到底要不要参加ACCA的考试呢?了解一下!

发布时间:2020-05-01

ACCA证书对于刚踏入财会行业的小白们来说是一块强有力的敲门砖,它证明了你具有了国际注册会计的资格和水平,听了这些之后你可能会有些心动,纠结于自己要不要考。那么,看一看下面的内容吧!

首先,对于一个几乎没有工作经验的应届生,ACCA将成为你能力的一个体现。ACCA证书是金融财会领域的热门证书之一,它的含金量和认可度备受国内财会人才的瞩目。在学校里面,你的时间如果很充裕的话,大可以把这部分时间利用起来考一个ACCA证书。ACCA证书对于刚踏入财会行业的小白们来说是一块强有力的敲门砖,它证明了你具有了国际注册会计的资格和水平。ACCA考试对英语有一定要求,这样也把英语一起学习了。如果是上课外辅导班还可以认识更多的人,说不定会交到一些朋友。本科毕业后想出国,有ACCA证书是一个加分项。相比于其他的同学,你有了ACCA证书,求职进入心仪的公司、找到合适的工作,概率也会更大一点,也就会早一点实现财务自由。不论是男孩子还是女孩子,年轻的时候可以好好拼搏一下。有句话说,拼搏的人生更美丽。

其次,在国外留学或者工作的同学,尤其是会计专业本科在英国就读,是建议你考的。ACCA是英国的财会考试,如果你正好在英国留学,并且就读于会计相关专业,完全可以利用教材、地点之便参加ACCA考试。作为本土考试,在英国大学里学习相关知识,可以让你更快掌握英式的答题思路和逻辑思维,考起试来事半功倍。ACCA的题目比较难,学习了ACCA,自己的考试成绩也有可能会得到提升。本身在国外,有良好的英文学习环境,学英语也会轻松一些,多跟会说英文的人交流,这样不仅可以培养自己的英语思维,还提升了自己的英语口语,岂不是很大的收获?即便你毕业之后没有从事会计相关的工作,也不会觉得这些学习是在浪费时间。

当然了,不论做什么事情,主要还是要靠自己的努力和勤奋。ACCA并不是高不可攀,更重要的是要有不断挑战自己、战胜困难的勇气和信心,这样也才能把ACCA拿下来。所以,想考ACCA的小伙伴不妨去试一试。

下面小编为大家准备了 ACCA考试 的相关考题,供大家学习参考。

(b) How can Maslow’s theory be applied to the motivation of staff? (5 marks)

(b) This theory is based on the idea that the goals of the individual and the organisation can be integrated and that personal satisfaction can be achieved through the workplace. It also assumes that individuals will achieve self-actualisation through their role in assisting the organisation to achieve its objectives. It follows therefore that work is the principal source of satisfaction.

The theory’s practical application is that managers should recognise that subordinates’ needs are always evolving and increasing, so continued attention to increasing the employees’ personal development, opportunities for advancement and recognition of achievement are essential to keep them motivated.

2 It was the final day of a two-week-long audit of Van Buren Company, a longstanding client of Fillmore Pierce Auditors.

In the afternoon, Anne Hayes, a recently qualified accountant and member of the audit team, was following an audit

trail on some cash payments when she discovered what she described to the audit partner, Zachary Lincoln, as an

‘irregularity’. A large and material cash payment had been recorded with no recipient named. The corresponding

invoice was handwritten on a scrap of paper and the signature was illegible.

Zachary, the audit partner, was under pressure to finish the audit that afternoon. He advised Anne to seek an

explanation from Frank Monroe, the client’s finance director. Zachary told her that Van Buren was a longstanding client

of Fillmore Pierce and he would be surprised if there was anything unethical or illegal about the payment. He said

that he had personally been involved in the Van Buren audit for the last eight years and that it had always been

without incident. He also said that Frank Monroe was an old friend of his from university days and that he was certain

that he wouldn’t approve anything unethical or illegal. Zachary said that Fillmore Pierce had also done some

consultancy for Van Buren so it was a very important client that he didn’t want Anne to upset with unwelcome and

uncomfortable questioning.

