2020年6月ACCA考试时间安排

发布时间:2020-01-02

号外号外!最新出炉2020年6月ACCA考试时间安排,有参加的ACCAer们必须知道,要带上相关证件准时到达哟~

2020年6月ACCA考试季为6月1日-6月5日,ACCA各科目考试都将在这期间进行。每个科目的具体考试日期安排如下:

Monday 1 June AA、AAA

Tuesday 2 June TX、ATX、SBL

Wednesday 3 June PM、APM

Thursday 4 June FR、SBR

Friday 5 June LW、FM、AFMACCA共有四个考季,每个考季又分为三个不同的报名阶段,分别为提前报名阶段、常规报名阶段和最后截止报名阶段。

不同的acca报名阶段中,每科的考试费用是不同的,平均每科的考试费用大约能够优惠一百元及以上,算下来考完ACCA就至少能够帮自己减少一千甚至更多的acca考试费用了。大家可以根据自己的考试安排,最好在早期报名和常规报名截止前报名,那个时候acca报名费用最优惠哦!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

6 Discuss how developments in each of the following areas has affected the scope of the audit and the audit work

undertaken:

(a) fair value accounting; (6 marks)

6 DEVELOPMENTS

General comments

Tutorial note: The following comments, that could be made in respect of any of the three areas of development, will be given

credit only once.

■ Audit scope – the scope of a statutory audit should be as necessary to form. an audit opinion (i.e. unlimited).

■ Audit work undertaken – the nature, timing and extent of audit procedures should be as necessary to implement the overall

audit plan.

(a) Fair value accounting

■ Different definitions of fair value exist (among financial reporting frameworks or for different assets and liabilities within

a particular framework). For example, under IFRS it is ‘the amount for which an asset could be exchanged (or a liability

settled) between knowledgeable, willing parties in an arm’s length transaction’.

■ The term ‘fair value accounting’ is used to describe the measurement and disclosure of assets and/or liabilities at fair

value and the charging to profit and loss (or directly to equity) of any changes in fair value measurements.

■ Fair value accounting concerns measurements and disclosures but not initial recognition of assets and liabilities in

financial statements. It does not then, for example, affect the nature, timing and extent of audit procedures to confirm

the existence and completeness of rights and obligations.

■ Fair value may be determined with varying degrees of subjectivity. For example, there will be little (if any) subjectivity

for assets bought and sold in active and open markets that readily provide reliable information on the prices at which

exchange transactions occur. However, the valuation of assets with unique characteristics (or entity-specific assets) often

requires the projection and discounting of future cash flows.

■ The audit of estimates of fair values based on valuation models/techniques can be approached like other accounting

estimates (in accordance with ISA 540 ‘Audit of Accounting Estimates’). However, although the auditor should be able

to review and test the process used by management to develop the estimate, there may be:

? a much greater need for an independent estimate (and hence greater reliance on the work of experts in accordance

with ISA 620);

? no suitable subsequent events to confirm the estimate made (e.g. for assets that are held for use and not for

trading).

Tutorial note: Consider, for example, how the audit of ‘in-process research and development’ might compare with that

for an allowance for slow-moving inventory.

■ Different financial reporting frameworks require or permit a variety of fair value measures and disclosures in financial

statements. They also vary in the level of guidance provided (to preparers of the financial statements – and hence their

auditors). Under IFRS, certain fair values are based on management intent and ‘reasonable supportable assumptions’.

■ The audit of management intent potentially increases the auditor’s reliance on management representations. The auditor

must obtain such representations from the highest level of management and exercise an appropriate degree of

professional scepticism, being particularly alert to the implications of any conflicting evidence.

■ A significant development in international financial reporting is that it is no longer sufficient to report transactions and

past and future events that may only be possible. IAS 1 ‘Presentation of Financial Statements’ (Revised) requires that

key assumptions (and other key sources of estimation uncertainty) be disclosed. This requirement gives rise to yet

another area on which auditors may qualify their audit opinion, on grounds of disagreement, where such disclosure is

incorrect or inadequate.

■ Perhaps one of the most significant impacts of fair value accounting on audit work is that it necessarily increases it.

Consider for example, that even where the fair value of an asset is as easily vouched as original cost, fair value is

determined at least annually whereas historic cost is unchanged (and not re-vouched to original purchase

documentation).

