2020年ACCA考试报名人数将持续增长?报考ACCA到底有没有用

发布时间:2020-03-07

从近几年的考试情况来看,2020年ACCA考试报名人数很可能会持续增长,这让一些对于ACCA不了解的小伙伴不免询问报考ACCA究竟有哪些好处?下面,51题库考试学习网为大家带来有关2020年ACCA会员就业前景的相关信息,以供参考。

首先,ACCA拥有完善的课程培训。ACCA的课程就是根据现时商务社会对财会人员的实际要求进行开发、设计的,尤其是注意培养学员的分析能力和在复杂条件下的决策、判断能力。这些课程能够显著提升学员的能力。因此,ACCA课程所带来的系统的、高质量的培训会给予学生真才实学,让学员学成后能适应各种环境,并使会员成为具有全面管理素质的高级财务管理专家。而这也是ACCA会员拥有高薪待遇的主要原因。

其次,ACCA在国际上的多个国家都受到了广泛认可。ACCA属于国际专业会计师组织,在国际上享有很高的声誉,与众多国际知名企业建立了密切的合作关系,比如跨国企业、各国地方企业、其他会计师组织、教育机构、以及联合国、世界银行等世界性组织。这些组织和企业都能给予学员优厚的待遇。

那么,ACCA会员的就职方向是哪些呢?ACCA学员毕业后的就职方向:外资银行金融投资分析师;跨国公司的财务、内审、金融、风险控制岗位;国际会计师事务所的审计师、咨询师岗位;国内境外上市公司的财务、金融分析岗位;国内审计师事务所的涉外部门主管等。这些岗位都属于涉外岗位,不但拥有良好的薪资待遇,还能带来较高的社会地位。

另外,ACCA会员的高含金量还体现在这些方面:

首先,ACCA会员资格在国际上得到广泛认可,尤其得到欧盟立法以及许多国家公司法的承认。因此可以说,拥有ACCA会员资格,就拥有了在世界各地就业的“通行证”。在世界上的很多国家,ACCA会员就是许多公司青睐的人才。

其次,ACCA会员在工商企业财务部门、(四大)审计/会计师事务所、金融机构和财政、税务部门从事财务以及财务管理工作,ACCA会员中有很多在世界各地大公司担任高级职位(财务经理、财务总监CFO,甚至总裁CEO)。因此,ACCA会员的就业前景是非常好的。

此外,ACCA还受到在中国的跨国公司、大型企业和国际“五大”会计公司全面认可。总的来说,ACCA会员年薪在中国50-100万RMB。

以上就是关于ACCA就业前景的相关内容。51题库考试学习网提醒:随着我国对外贸易的进一步发展,ACCA会员的含金量将进一步提升,因此小伙伴们如果感兴趣的话,那么要抓紧时间报考哦。最后,51题库考试学习网预祝准备参加2020年ACCA考试的小伙伴都能顺利通过。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

A new internal auditor, Daisy Rosepetal, has recently joined Bluebell Co. She has been asked by management to

establish and to monitor a variety of social and environmental Key Performance Indicators (KPIs). Daisy has no

experience in this area, and has asked you for some advice. It has been agreed with Bluebell Co’s audit committee

that you are to provide guidance to Daisy to help her in this part of her role, and that this does not impair the

objectivity of the audit.

(c) Recommend EIGHT KPIs which could be used to monitor Bluebell Co’s social and environmental

performance, and outline the nature of evidence that should be available to provide assurance on the

accuracy of the KPIs recommended. Your answer should be in the form. of briefing notes to be used at a

meeting with Daisy Rosepetal. (10 marks)

Note: requirement (c) includes 2 professional marks.

(iii) Calculate the cash remaining in the company as a result of the salary and dividend payments made in

(ii) above. (1 mark)

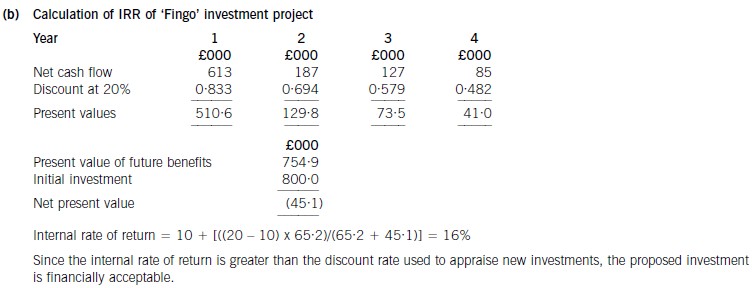

(b) Calculate the internal rate of return of the proposed investment and comment on your findings. (5 marks)

(b) Discuss the key issues which will need to be addressed in determining the basic components of an

internationally agreed conceptual framework. (10 marks)

Appropriateness and quality of discussion. (2 marks)

(b) There are several issues which have to be addressed if an international conceptual framework is to be successfully developed.