When Anne sought an explanation from Mr Monroe, she was told that nobody could remember what the payment

was for but that she had to recognise that ‘real’ audits were sometimes a bit messy and that not all audit trails would

end as she might like them to. He also reminded her that it was the final day and both he and the audit firm were

under time pressure to conclude business and get the audit signed off.

When Anne told Zachary what Frank had said, Zachary agreed not to get the audit signed off without Anne’s support,

but warned her that she should be very certain that the irregularity was worth delaying the signoff for. It was therefore

now Anne’s decision whether to extend the audit or have it signed off by the end of Friday afternoon.

Required:

(a) Explain why ‘auditor independence’ is necessary in auditor-client relationships and describe THREE threats

to auditor independence in the case. (9 marks)

(a) Importance of independence

The auditor must be materially independent of the client for the following reasons:

To increase credibility and to underpin confidence in the process. In an external audit, this will primarily be for the benefit of

the shareholders and in an internal audit, it will often be for the audit committee that is, in turn, the recipient of the internal

audit report.

To ensure the reliability of the audit report. Any evidence of lack of independence (or ‘capture’) has the potential to undermine

all or part of the audit report thus rendering the exercise flawed.

To ensure the effectiveness of the investigation of the process being audited. An audit, by definition, is only effective as a

means of interrogation if the parties are independent of each other.

Three threats to independence

There are three threats to independence described in the case.

The same audit partner (Zachary) was assigned to Van Buren in eight consecutive years. This is an association threat and is

a contravention of some corporate governance codes. Both Sarbanes-Oxley and the Smith Guidance (contained in the UK

Combined Code), for example, specify auditor rotation to avoid association threat.

Fillmore Pierce provides more than one service to the same client. One of the threats to independence identified between

Arthur Andersen and Enron after the Enron collapse was an over-dependence on Enron by Andersen arising from the provision

of several services to the same client. Good practice is not to offer additional services to audit clients to avoid the appearance

of compromised independence. Some corporate governance codes formally prohibit this.

The audit partner (Zachary) is an old friend of the financial director of Van Buren (Frank). This ‘familiarity’ threat should be

declared to Fillmore Pierce at the outset and it may disqualify Zachary from acting as audit partner on the Van Buren account.

Hindberg is a car retailer. On 1 April 2014, Hindberg sold a car to Latterly on the following terms:

The selling price of the car was $25,300. Latterly paid $12,650 (half of the cost) on 1 April 2014 and would pay the remaining $12,650 on 31 March 2016 (two years after the sale). Hindberg’s cost of capital is 10% per annum.

What is the total amount which Hindberg should credit to profit or loss in respect of this transaction in the year ended 31 March 2015?

A.$23,105

B.$23,000

C.$20,909

D.$24,150

At 31 March 2015, the deferred consideration of $12,650 would need to be discounted by 10% for one year to $11,500 (effectively deferring a finance cost of $1,150). The total amount credited to profit or loss would be $24,150 (12,650 + 11,500).

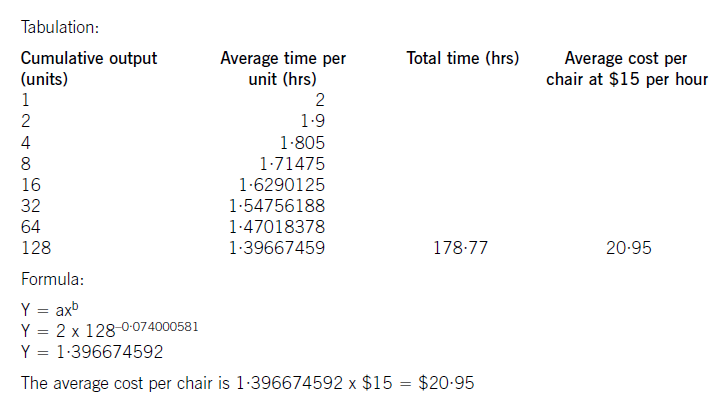

Big Cheese Chairs (BCC) manufactures and sells executive leather chairs. They are considering a new design of massaging chair to launch into the competitive market in which they operate.

They have carried out an investigation in the market and using a target costing system have targeted a competitive selling price of $120 for the chair. BCC wants a margin on selling price of 20% (ignoring any overheads).