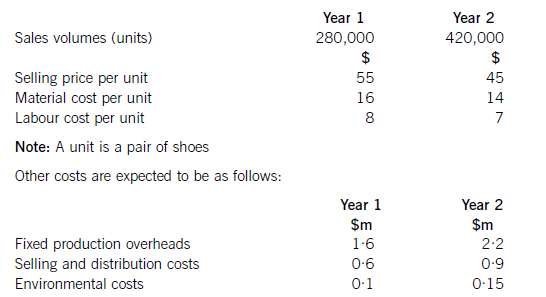

Shoe Co, a shoe manufacturer, has developed a new product called the ‘Smart Shoe’ for children, which has a built-in tracking device. The shoes are expected to have a life cycle of two years, at which point Shoe Co hopes to introduce a new type of Smart Shoe with even more advanced technology. Shoe Co plans to use life cycle costing to work out the total production cost of the Smart Shoe and the total estimated profit for the two-year period.

Shoe Co has spent $5·6m developing the Smart Shoe. The time spent on this development meant that the company missed out on the opportunity of earning an estimated $800,000 contribution from the sale of another product.

The company has applied for and been granted a ten-year patent for the technology, although it must be renewed each year at a cost of $200,000. The costs of the patent application were $500,000, which included $20,000 for the salary costs of Shoe Co’s lawyer, who is a permanent employee of the company and was responsible for preparing the application.

The following information is also available for the next two years:

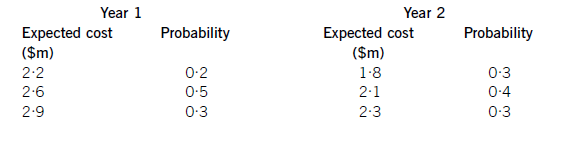

Shoe Co is still negotiating with marketing companies with regard to its advertising campaign, so is uncertain as to what the total marketing costs will be each year. However, the following information is available as regards the probabilities of the range of costs which are likely to be incurred:

Required:

Applying the principles of life cycle costing, calculate the total expected profit for Shoe Co for the two-year period.

(10 marks)

Totalsalesrevenue=(280,000x$55)+(420,000x$45)=$15·4m+18·9m=$34·3m.NoteTheexpectedprofithasbeencalculatedusinglifecyclecostingnotrelevantcosting.Hence,the$20,000salarycostincludedinpatentcostsshouldbeincludedinthelifecyclecost.Similarly,theopportunitycostof$800,000isnotincludedusinglifecyclecostingwhereasifrelevantcostingwasbeingusedtodecideonaparticularcourseofaction,theopportunitycostwouldbeincluded.Working1Expectedmarketingcostinyear1:(0·2x$2·2m)+(0·5x$2·6m)+(0·3x$2·9m)=$2·61mExpectedmarketingcostyear2:(0·3x$1·8m)+(0·4x$2·1m)+(0·3x$2·3m)=$2·07mTotalexpectedmarketingcost=$4·68m

2 The draft financial statements of Choctaw, a limited liability company, for the year ended 31 December 2004 showed

a profit of $86,400. The trial balance did not balance, and a suspense account with a credit balance of $3,310 was

included in the balance sheet.

In subsequent checking the following errors were found:

(a) Depreciation of motor vehicles at 25 per cent was calculated for the year ended 31 December 2004 on the

reducing balance basis, and should have been calculated on the straight-line basis at 25 per cent.

Relevant figures:

Cost of motor vehicles $120,000, net book value at 1 January 2004, $88,000

(b) Rent received from subletting part of the office accommodation $1,200 had been put into the petty cash box.

No receivable balance had been recognised when the rent fell due and no entries had been made in the petty

cash book or elsewhere for it. The petty cash float in the trial balance is the amount according to the records,

which is $1,200 less than the actual balance in the box.

(c) Bad debts totalling $8,400 are to be written off.

(d) The opening accrual on the motor repairs account of $3,400, representing repair bills due but not paid at

31 December 2003, had not been brought down at 1 January 2004.

(e) The cash discount totals for December 2004 had not been posted to the discount accounts in the nominal ledger.

The figures were:

$

Discount allowed 380

Discount received 290

After the necessary entries, the suspense account balanced.

Required:

Prepare journal entries, with narratives, to correct the errors found, and prepare a statement showing the

necessary adjustments to the profit.

(10 marks)

(b) Prepare a consolidated statement of financial position of the Ribby Group at 31 May 2008 in accordance

with International Financial Reporting Standards. (35 marks)

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2021-04-08

- 2020-01-08

- 2020-01-10

- 2020-01-09

- 2021-05-07

- 2020-02-22

- 2021-05-22

- 2020-01-09

- 2020-08-13

- 2021-01-13

- 2020-04-03

- 2020-02-23

- 2020-01-10

- 2020-03-22

- 2020-01-08

- 2020-02-26

- 2020-01-08

- 2021-01-13

- 2020-02-27

- 2020-04-19

- 2020-01-09

- 2020-03-21

- 2020-01-09

- 2020-01-08

- 2021-04-09

- 2020-04-18

- 2020-09-03

- 2021-02-25

- 2020-01-08

- 2020-05-20