2020年ACCA考试安排将会发生变化,这是真的吗?

发布时间:2020-03-11

ACCA考试分为四个考试季,每个考试季举行一次考试。其中,第一考试的考试时间就在三月份。受新冠疫情影响,部分报考了2020年第一考试季ACCA考试的小伙伴不免担心,这次考试是否能正常举行。鉴于此,51题库考试学习网在下面为大家带来2020年ACCA考试时间的相关信息,以供参考。

根据ACCA官网消息,2020年3月份的ACCA考试已经正式取消,学员缴纳的考试费用也将全部退还到ACCA账户当中,考生需要重新报名ACCA考试。

ACCA考试每年举行四次,分别在每年的3月、6月、9月、12月。不同年份的具体考试时间略有差异,请考生注意ACCA官网发布的消息。不过根据之前ACCA官方给出的消息,2020年3月份的ACCA考试将取消,因此考生只能报考6月份的ACCA考试。每次考试报名时间都分为三个阶段:提前报名、常规报名、后期报名。不同年份的具体时间略有不同,一般来说3月份考试的报名截止时间分别为上一年的11月、1月、2月;6月份考试的报名截止时间分别为当年的2月、4月以及5月;9月份考试的报名截止时间分别为当年的5月、7月、8月;12月份报名截止时间分别在当年的8月、10月、11月。小伙伴们在报名时,一定要注意官方公布的报名信息中显示的是报名截止日期哦。

以上就是关于ACCA考试时间的相关情况。51题库考试学习网提醒:报名3月份ACCA考试的小伙伴需要重新报名,然后才能参加考试。最后,51题库考试学习网预祝准备参加2020年ACCA考试的小伙伴都能顺利通过。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) Peter, one of Linden Limited’s non-executive directors, having lived and worked in the UK for most of his adult

life, sold his home near London on 22 March 2006 and, together with his wife (a French citizen), moved to live

in a villa which she owns in the south of France. Peter is now demanding that the tax deducted from his director’s

fees, for the board meetings held on 18 April and 16 May 2006, be refunded, on the grounds that, as he is no

longer resident in the UK, he is no longer liable to UK income tax. All of the company’s board meetings are held

at its offices in Cambridge.

Despite Peter’s assurance that none of the other companies of which he is a director has disputed his change of

tax status, Damian is uncertain whether he should make the refunds requested. However, as Peter is a friend of

the company’s founder, Linden Limited’s managing director is urging him to do so, stating that if the tax does

have to be paid, then Linden Limited could always bear the cost.

Required:

Advise Damian whether Peter is correct in his assertion regarding his tax position and in the case that there

is a UK tax liability the implications of the managing director’s suggestion. You are not required to consider

national insurance (NIC) issues. (4 marks)

(b) Peter will have been resident and ordinarily resident in the UK. When such individuals leave the UK for a purpose other than

to take up full time employment abroad, they normally continue to still be so regarded unless their absence spans a complete

tax year. But, where someone intends to live permanently abroad or to do so for a period of at least three tax years, they may

be treated as non-resident and non-ordinarily resident from the day after the date of their departure, if they can provide

evidence to HMRC of that intention. Selling a residence in the UK and setting up home abroad will normally constitute such

evidence. However to retain non-resident status the intention must actually be fulfilled, and visits to the UK must not exceed

182 days in any tax year or average more than 90 days per year over a period of four tax years. Given that Peter would appear

to have several company directorships in the UK, it is possible that he might fail to satisfy the 90 day average ‘substantial

visits’ rule.

Even if Peter is classed as non-resident, any remuneration earned in the UK will still be liable to UK income tax, and subject

to PAYE, unless it is for duties incidental to an overseas employment, which is unlikely to be the case for fees paid to a nonexecutive

director for attending board meetings. Thus, income tax should still be deducted from the fees under PAYE. Where

PAYE should have been deducted from a director’s emoluments and it has not been, but the tax is nevertheless accounted

for by the company to HMRC, then to the extent that the tax is not reimbursed by the director, he will be treated as receiving

a benefit equivalent to the amount of tax.

(b) Advise Sergio on the appropriateness of investing in a domestic rental property in view of his personal

circumstances and recommend suitable alternative investments giving reasons for your advice. (4 marks)

(b) Sergio’s investments

Sergio aims to leave a substantial asset to his family on his death. Accordingly, in view of his age, he is right to be considering

investing in an asset whose value is unlikely to fall suddenly, such as a domestic rental property. However, it must be

recognised that although the value of land and buildings can usually be relied on to increase over a long period of time, its

value may fall over a shorter period. The only investments that cannot fall in value are cash deposits, although they do, of

course, fall in real terms due to the effects of inflation.

Sergio should consider whether or not he wishes to increase his annual income. The return on capital invested in a domestic

rental property is unlikely to be very high due to the recent increases in property values in the UK. Also, there are likely to be

periods when the house is unoccupied during which no income will be generated. If it is important to Sergio to generate

additional income he should consider other low-risk investments with a more reliable and higher rate of return, for example,

gilt edged stocks, unit trusts and cash deposits.

