $200 million commercial property development. Moonstar Co has had some difficulties over the last few years, with some developments not generating the expected returns and the company has at times struggled to pay its finance costs. As a result Moonstar Co’s credit rating has been lowered, affecting the terms it can obtain for bank finance. Although Moonstar Co is listed on its local stock exchange, 75% of the share capital is held by members of the family who founded the company. The family members who are shareholders do not wish to subscribe for a rights issue and are unwilling to dilute their control over the company by authorising a new issue of equity shares. Moonstar Co’s board is therefore considering other methods of financing the development, which the directors believe will generate higher returns than other recent investments, as the country where Moonstar Co is based appears to be emerging from recession.

Securitisation proposals

One of the non-executive directors of Moonstar Co has proposed that it should raise funds by means of a securitisation process, transferring the rights to the rental income from the commercial property development to a special purpose vehicle. Her proposals assume that the leases will generate an income of 11% per annum to Moonstar Co over a ten-year period. She proposes that Moonstar Co should use 90% of the value of the investment for a collateralised loan obligation which should be structured as follows:

– 60% of the collateral value to support a tranche of A-rated floating rate loan notes offering investors LIBOR plus 150 basis points

– 15% of the collateral value to support a tranche of B-rated fixed rate loan notes offering investors 12%

– 15% of the collateral value to support a tranche of C-rated fixed rate loan notes offering investors 13%

– 10% of the collateral value to support a tranche as subordinated certificates, with the return being the excess of receipts over payments from the securitisation process

The non-executive director believes that there will be sufficient demand for all tranches of the loan notes from investors. Investors will expect that the income stream from the development to be low risk, as they will expect the property market to improve with the recession coming to an end and enough potential lessees to be attracted by the new development.

The non-executive director predicts that there would be annual costs of $200,000 in administering the loan. She acknowledges that there would be interest rate risks associated with the proposal, and proposes a fixed for variable interest rate swap on the A-rated floating rate notes, exchanging LIBOR for 9·5%.

However the finance director believes that the prediction of the income from the development that the non-executive director has made is over-optimistic. He believes that it is most likely that the total value of the rental income will be 5% lower than the non-executive director has forecast. He believes that there is some risk that the returns could be so low as to jeopardise the income for the C-rated fixed rate loan note holders.

Islamic finance

Moonstar Co’s chief executive has wondered whether Sukuk finance would be a better way of funding the development than the securitisation.

Moonstar Co’s chairman has pointed out that a major bank in the country where Moonstar Co is located has begun to offer a range of Islamic financial products. The chairman has suggested that a Mudaraba contract would be the most appropriate method of providing the funds required for the investment.

Required:

(a) Calculate the amounts in $ which each of the tranches can expect to receive from the securitisation arrangement proposed by the non-executive director and discuss how the variability in rental income affects the returns from the securitisation. (11 marks)

(b) Discuss the benefits and risks for Moonstar Co associated with the securitisation arrangement that the non-executive director has proposed. (6 marks)

(c) (i) Discuss the suitability of Sukuk finance to fund the investment, including an assessment of its appeal to potential investors. (4 marks)

(ii) Discuss whether a Mudaraba contract would be an appropriate method of financing the investment and discuss why the bank may have concerns about providing finance by this method. (4 marks)

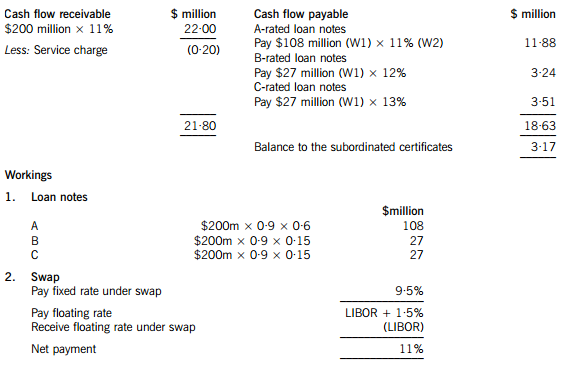

(a) An annual cash flow account compares the estimated cash flows receivable from the property against the liabilities within the securitisation process. The swap introduces leverage into the arrangement.