The frame. and massage mechanism will be bought in for $51 per chair and BCC will upholster it in leather and assemble it ready for despatch.

Leather costs $10 per metre and two metres are needed for a complete chair although 20% of all leather is wasted in the upholstery process.

The upholstery and assembly process will be subject to a learning effect as the workers get used to the new design.

BCC estimates that the first chair will take two hours to prepare but this will be subject to a learning rate (LR) of 95%.

The learning improvement will stop once 128 chairs have been made and the time for the 128th chair will be the time for all subsequent chairs. The cost of labour is $15 per hour.

The learning formula is shown on the formula sheet and at the 95% learning rate the value of b is -0·074000581.

Required:

(a) Calculate the average cost for the first 128 chairs made and identify any cost gap that may be present at

that stage. (8 marks)

(b) Assuming that a cost gap for the chair exists suggest four ways in which it could be closed. (6 marks)

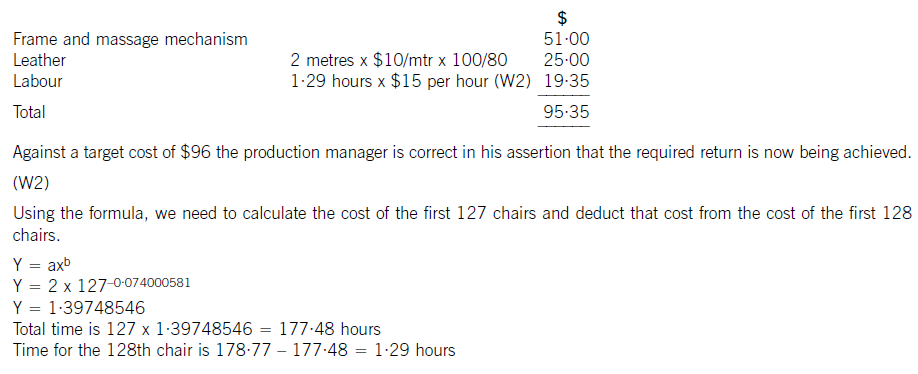

The production manager denies any claims that a cost gap exists and has stated that the cost of the 128th chair will be low enough to yield the required margin.

(c) Calculate the cost of the 128th chair made and state whether the target cost is being achieved on the 128th chair. (6 marks)

(W1)

The cost of the labour can be calculated using learning curve principles. The formula can be used or a tabular approach would

also give the average cost of 128 chairs. Both methods are acceptable and shown here.

(b) To reduce the cost gap various methods are possible (only four are needed for full marks)

– Re-design the chair to remove unnecessary features and hence cost

– Negotiate with the frame. supplier for a better cost. This may be easier as the volume of sales improve as suppliers often

are willing to give discounts for bulk buying. Alternatively a different frame. supplier could be found that offers a better

price. Care would be needed here to maintain the required quality

– Leather can be bought from different suppliers or at a better price also. Reducing the level of waste would save on cost.

Even a small reduction in waste rates would remove much of the cost gap that exists

– Improve the rate of learning by better training and supervision

– Employ cheaper labour by reducing the skill level expected. Care would also be needed here not to sacrifice quality or

push up waste rates.

(c) The cost of the 128th chair will be:

声明:本文内容由互联网用户自发贡献自行上传,本网站不拥有所有权,未作人工编辑处理,也不承担相关法律责任。如果您发现有涉嫌版权的内容,欢迎发送邮件至:contact@51tk.com 进行举报,并提供相关证据,工作人员会在5个工作日内联系你,一经查实,本站将立刻删除涉嫌侵权内容。

- 2020-01-09

- 2020-01-09

- 2020-03-15

- 2020-01-10

- 2020-01-09

- 2020-01-09

- 2020-02-05

- 2020-01-10

- 2020-01-10

- 2020-01-10

- 2021-09-20

- 2020-01-10

- 2020-05-02

- 2020-02-18

- 2020-01-09

- 2020-03-07

- 2020-02-01

- 2021-10-17

- 2021-04-24

- 2020-01-30

- 2020-03-27

- 2020-02-02

- 2020-01-10

- 2020-04-23

- 2020-05-14

- 2020-01-10

- 2020-05-05

- 2020-01-09

- 2020-03-31

- 2020-01-09