你知道工商管理专业可以考acca吗?免考哪几科?

发布时间:2020-04-11

你知道工商管理专业可以考acca吗?免考哪几科?不清楚的小伙伴看过来,一起跟51题库考试学习网了解一下吧!

一、工商管理专业可以考acca事项

无论专业如何都是可以报考ACCA,只要是教育部承认的大专以上学历,即可报名成为ACCA的正式学员;

政策上看报名注册ACCA学员,只需要具备以下条件之一即可:

教育部认可的高等院校在校生(本科在校),顺利完成大一的课程考试,即可报名成为ACCA的正式学员;

2、凡具有教育部承认的大专以上学历,即可报名成为ACCA的正式学员;

3、未符合1、2项报名资格的申请者,也可以先申请参加FIA(Foundations in Accountancy)基础财务资格考试。在完成FAB(基础商业会计)、FMA(基础管理会计)、FFA(基础财务会计)3门课程后,可豁免ACCA

AB-FA三门课程的考试,直接进入ACCA技能课程的考试。

二、ACCA免考专业

会计学专业 - 获得学士学位或硕士学位(金融、财务管理、审计专业也享受等同于会计学专业的免试政策)。

三、ACCA免考政策相关注意事项:

1)获得大学学历的非在校人员,只要年满21周岁即可通过成人途径(MSER)注册成为ACCA学员,但不能申请任何科目的免考。

2)申请牛津布鲁克斯大学的学士学位,需要出具相关英文水平证明,如CET-6, TOEFL 500分, IELTS

6.5分;如果没有英语证明,则不能申请F3的免试。

3)学员只有顺利通过整学年的课程才能够申请免试。

4)针对在校生的部分课程免试政策只适用于大学本科的在读学生,而不适用于硕士学位或大专学历的在读学生。

5)获得硕士学位和大专文凭的学生的免试课程只能按所学课程的相关性由ACCA免试评估部门进行逐门评估而定。

6)在中国,会计学学士学位是指会计学士、会计学学士、会计与金融学士或经济学学士(专业方向为会计学,会计与金融,国际会计,注册会计师)。

7)取得与会计学相关领域专业的学位都按“其他专业”对待,例如财务会计、工业会计、外贸会计、会计电算化、铁路会计等。

8)在大学第一学年所学过的课程不能作为申请免试的依据。

9)特许学位(即海外大学与中国本地大学合作而授予海外大学学位的项目),部分完成时不能申请免试。

10)本政策适用于在中国教育部认可的高等院校全部完成或部分完成本科课程的学生,而不考虑目前居住地点。

11)欲申请牛津·布鲁克斯大学学士学位的学员在取得本科学位之前,不能申请F4和F5课程的免试。

12)学员以国外大学学位申请免考,请直接到ACCA官方网站查询可免课程,一般不需要再提供国内的学历证明。

以上就是51题库考试学习网今天分享的全部内容啦,大家看完之后,希望可以帮助到你哦!想了解更多相关信息,请关注51题库考试学习网。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(c) Assess Mr Hogg’s belief that employing child labour is ‘always ethically wrong’ from deontological and

teleological (consequentialist) ethical perspectives. (9 marks)

(c) Mr Hogg’s belief that employing child labour is ‘always ethically wrong’

Deontological perspective:

In the case scenario, Mr Hogg is demonstrating a deontological position on child labour by saying that it is ‘always’ wrong.

He is adopting an absolutist rather than a relativist or situational stance in arguing that there are no situations in which child

labour might be ethically acceptable. The deontological view is that an act is right or wrong in itself and does not depend

upon any other considerations (such as economic necessity or the extent of the child’s willingness to work). If child labour is

wrong in one situation, it follows that it is wrong in all situations because of the Kantian principle of generalisability (in the

categorical imperative). Because child labour is wrong and potentially exploitative in some situations, the deontological

position says that it must be assumed to be wrong in all situations. The fact that it may cause favourable outcomes in some

situations does not make it ethically right, because the deontological position is not situational and the quality of the outcome

is not taken into account.

Teleological perspective:

According to the teleological perspective, an act is right or wrong depending on the favourableness of the outcome. It is

sometimes called the consequentialist perspective because the consequences of the action are considered more important

than the act itself.

In the teleological perspective, ethics is situational and not absolute. Therefore child labour is morally justified if the outcome

is favourable. The economic support of a child’s family by provision of wages for family support might be considered to be a

favourable outcome that justifies child labour. There is an ethical trade-off between the importance of the family income from

child labour and the need to avoid exploitation and interfere with the child’s education. Education is clearly important but

family financial support might be a more favourable outcome, at least in the short term, and if so, this would justify the child

working rather than being in school. For HPC, child labour is likely to be cheaper than adult labour but will alienate European

buyers and be in breach of its code of ethics. Child labour may be ethically acceptable if the negative consequences can be

addressed and overcome.

[Tutorial note: other, equally relevant points made in evaluating Mr Hogg’s opinion will be valid. The texts discuss teleology

in terms of utilitarianism and egoism. Although this distinction is not relevant to the question, candidates should not be

penalised for introducing the distinction if the other points raised are relevant]

(ii) the recent financial performance of Merton plc from a shareholder perspective. Clearly identify any

issues that you consider should be brought to the attention of the ordinary shareholders. (15 marks)

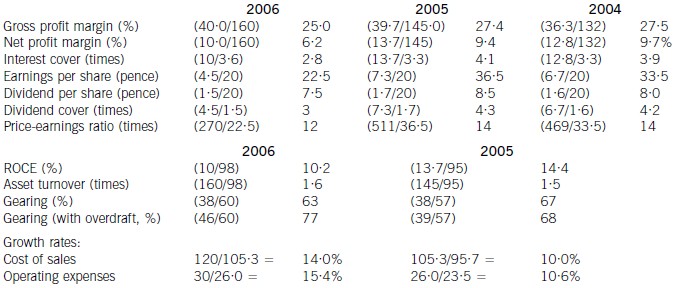

(ii) Discussion of financial performance

It is clear that 2006 has been a difficult year for Merton plc. There are very few areas of interest to shareholders where

anything positive can be found to say.