The holders of the certificates are expected to receive $3·17million on $18 million, giving them a return of 17·6%. If the cash flows are 5% lower than the non-executive director has predicted, annual revenue received will fall to $20·90 million, reducing the balance available for the subordinated certificates to $2·07 million, giving a return of 11·5% on the subordinated certificates, which is below the returns offered on the B and C-rated loan notes. The point at which the holders of the certificates will receive nothing and below which the holders of the C-rated loan notes will not receive their full income will be an annual income of $18·83 million (a return of 9·4%), which is 14·4% less than the income that the non-executive director has forecast.

(b) Benefits

The finance costs of the securitisation may be lower than the finance costs of ordinary loan capital. The cash flows from the commercial property development may be regarded as lower risk than Moonstar Co’s other revenue streams. This will impact upon the rates that Moonstar Co is able to offer borrowers.

The securitisation matches the assets of the future cash flows to the liabilities to loan note holders. The non-executive director is assuming a steady stream of lease income over the next 10 years, with the development probably being close to being fully occupied over that period.

The securitisation means that Moonstar Co is no longer concerned with the risk that the level of earnings from the properties will be insufficient to pay the finance costs. Risks have effectively been transferred to the loan note holders.

Risks

Not all of the tranches may appeal to investors. The risk-return relationship on the subordinated certificates does not look very appealing, with the return quite likely to be below what is received on the C-rated loan notes. Even the C-rated loan note holders may question the relationship between the risk and return if there is continued uncertainty in the property sector.

If Moonstar Co seeks funding from other sources for other developments, transferring out a lower risk income stream means that the residual risks associated with the rest of Moonstar Co’s portfolio will be higher. This may affect the availability and terms of other borrowing.

It appears that the size of the securitisation should be large enough for the costs to be bearable. However Moonstar Co may face unforeseen costs, possibly unexpected management or legal expenses.

(c) (i) Sukuk finance could be appropriate for the securitisation of the leasing portfolio. An asset-backed Sukuk would be the same kind of arrangement as the securitisation, where assets are transferred to a special purpose vehicle and the returns and repayments are directly financed by the income from the assets. The Sukuk holders would bear the risks and returns of the relationship.

The other type of Sukuk would be more like a sale and leaseback of the development. Here the Sukuk holders would be guaranteed a rental, so it would seem less appropriate for Moonstar Co if there is significant uncertainty about the returns from the development.

The main issue with the asset-backed Sukuk finance is whether it would be as appealing as certainly the A-tranche of the securitisation arrangement which the non-executive director has proposed. The safer income that the securitisation offers A-tranche investors may be more appealing to investors than a marginally better return from the Sukuk. There will also be costs involved in establishing and gaining approval for the Sukuk, although these costs may be less than for the securitisation arrangement described above.

(ii) A Mudaraba contract would involve the bank providing capital for Moonstar Co to invest in the development. Moonstar Co would manage the investment which the capital funded. Profits from the investment would be shared with the bank, but losses would be solely borne by the bank. A Mudaraba contract is essentially an equity partnership, so Moonstar Co might not face the threat to its credit rating which it would if it obtained ordinary loan finance for the development. A Mudaraba contract would also represent a diversification of sources of finance. It would not require the commitment to pay interest that loan finance would involve.

Moonstar Co would maintain control over the running of the project. A Mudaraba contract would offer a method of obtaining equity funding without the dilution of control which an issue of shares to external shareholders would bring. This is likely to make it appealing to Moonstar Co’s directors, given their desire to maintain a dominant influence over the business.

