什么?你觉得ACCA证书在中国没有用?

发布时间:2020-02-06

相信大家都或多或少的听说过ACCA。那么什么是ACCA呢?由51题库考试学习网为您进行解答。ACCA是目前财经领域认可度最高的资格证书,也是世界上拥有学员和会员最多的,为此还被我国称之为“国际注册会计师”。那到底ACCA证书在中国有什么用大家知道吗?那不知道的朋友们快跟着51题库考试学习网给大家带来的这篇文章吧!

第一,薪资待遇

ACCA作为全球规模最大的专业会计师组织,被公认为“国际财会界的通行证”。如今财会业的现状是,财务会计已经达到饱和,因此拥有ACCA证书的管理会计型人才一直都十分受到世界500强企业和国际国内大型知名企业的青睐。在中国,共有超过400家的国际国内知名企业是ACCA的“认可雇主企业”,如BP石油、联合利华、可口可乐、空客公司、GE等,ACCA在这些企业就职都可以获得很好的个人职业发展。

此外,根据相关数据统计,ACCA的普遍薪酬是普通财务薪酬的2-5倍,年薪普遍在30-80万人民币,有的甚至达到百万。

第二,发展前景

相比较国内已经趋于饱和的技术型会计,ACCA考试更偏重于财务管理以及财务统筹、预算以及规划企业走向和未来发展。据调查发现,在招聘工作中,大部分招聘职位如财务总监、总经理助理、董事长助理以及CFO等都可能附加ACCA的资格要求。而这些职位则要求求职者不仅需要具备财务方面的基础专业知识,同时还需要具备财务分析能力、财务管理能力、做出专业的财务报告让非财务人员理解并执行的能力等。

第三,知识结构完善

ACCA考试一共设置了16门课程,课程内容涵盖的不仅仅是会计、审计方面的专业知识,同时还涵盖人力资源、公司管理、战略决策、法务、税务、业绩衡量、财务管理、职业道德等方面的知识体系,为ACCA学员提供了完整的国际财会知识架构,让学员无论是从事财务、金融还是管理等方面的工作都能成为行业的领先者。

第四,全英文考试,国际商业惯例表达,提升专业语言能力。

以上就是由51题库考试学习网为您带来的有关AACA的相关信息了,想要获取更多信息的同学,请持续关注51题库考试学习网。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) When a director retires, amounts become payable to the director as a form. of retirement benefit as an annuity.

These amounts are not based on salaries paid to the director under an employment contract. Sirus has

contractual or constructive obligations to make payments to former directors as at 30 April 2008 as follows:

(i) certain former directors are paid a fixed annual amount for a fixed term beginning on the first anniversary of

the director’s retirement. If the director dies, an amount representing the present value of the future payment

is paid to the director’s estate.

(ii) in the case of other former directors, they are paid a fixed annual amount which ceases on death.

The rights to the annuities are determined by the length of service of the former directors and are set out in the

former directors’ service contracts. (6 marks)

Required:

Draft a report to the directors of Sirus which discusses the principles and nature of the accounting treatment of

the above elements under International Financial Reporting Standards in the financial statements for the year

ended 30 April 2008.

(b) Directors’ retirement benefits

The directors’ retirement benefits are unfunded plans which may fall under IAS19 ‘Employee Benefits’.

Sirus should review its contractual or constructive obligation to make retirement benefit payments to its former directors at the

time when they leave the firm. The payments may create a financial liability under IAS32, or may give rise to a liability of

uncertain timing and amount which may fall within the scope of IAS37 ‘Provisions, contingent liabilities and contingent

assets’. Certain former directors are paid a fixed annuity for a fixed term which is payable annually, and on death, the present

value of future payments are paid to the director’s estate. An annuity meets the definition of a financial liability under IAS32,

if there is a contractual obligation to deliver cash or a financial asset. The latter form. of annuity falls within the scope of

IAS32/39. The present value of the annuity payments should be determined. The liability is recognised because the directors

have a contractual right to the annuity and the firm has no discretion in terms of withholding the payment. As the rights to

the annuities are earned over the period of the service of the directors, then the costs should have been recognised also over

the service period.

