澳门2020年ACCA国际会计师报名入口及报名流程~

发布时间:2020-01-09

各位“资深”ACCAer们,提醒一下大家,目前正处于2020年3月份ACCA考试的常规报名阶段,没有报名的同学请抓紧时间报名哦~ 什么?作为“资深”ACCAer的你竟然忘记了ACCA报名的流程是什么样的?那么接下来,51题库考试学习网将告诉大家关于ACCA考试报名流程的具体操作步骤,萌新建议收藏哦~

第一步:登录ACCA官方网站:https://www.accaglobal.com/africa/en.html,点击myACCA(在这里温馨提示大家,因为ACCA称之为国际注册会计师,因此报名的流程是全英文的)

第二步:输入你的ACCA账号和密码,点击SIGN in to Myacca

第三步:在左侧导航栏中找到“EXAM ENTRY”,点击进入

第四步:点击 Book your

exams now

第五步:点击 Add

an exam

第六步(这个步骤相对比较复杂,各位同学们注意哟!):分别选择地点、时间、报考科目

第七步:在下图红色画圈处点击方框处打钩,之后点击Proceed to Payment支付考试费用

最后一步:有VISA双币卡的同学可以用VISA卡支付,没有VISA卡的同学可以使用支付宝支付(Alipay)

“资深”ACCAer们看完上面的科目报名缴费流程,是不是回忆起来了呀?“新手”ACCAer们是否对报名缴费流程有了一定的了解呢?51题库考试学习网在这里想告诉大家:毕竟报考ACCA考试的费用不算一个小数目,请同学们报考时谨慎考虑,一旦报名的那一刻就一定要坚持下来,学习的路程注定是孤独的,要坚定自己的内心,持之以恒地学习下去,加油,同学们~

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

You are the audit supervisor of Maple & Co and are currently planning the audit of an existing client, Sycamore Science Co (Sycamore), whose year end was 30 April 2015. Sycamore is a pharmaceutical company, which manufactures and supplies a wide range of medical supplies. The draft financial statements show revenue of $35·6 million and profit before tax of $5·9 million.

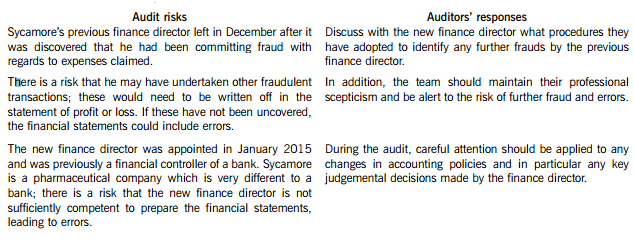

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

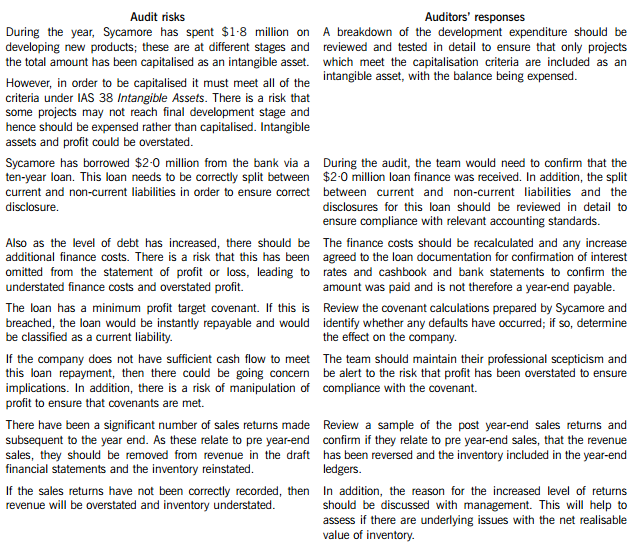

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

(a) Fraud responsibility

Maple & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error.

In order to fulfil this responsibility, Maple & Co is required to identify and assess the risks of material misstatement of the financial statements due to fraud.

They need to obtain sufficient appropriate audit evidence regarding the assessed risks of material misstatement due to fraud, through designing and implementing appropriate responses. In addition, Maple & Co must respond appropriately to fraud or suspected fraud identified during the audit.

When obtaining reasonable assurance, Maple & Co is responsible for maintaining professional scepticism throughout the audit, considering the potential for management override of controls and recognising the fact that audit procedures which are effective in detecting error may not be effective in detecting fraud.