The bank would be concerned about the uncertainties regarding the rental income from the development. Although the lack of involvement by the bank might appeal to Moonstar Co's directors, the bank might not find it so attractive. The bank might be concerned about information asymmetry – that Moonstar Co’s management might be reluctant to supply the bank with the information it needs to judge how well its investment is performing.

5 A management accounting focus for performance management in an organisation may incorporate the following:

(1) the determination and quantification of objectives and strategies

(2) the measurement of the results of the strategies implemented and of the achievement of the results through a

number of determinants

(3) the application of business change techniques, in the improvement of those determinants.

Required:

(a) Discuss the meaning and inter-relationship of the terms (shown in bold type) in the above statement. Your

answer should incorporate examples that may be used to illustrate each term in BOTH profit-seeking

organisations and not-for-profit organisations in order to highlight any differences between the two types of

organisation. (14 marks)

5 (a) Objectives may be viewed as profit and market share in a profit-oriented organisation or the achievement of ‘value for money’

in a not-for-profit organisation (NFP). The overall objective of an organisation may be expressed in the wording of its mission

statement.

In order to achieve the objectives, long-term strategies will be required. In a profit-oriented organisation, this may incorporate

the evaluation of strategies that might include price reductions, product design changes, advertising campaign, product mix

change and methods changes, embracing change techniques such as BPR, JIT, TQM and ABM. In NFP situations, strategies

might address the need to achieve ‘economy’ through reduction in average cost per unit; ‘efficiency’ through maximisation of

the input:output ratio, whilst checking on ‘effectiveness’ through monitoring whether the objectives are achieved.

The annual budget will quantify the short-term results anticipated of the strategies. These results may be seen as the level of

financial performance and competitiveness achieved. This quantification may be compared with previous years and with

actual performance on an ongoing basis. Financial performance may be measured in terms of profit, liquidity, capital structure

and a range of ratios. Competitiveness may be measured by sales growth, market share and the number of new customers.

In a not-for-profit organisation, the results may be monitored by checking on the effectiveness of actions aimed at the

achievement of the objectives. For instance, the effectiveness of a University may be measured by the number of degrees

awarded and the grades achieved. The level of student ‘drop-outs’ each year may also be seen as a measure of ineffectiveness.

The determinants of results may consist of a number of measures. These may include the level of quality, customer

satisfaction, resource utilisation, innovation and flexibility that are achieved. Such determinants may focus on a range of nonfinancial

measures that may be monitored on an ongoing basis, as part of the feedback information in conjunction with

financial data.

A range of business change techniques may be used to enhance performance management.

Techniques may include:

Business process re-engineering (BPR) which involves the examination of business processes with a view to improving the

way in which each is implemented. A major focus may be on the production cycle, but it will also be applicable in areas such

as the accounting department.

Just-in-time (JIT) which requires commitment to the pursuit of ‘excellence’ in all aspects of an organisation.

Total quality management (TQM) which aims for continuous quality improvement in all aspects of the operation of an

organisation.

Activity based management systems (ABM) which focus on activities that are required in an organisation and the cost drivers

for such activities, with a view to identifying and improving activities that add value and eliminating those activities that do

not add value.

Long-term performance management is likely to embrace elements of BPR, JIT, TQM and ABM. All of these will be reflected

in the annual budget on an ongoing basis.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-03-14

- 2020-01-10

- 2020-01-10

- 2020-02-19

- 2020-01-10

- 2020-04-23

- 2020-04-28

- 2020-05-05

- 2020-04-23

- 2020-04-30

- 2020-01-10

- 2020-01-10

- 2020-05-09

- 2020-01-10

- 2020-01-10

- 2020-01-31

- 2020-04-07

- 2020-03-14

- 2020-01-10

- 2020-01-10

- 2020-02-20

- 2020-01-09

- 2020-01-09

- 2020-01-10

- 2020-04-18

- 2020-03-07

- 2020-01-10

- 2020-01-10

- 2020-04-24

- 2020-05-09