Where an annuity has a life contingent element and, therefore, embodies a mortality risk, it falls outside the scope of IAS39

because the annuity will meet the definition of an insurance contract which is scoped out of IAS39, along with employers’

rights and obligations under IAS19. Such annuities will, therefore, fall within the scope of IAS37 if a constructive obligation

exists. Sirus should assess the probability of the future cash outflow of the present obligation. Because there are a number of

similar obligations, IAS37 requires that the class of obligations as a whole should be considered (similar to a warranty

provision). A provision should be made for the best estimate of the costs of the annuity and this would include any liability

for post retirement payments to directors earned to date. The liability should be built up over the service period rather than

just when the director leaves. In practice the liability will be calculated on an actuarial basis consistent with the principles in

IAS19. The liability should be recalculated on an annual basis, as for any provision, to take account of changes in directors

and other factors. The liability will be discounted where the effect is material.

(iii) Advice in connection with the sale of the manufacturing premises by Tethys Ltd; (7 marks)

(iii) Tethys Ltd – Sale of the manufacturing premises

Value added tax (VAT)

– The building is not a new building (i.e. it is more than three years old). Accordingly, the sale of the building is an

exempt supply and VAT should not be charged unless Tethys Ltd has opted to tax the building in the past.

Taxable profits on sale

– There will be no balancing adjustment in respect of industrial building allowances as the building is to be sold on

or after 21 March 2007.

– The capital gain arising on the sale of the building will be £97,760 (£240,000 – (£112,000 x 1·27)).

Rollover relief

– Tethys Ltd is not in a capital gains group with Saturn Ltd. Accordingly, rollover relief will only be available if Tethys

Ltd, rather than any of the other Saturn Ltd group companies, acquires sufficient qualifying business assets.

– The amount of sales proceeds not spent in the qualifying period is chargeable, i.e. £40,000 (£240,000 –

£200,000). The balance of the gain, £57,760 (£97,760 – £40,000), can be rolled over.

– Qualifying business assets include land and buildings and fixed plant and machinery. The assets must be brought

into immediate use in the company’s trade.

– The assets must be acquired in the four-year period beginning one year prior to the sale of the manufacturing

premises.

Further information required:

– Whether or not Tethys Ltd has opted to tax the building in the past for the purposes of VAT.

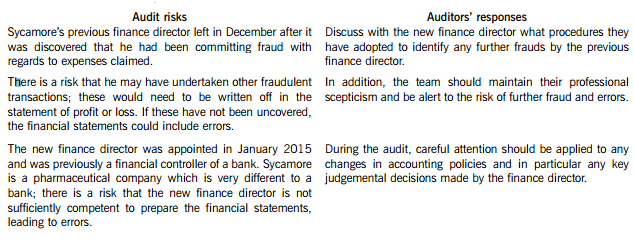

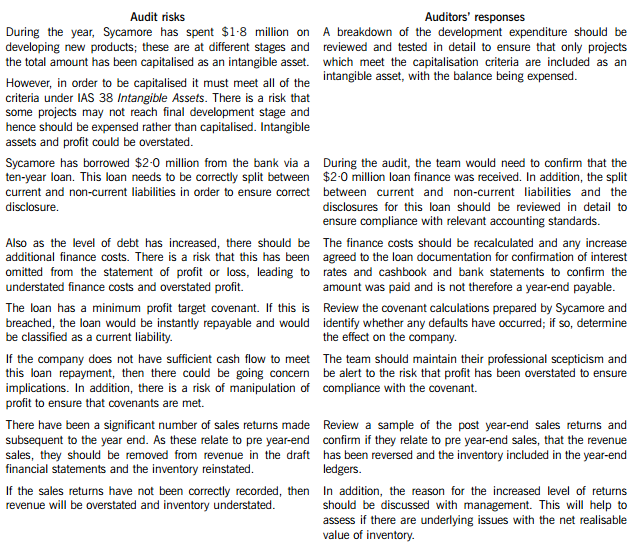

You are the audit supervisor of Maple & Co and are currently planning the audit of an existing client, Sycamore Science Co (Sycamore), whose year end was 30 April 2015. Sycamore is a pharmaceutical company, which manufactures and supplies a wide range of medical supplies. The draft financial statements show revenue of $35·6 million and profit before tax of $5·9 million.