Sergio must also decide whether it is important to him to be able to access capital quickly, as it is usually not possible to

realise the capital invested in land and buildings at short notice. If this is important, Sergio should consider holding some of

his capital in cash deposits or other liquid investments, eg unit trusts.

Sergio could invest up to £7,000 each year in an individual savings account (ISA). A maximum of £3,000 can be held as a

cash deposit with the balance invested in quoted shares. The income and gains arising on the funds invested would be

exempt from both income tax and capital gains tax. This would be a relatively low-risk investment and would also be

accessible quickly if required.

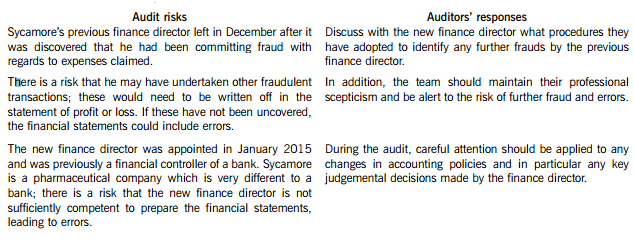

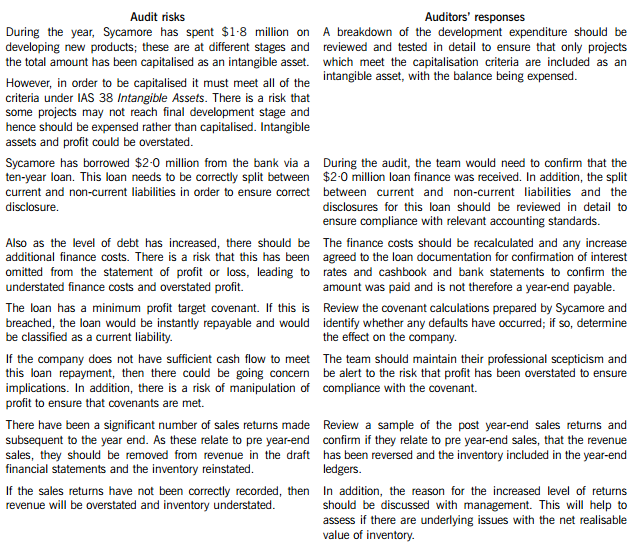

You are the audit supervisor of Maple & Co and are currently planning the audit of an existing client, Sycamore Science Co (Sycamore), whose year end was 30 April 2015. Sycamore is a pharmaceutical company, which manufactures and supplies a wide range of medical supplies. The draft financial statements show revenue of $35·6 million and profit before tax of $5·9 million.

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

(a) Fraud responsibility

Maple & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error.

In order to fulfil this responsibility, Maple & Co is required to identify and assess the risks of material misstatement of the financial statements due to fraud.

They need to obtain sufficient appropriate audit evidence regarding the assessed risks of material misstatement due to fraud, through designing and implementing appropriate responses. In addition, Maple & Co must respond appropriately to fraud or suspected fraud identified during the audit.

When obtaining reasonable assurance, Maple & Co is responsible for maintaining professional scepticism throughout the audit, considering the potential for management override of controls and recognising the fact that audit procedures which are effective in detecting error may not be effective in detecting fraud.

To ensure that the whole engagement team is aware of the risks and responsibilities for fraud and error, ISAs require that a discussion is held within the team. For members not present at the meeting, Sycamore’s audit engagement partner should determine which matters are to be communicated to them.

(b) Audit risks and auditors’ responses

(c) (i) Review engagements

Review engagements are often undertaken as an alternative to an audit, and involve a practitioner reviewing financial data, such as six-monthly figures. This would involve the practitioner undertaking procedures to state whether anything has come to their attention which causes the practitioner to believe that the financial data is not in accordance with the financial reporting framework.

A review engagement differs to an external audit in that the procedures undertaken are not nearly as comprehensive as those in an audit, with procedures such as analytical review and enquiry used extensively. In addition, the practitioner does not need to comply with ISAs as these only relate to external audits.

(ii) Levels of assurance

The level of assurance provided by audit and review engagements is as follows:

External audit – A high but not absolute level of assurance is provided, this is known as reasonable assurance. This provides comfort that the financial statements present fairly in all material respects (or are true and fair) and are free of material misstatements.

Review engagements – where an opinion is being provided, the practitioner gathers sufficient evidence to be satisfied that the subject matter is plausible; in this case negative assurance is given whereby the practitioner confirms that nothing has come to their attention which indicates that the subject matter contains material misstatements.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-03-08

- 2020-01-09

- 2020-01-09

- 2020-02-20

- 2020-01-09

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-03-11

- 2020-04-25

- 2020-02-21

- 2020-04-05

- 2020-03-08

- 2020-01-09

- 2020-03-01

- 2020-02-20

- 2020-01-09

- 2019-12-27

- 2020-05-13

- 2020-01-10

- 2019-08-03

- 2020-01-10

- 2020-04-24

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-04-08

- 2020-05-13

- 2020-04-23

- 2020-04-18