To ensure that the whole engagement team is aware of the risks and responsibilities for fraud and error, ISAs require that a discussion is held within the team. For members not present at the meeting, Sycamore’s audit engagement partner should determine which matters are to be communicated to them.

(b) Audit risks and auditors’ responses

(c) (i) Review engagements

Review engagements are often undertaken as an alternative to an audit, and involve a practitioner reviewing financial data, such as six-monthly figures. This would involve the practitioner undertaking procedures to state whether anything has come to their attention which causes the practitioner to believe that the financial data is not in accordance with the financial reporting framework.

A review engagement differs to an external audit in that the procedures undertaken are not nearly as comprehensive as those in an audit, with procedures such as analytical review and enquiry used extensively. In addition, the practitioner does not need to comply with ISAs as these only relate to external audits.

(ii) Levels of assurance

The level of assurance provided by audit and review engagements is as follows:

External audit – A high but not absolute level of assurance is provided, this is known as reasonable assurance. This provides comfort that the financial statements present fairly in all material respects (or are true and fair) and are free of material misstatements.

Review engagements – where an opinion is being provided, the practitioner gathers sufficient evidence to be satisfied that the subject matter is plausible; in this case negative assurance is given whereby the practitioner confirms that nothing has come to their attention which indicates that the subject matter contains material misstatements.

(c) Briefly outline the corporation tax (CT) issues that Tay Limited should consider when deciding whether to

acquire the shares or the assets of Tagus LDA. You are not required to discuss issues relating to transfer

pricing. (7 marks)

(c) (1) Acquisition of shares

Status

The acquisition of shares in Tagus LDA will add another associated company to the group. This may have an adverse

effect on the rates of corporation tax paid by the two existing group companies, particularly Tay Limited.

Taxation of profits

Profits will be taxed in Portugal. Any profits remitted to the UK as dividends will be taxable as Schedule D Case V income,

but will attract double tax relief. Double tax relief will be available against two types of tax suffered in Portugal. Credit

will be given for any tax withheld on payments from Tagus LDA to Tay Limited and relief will also be available for the

underlying tax as Tay Limited owns at least 10% of the voting power of Tagus LDA. The underlying tax is the tax

attributable to the relevant profits from which the dividend was paid. Double tax relief is given at the lower rate of the

UK tax and the foreign tax (withholding and underlying taxes) suffered.

Losses

As Tagus LDA is a non-UK resident company, losses arising in Tagus LDA cannot be group relieved against profits of the

two UK companies. Similarly, any UK trading losses cannot be used against profits generated by Tagus LDA.

(2) Acquisition of assets

Status

The business of Tagus will be treated as a branch of Tay Limited i.e. an extension of the UK company’s activities. The

number of associated companies will be unaffected.

Taxation of profits

Tay Limited will be treated as having a permanent establishment in Portugal. Profits attributable to the Tagus business

will thus still be taxed in Portugal. In addition, the profits will be taxed in the UK as trading income. Double tax relief

will be available for the tax already suffered in Portugal at the lower of the two rates.

Capital allowances will be available. As the assets in question will not previously have been subject to a claim for UK

capital allowances, there will be no cost restriction and the consideration attributable to each asset will form. the basis

for the capital allowance claim.

Losses

The Tagus trade is part of Tay Limited’s trade, so any losses incurred by the Portuguese trade will automatically be offset

against the trading profits of the UK trade, and vice versa.

(d) Family owned and managed businesses often find delegation and succession difficult processes to get right.

What models would you recommend that Tony use in looking to change his leadership and management style

to create a culture in the Shirtmaster Group better able to deal with the challenges it faces? (10 marks)

(d) Much has been written on the links between leadership and culture and in particular the influence of the founder on the

culture of the organisation. Schein actually argues that leadership and culture are two sides of the same coin. Tony’s father

had a particular vision of the type of company he wanted and importance of product innovation to the success of the business.

Tony is clearly influenced by that cultural legacy and has maintained a dominant role in the business though there is little

evidence of continuing innovation. Using the McKinsey 7-S model the founder or leader is the main influence on the

development of the shared values in the firm that shapes the culture. However, it is clear from the scenario that Tony through

his ‘hands-on’ style. of leadership is affecting the other elements in the model – strategy, structure and systems – the ‘hard’

factors and the senior staff and their skills – the ‘soft’ factors – in making strategic decisions.

