ACCA考试的注册费用是多少?每年都要交吗?

发布时间:2020-09-03

各位小伙伴注意了!很多同学提出疑问:ACCA考试的注册费用是多少?为了帮助大家了解更多,51题库考试学习网为大家带来了相关内容,让我们一起来看看吧!

ACCA注册费用:

ACCA注册费用是指在学员首次注册的时候一次性收取的费用,费用标准为79英镑。由此可知,这项费用并不用每年都需要缴纳。之后每年需要缴纳的费用为年费,学员年费为112英镑,准会员为123英镑,而会员首次为246英镑,之后则需要缴纳258英镑。

这两个费用是相对固定的费用,每个学员都是一样的。而考试费用则有较大浮动,不同的报考时间和不同的免考科目都会带来比较大的费用区别,一个基本原则是建议想要报名的学生尽早报名,这样才能最大程度地节约考试成本。

另外无论在几月份注册ACCA,都将从注册后第二个自然年度的一月份开始缴纳年费,以保持学员身份、继续考试。没有在规定时间内及时付清所欠的任何费用(年费、免试费等)都将被除名。如果被除名后,还想继续报考ACCA,就需要重新缴纳注册费用。

在不同国家考考ACCA,不同地区的成绩都会承认吗?

学员的考试成绩在注册后的有效期内都有效。每个学员注册后拥有一个注册号,可以凭此在全球230多个考点中更换、选择适合自己的考点。学员不论在何地参加考试,其成绩都会记录在ACCA学员系统中。

ACCA课程包括哪些内容:

ACCA考试是按现代企业财务人员需要具备的技能和技术的要求而设计的,共有13门课程,两门选修课,课程分为3个部分:

第一部分涉及基本会计原理;

第二部分涵盖专业财会人员应具备的核心专业技能;

第三部分培养学员以专业知识对信息进行评估,并提出合理的经营建议和忠告。

ACCA学员在通过ACCA专业资格考试第一、二部分即前9门的考试之后,再提交一份研究和分析报告,就有机会获得牛津·布鲁克斯大学的应用会计(优等)理学士学位。根据中英双方2003年2月签订的《中华人民共和国政府和大不列颠及北爱尔兰联合王国政府及托管政府关于相互承认高等教育学位证书的协议》协议,获得牛津·布鲁克斯大学(优等)理学士学位且成绩优异者,在不用取得中国硕士学位的前提下,可以直接参加中国博士生入学考试。

以上就是今天分享的全部内容了,各位小伙伴根据自己的情况进行查阅,希望本文对各位有所帮助,预祝各位取得满意的成绩,如需了解更多相关内容,请关注51题库考试学习网!

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) Discuss the view that fair value is a more relevant measure to use in corporate reporting than historical cost.

(12 marks)

(b) The main disagreement over a shift to fair value measurement is the debate over relevance versus reliability. It is argued that

historical cost financial statements are not relevant because they do not provide information about current exchange values

for the entity’s assets which to some extent determine the value of the shares of the entity. However, the information provided

by fair values may be unreliable because it may not be based on arm’s-length transactions. Proponents of fair value

accounting argue that this measurement is more relevant to decision makers even if it is less reliable and would produce

balance sheets that are more representative of a company’s value. However it can be argued that relevant information that is

unreliable is of no use to an investor. One advantage of historical cost financial information is that it produces earnings

numbers that are not based on appraisals or other valuation techniques. Therefore, the income statement is less likely to be

subject to manipulation by management. In addition, historical cost balance sheet figures comprise actual purchase prices,

not estimates of current values that can be altered to improve various financial ratios. Because historical cost statements rely

less on estimates and more on ‘hard’ numbers, it can be said that historical cost financial statements are more reliable than

fair value financial statements. Furthermore, fair value measurements may be less reliable than historical costs measures

because fair value accounting provides management with the opportunity to manipulate the reported profit for the period.

Developing reliable methods of measuring fair value so that investors trust the information reported in financial statements is

critical.

Fair value measurement could be said to be more relevant than historical cost as it is based on market values and not entity

specific measurement on initial recognition, so long as fair values can be reliably measured. Generally the fair value of the

consideration given or received (effectively historical cost) also represents the fair value of the item at the date of initial

recognition. However there are many cases where significant differences between historical cost and fair value can arise on

initial recognition.

Historical cost does not purport to measure the value received. It cannot be assumed that the price paid can be recovered in

the market place. Hence the need for some additional measure of recoverable value and impairment testing of assets.

Historical cost can be an entity specific measurement. The recorded historical cost can be lower or higher than its fair value.

For example the valuation of inventory is determined by the costing method adopted by the entity and this can vary from

entity to entity. Historical cost often requires the allocation of costs to an asset or liability. These costs are attributed to assets,

liabilities and expenses, and are often allocated arbitrarily. An example of this is self constructed assets. Rules set out in

accounting standards help produce some consistency of historical cost measurements but such rules cannot improve

representational faithfulness.

Another problem with historical cost arises as regards costs incurred prior to an asset being recognised. Historical costs

recorded from development expenditure cannot be capitalised if they are incurred prior to the asset meeting the recognition

criteria in IAS38 ‘Intangible Assets’. Thus the historical cost amount does not represent the fair value of the consideration

given to create the asset.

The relevance of historical cost has traditionally been based on a cost/revenue matching principle. The objective has been to

expense the cost of the asset when the revenue to which the asset has contributed is recognised. If the historical cost of the

asset differs from its fair value on initial recognition then the matching process in future periods becomes arbitrary. The

measurement of assets at fair value will enhance the matching objective. Historical cost may have use in predicting future

net reported income but does not have any necessary implications for future cash flows. Fair value does embody the market’s

expectations for those future cash flows.