Sycamore’s previous finance director left the company in December 2014 after it was discovered that he had been claiming fraudulent expenses from the company for a significant period of time. A new finance director was appointed in January 2015 who was previously a financial controller of a bank, and she has expressed surprise that Maple & Co had not uncovered the fraud during last year’s audit.

During the year Sycamore has spent $1·8 million on developing several new products. These projects are at different stages of development and the draft financial statements show the full amount of $1·8 million within intangible assets. In order to fund this development, $2·0 million was borrowed from the bank and is due for repayment over a ten-year period. The bank has attached minimum profit targets as part of the loan covenants.

The new finance director has informed the audit partner that since the year end there has been an increased number of sales returns and that in the month of May over $0·5 million of goods sold in April were returned.

Maple & Co attended the year-end inventory count at Sycamore’s warehouse. The auditor present raised concerns that during the count there were movements of goods in and out the warehouse and this process did not seem well controlled.

During the year, a review of plant and equipment in the factory was undertaken and surplus plant was sold, resulting in a profit on disposal of $210,000.

Required:

(a) State Maples & Co’s responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

(b) Describe SIX audit risks, and explain the auditor’s response to each risk, in planning the audit of Sycamore Science Co. (12 marks)

(c) Sycamore’s new finance director has read about review engagements and is interested in the possibility of Maple & Co undertaking these in the future. However, she is unsure how these engagements differ from an external audit and how much assurance would be gained from this type of engagement.

Required:

(i) Explain the purpose of review engagements and how these differ from external audits; and (2 marks)

(ii) Describe the level of assurance provided by external audits and review engagements. (2 marks)

(a) Fraud responsibility

Maple & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error.

In order to fulfil this responsibility, Maple & Co is required to identify and assess the risks of material misstatement of the financial statements due to fraud.

They need to obtain sufficient appropriate audit evidence regarding the assessed risks of material misstatement due to fraud, through designing and implementing appropriate responses. In addition, Maple & Co must respond appropriately to fraud or suspected fraud identified during the audit.

When obtaining reasonable assurance, Maple & Co is responsible for maintaining professional scepticism throughout the audit, considering the potential for management override of controls and recognising the fact that audit procedures which are effective in detecting error may not be effective in detecting fraud.

To ensure that the whole engagement team is aware of the risks and responsibilities for fraud and error, ISAs require that a discussion is held within the team. For members not present at the meeting, Sycamore’s audit engagement partner should determine which matters are to be communicated to them.

(b) Audit risks and auditors’ responses

(c) (i) Review engagements

Review engagements are often undertaken as an alternative to an audit, and involve a practitioner reviewing financial data, such as six-monthly figures. This would involve the practitioner undertaking procedures to state whether anything has come to their attention which causes the practitioner to believe that the financial data is not in accordance with the financial reporting framework.

A review engagement differs to an external audit in that the procedures undertaken are not nearly as comprehensive as those in an audit, with procedures such as analytical review and enquiry used extensively. In addition, the practitioner does not need to comply with ISAs as these only relate to external audits.

(ii) Levels of assurance

The level of assurance provided by audit and review engagements is as follows:

External audit – A high but not absolute level of assurance is provided, this is known as reasonable assurance. This provides comfort that the financial statements present fairly in all material respects (or are true and fair) and are free of material misstatements.

Review engagements – where an opinion is being provided, the practitioner gathers sufficient evidence to be satisfied that the subject matter is plausible; in this case negative assurance is given whereby the practitioner confirms that nothing has come to their attention which indicates that the subject matter contains material misstatements.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-04-07

- 2020-01-10

- 2020-05-02

- 2020-01-10

- 2020-01-10

- 2019-03-28

- 2021-08-29

- 2020-01-10

- 2020-01-10

- 2020-05-05

- 2020-01-09

- 2020-03-01

- 2020-01-10

- 2020-01-10

- 2020-09-03

- 2020-02-27

- 2020-03-17

- 2020-04-16

- 2020-01-10

- 2020-01-09

- 2020-01-10

- 2020-01-10

- 2020-02-20

- 2020-03-26

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-14

- 2019-12-29

- 2020-01-10