Delegation has been highlighted as one of the problems Tony has to face and it is a familiar one in family firms. Certainly

there could be need for him to give his senior management team the responsibility for the functional areas they nominally

control. Tony’s style. is very much a ‘hands-on’ style. but this may be inappropriate for handling the problems that the company

faces. Equally, he seems too responsible for the strategic decisions the company is taking and not effectively involving his

team in the strategy process. Style. is seen as a key factor in influencing the culture of an organisation and getting the right

balance between being seen as a paternalistic owner-manager and a chairman and chief executive looking to develop his

senior management team is difficult. Leadership is increasingly being seen as encouraging and enabling others to handle

change and challenge and questioning the assumptions that have influenced Shirtmaster’s strategic thinking and development

to date. The positive side of Tony’s style. of leadership is that he is both known and well regarded by the staff on the factory

floor. Unfortunately, if the decision is taken to source shirts from abroad this may mean that the manufacturing capability

disappears.

6D–ENGAA

Paper 3.5

Tony should be aware that changing the culture of an organisation is not an easy task and that as well as his leadership style

influencing, his leadership can also be constrained by the existing culture that exists in the Shirtmaster Group. Other models

that could be useful include Johnson, Scholes and Whittington’s cultural web and Lewin’s three-stage model of change and

forcefield analysis. Finally, Peters and Waterman in their classic study ‘In search of excellence’ provides insights into the closerelationship between leadership and creating a winning culture.

5 Crusoe has contacted you following the death of his father, Noland. Crusoe has inherited the whole of his father’s

estate and is seeking advice on his father’s capital gains tax position and the payment of inheritance tax following his

death.

The following information has been extracted from client files and from telephone conversations with Crusoe.

Noland – personal information:

– Divorcee whose only other relatives are his sister, Avril, and two grandchildren.

– Died suddenly on 1 October 2007 without having made a will.

– Under the laws of intestacy, the whole of his estate passes to Crusoe.

Noland – income tax and capital gains tax:

– Has been a basic rate taxpayer since the tax year 2000/01.

– Sales of quoted shares resulted in:

– Chargeable gains of £7,100 and allowable losses of £17,800 in the tax year 2007/08.

– Chargeable gains of approximately £14,000 each tax year from 2000/01 to 2006/07.

– None of the shares were held for long enough to qualify for taper relief.

Noland – gifts made during lifetime:

– On 1 December 1999 Noland gave his house to Crusoe.

– Crusoe has allowed Noland to continue living in the house and has charged him rent of £120 per month

since 1 December 1999. The market rent for the house would be £740 per month.

– The house was worth £240,000 at the time of the gift and £310,000 on 1 October 2007.

– On 1 November 2004 Noland transferred quoted shares worth £232,000 to a discretionary trust for the benefit

of his grandchildren.

Noland – probate values of assets held at death: £

– Portfolio of quoted shares 370,000

Shares in Kurb Ltd 38,400

Chattels and cash 22,300

Domestic liabilities including income tax payable (1,900)

– It should be assumed that these values will not change for the foreseeable future.

Kurb Ltd:

– Unquoted trading company

– Noland purchased the shares on 1 December 2005.

Crusoe:

– Long-standing personal tax client of your firm.

– Married with two young children.

– Successful investment banker with very high net worth.

– Intends to gift the portfolio of quoted shares inherited from Noland to his aunt, Avril, who has very little personal

wealth.

Required:

(a) Prepare explanatory notes together with relevant supporting calculations in order to quantify the tax relief

potentially available in respect of Noland’s capital losses realised in 2007/08. (4 marks)

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-10

- 2020-03-08

- 2020-03-08

- 2020-03-12

- 2020-04-10

- 2020-01-10

- 2019-07-21

- 2020-03-13

- 2020-03-07

- 2020-03-11

- 2020-03-03

- 2019-12-31

- 2020-01-10

- 2020-01-29

- 2020-03-04

- 2020-04-15

- 2020-04-28

- 2021-05-14

- 2020-04-18

- 2020-01-10

- 2020-02-28

- 2020-01-08

- 2019-12-29

- 2020-05-21

- 2020-01-03

- 2020-03-03

- 2020-03-22

- 2020-01-09

- 2020-04-17

- 2020-01-09