These are:

(i) Objectives

Agreement will be required as to whether financial statements are to be produced for shareholders or a wide range of

users and whether decision usefulness is the key criteria or stewardship. Additionally there is the question of whether

the objective is to provide information in making credit and investment decisions.

(ii) Qualitative Characteristics

The qualities to be sought in making decisions about financial reporting need to be determined. The decision usefulness

of financial reports is determined by these characteristics. There are issues concerning the trade-offs between relevance

and reliability. An example of this concerns the use of fair values and historical costs. It has been argued that historical

costs are more reliable although not as relevant as fair values. Additionally there is a conflict between neutrality and the

traditions of prudence or conservatism. These characteristics are constrained by materiality and benefits that justify

costs.

(iii) Definitions of the elements of financial statements

The principles behind the definition of the elements need agreement. There are issues concerning whether ‘control’

should be included in the definition of an asset or become part of the recognition criteria. Also the definition of ‘control’

is an issue particularly with financial instruments. For example, does the holder of a call option ‘control’ the underlying

asset? Some of the IASB’s standards contravene its own conceptual framework. IFRS3 requires the capitalisation of

goodwill as an asset despite the fact that it can be argued that goodwill does not meet the definition of an asset in the

Framework. IAS12 requires the recognition of deferred tax liabilities that do not meet the liability definition. Similarly

equity and liabilities need to be capable of being clearly distinguished. Certain financial instruments could either be

liabilities or equity. For example obligations settled in shares.

(iv) Recognition and De-recognition

The principles of recognition and de-recognition of assets and liabilities need reviewing. Most frameworks have

recognition criteria, but there are issues over the timing of recognition. For example, should an asset be recognised when

a value can be placed on it or when a cost has been incurred? If an asset or liability does not meet recognition criteria

when acquired or incurred, what subsequent event causes the asset or liability to be recognised? Most frameworks do

not discuss de-recognition. (The IASB’s Framework does not discuss the issue.) It can be argued that an item should be

de-recognised when it does not meet the recognition criteria, but financial instruments standards (IAS39) require other

factors to occur before financial assets can be de-recognised. Different attributes should be considered such as legal

ownership, control, risks or rewards.

(v) Measurement

More detailed discussion of the use of measurement concepts, such as historical cost, fair value, current cost, etc are

required and also more guidance on measurement techniques. Measurement concepts should address initial

measurement and subsequent measurement in the form. of revaluations, impairment and depreciation which in turn

gives rise to issues about classification of gains or losses in income or in equity.

(vi) Reporting entity

Issues have arisen over what sorts of entities should issue financial statements, and which entities should be included

in consolidated financial statements. A question arises as to whether the legal entity or the economic unit should be the

reporting unit. Complex business arrangements raise issues over what entities should be consolidated and the basis

upon which entities are consolidated. For example, should the basis of consolidation be ‘control’ and what does ‘control’

mean?

(vii) Presentation and disclosure

Financial reporting should provide information that enables users to assess the amounts, timing and uncertainty of the

entity’s future cash flows, its assets, liabilities and equity. It should provide management explanations and the limitations

of the information in the reports. Discussions as to the boundaries of presentation and disclosure are required.

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-10

- 2020-04-18

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2020-01-09

- 2020-05-01

- 2020-05-10

- 2020-01-10

- 2020-01-10

- 2020-02-05

- 2020-05-20

- 2020-01-09

- 2020-01-10

- 2020-01-10

- 2020-05-10

- 2020-01-10

- 2020-04-14

- 2020-03-07

- 2020-03-21

- 2020-02-28

- 2020-01-05

- 2020-01-10

- 2020-02-19

- 2020-03-19

- 2020-01-10

- 2020-01-10

- 2020-05-15