However, historical cost is grounded in actual transaction amounts and has existed for many years to the extent that it is

supported by practical experience and familiarity. Historical cost is accepted as a reliable measure especially where no other

relevant measurement basis can be applied.

(d) Player trading

Another proposal is for the club to sell its two valuable players, Aldo and Steel. It is thought that it will receive a

total of $16 million for both players. The players are to be offered for sale at the end of the current football season

on 1 May 2007. (5 marks)

Required:

Discuss how the above proposals would be dealt with in the financial statements of Seejoy for the year ending

31 December 2007, setting out their accounting treatment and appropriateness in helping the football club’s

cash flow problems.

(Candidates do not need knowledge of the football finance sector to answer this question.)

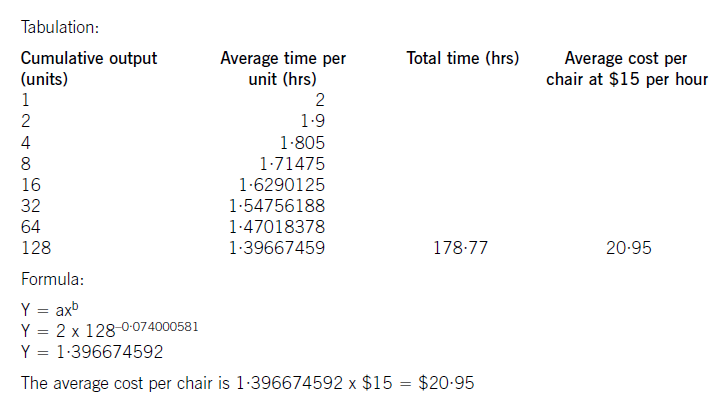

Big Cheese Chairs (BCC) manufactures and sells executive leather chairs. They are considering a new design of massaging chair to launch into the competitive market in which they operate.

They have carried out an investigation in the market and using a target costing system have targeted a competitive selling price of $120 for the chair. BCC wants a margin on selling price of 20% (ignoring any overheads).

The frame. and massage mechanism will be bought in for $51 per chair and BCC will upholster it in leather and assemble it ready for despatch.

Leather costs $10 per metre and two metres are needed for a complete chair although 20% of all leather is wasted in the upholstery process.

The upholstery and assembly process will be subject to a learning effect as the workers get used to the new design.

BCC estimates that the first chair will take two hours to prepare but this will be subject to a learning rate (LR) of 95%.

The learning improvement will stop once 128 chairs have been made and the time for the 128th chair will be the time for all subsequent chairs. The cost of labour is $15 per hour.

The learning formula is shown on the formula sheet and at the 95% learning rate the value of b is -0·074000581.

Required:

(a) Calculate the average cost for the first 128 chairs made and identify any cost gap that may be present at

that stage. (8 marks)

(b) Assuming that a cost gap for the chair exists suggest four ways in which it could be closed. (6 marks)

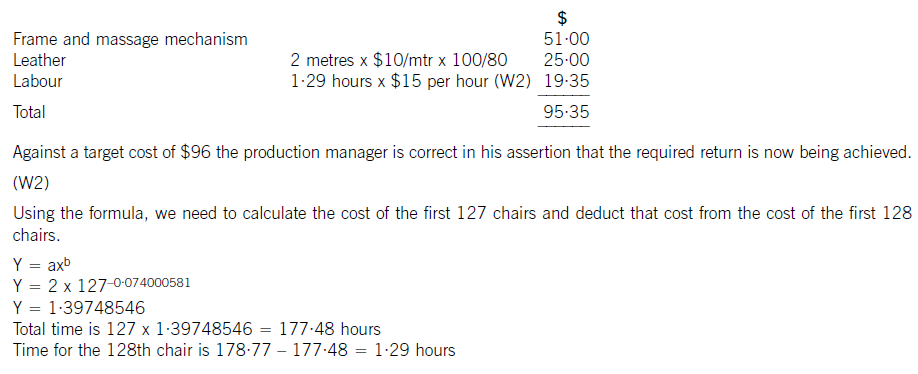

The production manager denies any claims that a cost gap exists and has stated that the cost of the 128th chair will be low enough to yield the required margin.

(c) Calculate the cost of the 128th chair made and state whether the target cost is being achieved on the 128th chair. (6 marks)

(W1)

The cost of the labour can be calculated using learning curve principles. The formula can be used or a tabular approach would

also give the average cost of 128 chairs. Both methods are acceptable and shown here.

(b) To reduce the cost gap various methods are possible (only four are needed for full marks)

– Re-design the chair to remove unnecessary features and hence cost

– Negotiate with the frame. supplier for a better cost. This may be easier as the volume of sales improve as suppliers often

are willing to give discounts for bulk buying. Alternatively a different frame. supplier could be found that offers a better

price. Care would be needed here to maintain the required quality

– Leather can be bought from different suppliers or at a better price also. Reducing the level of waste would save on cost.

Even a small reduction in waste rates would remove much of the cost gap that exists

– Improve the rate of learning by better training and supervision

– Employ cheaper labour by reducing the skill level expected. Care would also be needed here not to sacrifice quality or

push up waste rates.

(c) The cost of the 128th chair will be:

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2019-12-06

- 2020-01-09

- 2020-04-18

- 2020-01-10

- 2020-01-03

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-09

- 2021-02-14

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2019-12-29

- 2020-04-30

- 2020-01-09

- 2020-01-10

- 2020-02-05

- 2020-01-29

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-09

- 2020-02-01

- 2020-01-10

- 2020-04-07

- 2020-04-23

- 2020-05-09

- 2020-04-30

- 2021-04-24