Profitability

Return on capital employed has declined from 14·4% in 2005, which compared favourably with the sector average of

12%, to 10·2% in 2006. Since asset turnover has improved from 1·5 to 1·6 in the same period, the cause of the decline

is falling profitability. Gross profit margin has fallen each year from 27·5% in 2004 to 25% in 2006, equal to the sector

average, despite an overall increase in turnover during the period of 10% per year. Merton plc has been unable to keep

cost of sales increases (14% in 2006 and 10% in 2005) below the increases in turnover. Net profit margin has declined

over the same period from 9·7% to 6·2%, compared to the sector average of 8%, because of substantial increases in

operating expenses (15·4% in 2006 and 10·6% in 2005). There is a pressing need here for Merton plc to bring cost

of sales and operating costs under control in order to improve profitability.

Gearing and financial risk

Gearing as measured by debt/equity has fallen from 67% (2005) to 63% (2006) because of an increase in

shareholders’ funds through retained profits. Over the same period the overdraft has increased from £1m to £8m and

cash balances have fallen from £16m to £1m. This is a net movement of £22m. If the overdraft is included, gearing

has increased to 77% rather than falling to 63%.

None of these gearing levels compare favourably with the average gearing for the sector of 50%. If we consider the large

increase in the overdraft, financial risk has clearly increased during the period. This is also evidenced by the decline in

interest cover from 4·1 (2005) to 2·8 (2006) as operating profit has fallen and interest paid has increased. In each year

interest cover has been below the sector average of eight and the current level of 2·8 is dangerously low.

Share price

As the return required by equity investors increases with increasing financial risk, continued increases in the overdraft

will exert downward pressure on the company’s share price and further reductions may be expected.

Investor ratios

Earnings per share, dividend per share and dividend cover have all declined from 2005 to 2006. The cut in the dividend

per share from 8·5 pence per share to 7·5 pence per share is especially worrying. Although in its announcement the

company claimed that dividend growth and share price growth was expected, it could have chosen to maintain the

dividend, if it felt that the current poor performance was only temporary. By cutting the dividend it could be signalling

that it expects the poor performance to continue. Shareholders have no guarantee as to the level of future dividends.

This view could be shared by the market, which might explain why the price-earnings ratio has fallen from 14 times to

12 times.

Financing strategy

Merton plc has experienced an increase in fixed assets over the last period of £10m and an increase in stocks and

debtors of £21m. These increases have been financed by a decline in cash (£15m), an increase in the overdraft (£7m)

and an increase in trade credit (£6m). The company is following an aggressive strategy of financing long-term

investment from short-term sources. This is very risky, since if the overdraft needed to be repaid, the company would

have great difficulty in raising the funds required.

A further financing issue relates to redemption of the existing debentures. The 10% debentures are due to be redeemed

in two years’ time and Merton plc will need to find £13m in order to do this. It does not appear that this sum can be

raised internally. While it is possible that refinancing with debt paying a lower rate of interest may be possible, the low

level of interest cover may cause concern to potential providers of debt finance, resulting in a higher rate of interest. The

Finance Director of Merton plc needs to consider the redemption problem now, as thought is currently being given to

raising a substantial amount of new equity finance. This financing choice may not be available again in the near future,

forcing the company to look to debt finance as a way of effecting redemption.

Overtrading

The evidence produced by the financial analysis above is that Merton plc is showing some symptoms of overtrading

(undercapitalisation). The board are suggesting a rights issue as a way of financing an expansion of business, but it is

possible that a rights issue will be needed to deal with the overtrading problem. This is a further financing issue requiring

consideration in addition to the redemption of debentures mentioned earlier.

Conclusion

Ordinary shareholders need to be aware of the following issues.

1. Profitability has fallen over the last year due to poor cost control

2. A substantial increase in the overdraft over the last year has caused gearing to increase

3. It is possible that the share price will continue to fall

4. The dividend cut may warn of continuing poor performance in the future

5. A total of £13m of debentures need redeeming in two year’s time

6. A large amount of new finance is needed for working capital and debenture redemption

Appendix: Analysis of key ratios and financial information

(b) During the inventory count on 31 December, some goods which had cost $80,000 were found to be damaged.

In February 2005 the damaged goods were sold for $85,000 by an agent who received a 10% commission out

of the sale proceeds. (2 marks)

Required:

Advise the directors on the correct treatment of these matters, stating the relevant accounting standard which

justifies your answer in each case.

NOTE: The mark allocation is shown against each of the three matters.

(b) The inventories should be valued at the lower of cost and net realisable value. Cost is $80,000, net realisable value is

$85,000 less 10%, or $76,500. The net realisable value of $76,500 should therefore be taken (IAS2 Inventories)

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2019-07-19

- 2020-02-06

- 2020-01-09

- 2020-02-18

- 2020-01-09

- 2020-05-10

- 2020-05-03

- 2020-01-09

- 2020-01-09

- 2019-07-19

- 2020-02-04

- 2020-05-14

- 2020-01-09

- 2020-03-22

- 2020-01-09

- 2020-05-11

- 2020-01-30

- 2020-03-25

- 2020-05-05

- 2020-01-14

- 2020-02-11

- 2020-01-09

- 2020-02-19

- 2020-01-09

- 2020-01-09

- 2020-05-20

- 2019-12-30

- 2020-05-07

- 2021-04-23

- 2020-01-09